![What is Ripple (XRP)? [A Comprehensive Guide to Understanding XRP]](https://www.publish0x.com/img/62045.jpeg?action=resize&ar=1&inv=0&ori=1&st=1&up=1&w=1140&signature=66f6f13e3dee93774fcc3d516229db91c6155bce1f33eb6f308a4e08adf93e14)

Ripple and its token XRP, like Bitcoin and Ethereum and a few other tokens in the top 20, stand out in a market where every 3rd token appears to be a pale imitation of some token or other - whether it is a cross-border banking-focused token, a means of exchange or a supply chain focused token. Some might argue that Ripple should not be put in the same bracket as “true” cryptocurrencies like Bitcoin and Ethereum, but proponents of these arguments fail to see that Ripple is designed with a very specific purpose in mind, for which the lesser degree of decentralization is more suitable.

That certainly hasn’t stopped millions of investors from purchasing their share of tokens in the hope of a price rise. Against a day-to-day use token like Bitcoin, or utility tokens like many ERC-20 tokens, XRP does not have much “in-the-moment” utility for retail investors (which is a major qualm for them; a point we shall address shortly) - and yet Ripple seems to unquestionably be growing, both in terms of the number of investors and the number of financial institutions joining its RippleNet is unmatched by any other project in its capability to attract incumbent enterprises towards Distributed Ledger Technologies (DLTs).

Ripple shares another interesting characteristic in common with Bitcoin and Ethereum, surpassed only by these two (and perhaps a few other projects) - one of the most fascinating origin stories.

History of Ripple (XRP)

Believe it or not, Ripple’s fundamental conception actually dates back to before Bitcoin. In 2004, Ryan Fugger, web and decentralized systems developer and consultant, conceived of a network in which a monetary system “based on the trust present in our ordinary social and business relationships.” This was a community project, that employed the IOU system that Ripple still operates on today, and was called RipplePay.

Fast forward a few years later, and prominent crypto figure Jed McCaleb - the man who created Mt. Gox and now the Director of the Stellar Development Foundation - and Chris Larsen, a Silicon Valley angel investor who has made a career out of building several successful pro-consumer businesses, like Prosper Marketplace and E-Loan.

Larsen also became Ripple’s Chief Executive Officer (CEO) stepped down from the position in 2016 to become the Executive Chairman of the board, at which point Brad Garlinghouse was appointed as CEO, who continues to serve the role.

Following his sale of Mt. Gox, McCaleb began working on a decentralized network that was not dissimilar from what Fugger was working on, which was focused on establishing consensus between network members without the need for mining. Fugger handed the development of RipplePay to McCaleb and Larsen, and the development of the protocol was handled by the then named OpenCoin, which was eventually changed to Ripple Labs. McCaleb and Larsen then became the official founders of Ripple, before quickly recruiting current Chief Cryptographer David Schwartz, among many others.

McCaleb himself has achieved a sort of demi-god status among the cryptocommunity. Even well before his entry into DLTs and cryptocurrencies, McCaleb was working extensively with Peer-to-Peer technology, having developed the filesharing eDonkey P2P network and the eDonkey2000 software. McCaleb served as the Chief Technology Officer (CTO) until 2013, after which he formed the Stellar Development Foundation jointly with Joyce Kim in 2014. He is currently the Director and CTO of Stellar. Some hold the Stellar Lumens (XLM) project as a competitor to Ripple, though this can also be debated.

The two founders envisioned Ripple as a payments network that could instantaneously transact both fiat and crypto funds, as well as other value-based assets like frequent flyer miles and loyalty points. They saw Ripple as playing a part in the creation of the “Internet of Value”, which is essentially the instantaneous transaction of these different assets of value.

It is also important to note that Ripple is a Ripple has conducted two rounds of funding since its inception, raising over $120 million. The Series A funding was conducted in 2013, and received funding from many big names, including Google Ventures, Andreesen Horowitz and IDF Capital Partners. Other sources of funding include Standard Chartered, SBI Investment, Accenture, BlockChain Capital, China Growth Capital and Santander InnoVentures. More than 30 companies have invested in Ripple.

The Purpose of the XRP Token - Mostly Just for Financial Institutions

Source: https://www.ripple.com/wp-content/uploads/2019/09/RippleNet-On-Demand-Liquidity.pdf

Ripple and its token XRP are two quite separate entities, the first being the company behind the development and business expansion of the second, which is the actual token. The most important aspect of Ripple that is required for a would-be investor to know is that the token, and all of Ripple’s services are intended primarily for incumbent enterprise entities - even within that, it’s mostly just financial institutions and companies.

That’s not to say that Ripple does not have use outside a banking network. In fact, it has actually seen implementation already on the Point-of-Sale side, via the development of third party applications, like those made by the developers at XRPL labs.

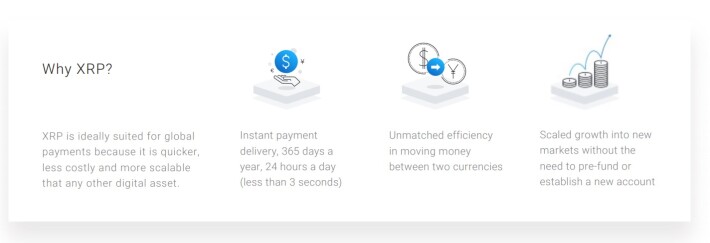

Ripple itself has explained, both in blog posts, conferences and in comprehensive videos, the purpose of its network: to support emerging economies, payment trends and the e-commerce/payment platform boom by offering a modern solution that keeps up with how customers and businesses’ transaction/value exchange desires.

This includes quicker payments, access to remote markets, lower transaction fees and on-demand liquidity, the latter being a particularly strong pain point for current international payments.

Ripple’s three main services are xVia, xCurrent and xRapid, which have been merged together on the RippleNet for its members to utilize. While these are now part of one and the same service, namely RippleNet, when they weren’t merged, they served 3 distinct purposes.

XVia was used to connect emerging and remote markets to the global economy. It provides APIs to these businesses that would like to expand quickly by entering the global market. Establishing new corridors quickly is the name of the game here. xCurrent is an enterprise solution that facilitates instant settlements with certainty in transaction execution. One of the issues with the SWIFT system is that payments can sometimes take weeks, with no surety in the fact that it has been executed. xCurrent offers a real-time messaging solution that to execute and confirm the transaction. xRapid speeds up international payments with the bridge currency being the XRP token and provides the aforementioned on-demand liquidity.

The RippleNet, which will be discussed in greater detail later, is a banking network that has been described by CEO Brad Garlinhouse as an upgrade to the world’s current go-to cross-border payments system, SWIFT. Calling it SWIFT 2.0, Garlinghouse has spoken extensively with financial industry insiders on the benefits of RippleNet, which has already seen over 200 financial players join the network.

Issues

Of course, Ripple has received its fair share of - justifiable - complaints, mostly having to do with the fact that its tokens are pre-mined, that the network is, comparatively, centralized, and, for retail investors, the XRP token lacks a real use case. These two points have led to it lawsuits, which have not yet been put to rest.

The first point has been one of the key contentions in the lawsuit filed against Ripple by some retail investors, who are among a minority who have threatened to launch a hard fork. Ripple’s 100 billion tokens have all been pre-mined, and is periodically released by Ripple into the market, some of which has been purchased. The argument is that Ripple has made it seem as if XRP is a currency, which the plaintiffs argue is not the case.

Furthermore, Ripple’s periodic release of tokens has also been cited as a cause for concern. This has some investors worried that Ripple could cause a massive drop in the price, as a greater supply means less demand. Ripple officials have said that this wouldn’t be in Ripple’s interests to do so, which is correct, but in combination with the fact that Ripple has enormous influence in the operation of the network,

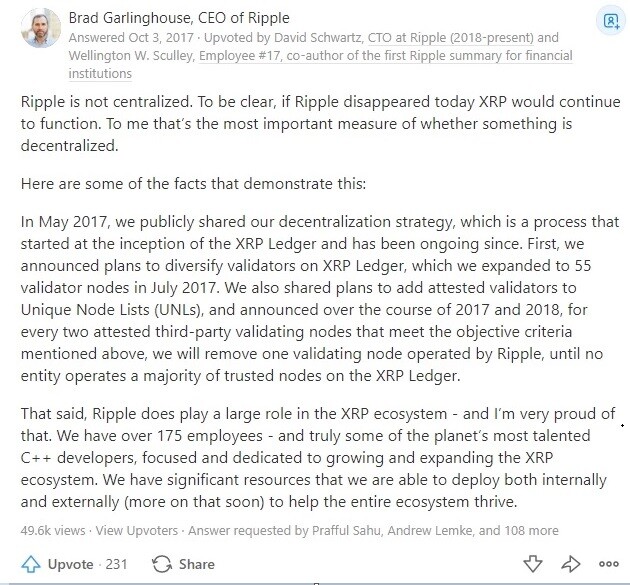

On top of the argument stated above, Ripple’s relative lack of decentralization has compounded the problem. Ripple is indeed more on the centralized side of the decentralization spectrum, running many nodes on the network. However, Garlinghouse himself has said that Ripple has taken steps to ensure greater decentralization by removing one of Ripple’s validating nodes for every 2 attested third party nodes that meet the required criteria to be a node.

Source: https://www.quora.com/Why-is-Ripple-centralized

A former Ripple employee has himself said that the growth of Ripple as an entity is separate from the growth of XRP, which are uncorrelated. Ripple has tried to assuage this sentiment by introducing some retail focused use cases: it partnered with one of the world’s largest money transfer services MoneyGram earlier this year. The applications developed by XRPL Labs, among others, are also somewhat of a rebuttal to the argument that XRP lacks use cases, but the point haunts Ripple still. Perhaps this will change in the future.

As you can see, the issues lie primarily on the retail side. On the institutional side, however, Ripple is doing phenomenally well, gathering more partners at a breakneck pace. These partners have offered Ripple and its solutions a lot of praise, which has been backed by pilot programs that have proven the speed and efficiency of the solutions. It is for this reason that many investors are still bullish on Ripple’s prospects, which, for the moment, has no competition to give it a run for its money.

Partnerships

In what probably Ripple’s hottest selling point, the company has established an incredibly strong and diverse network of partners that covers the entire 6 continents and over 40 countries. It has done so through RippleNet, its much discussed network of financial institutions, payments providers and other payment entities that utilize its services and the XRP token to facilitate instantaneous transfers with certainty.

The lengthy list of Ripple’s partners puts it out of the scope of this write-up, but there are several excellent sources available that detail both the quality and quantity of those partnerships.

Competitors

In its particular niche, which is providing banking solutions to incumbent financial institutions, Ripple is by far the leader of the pack. There are many more crypto projects which are working on the same industry pain points, but one would be hard pressed to say that they compete with Ripple in any meaningful way.

Ripple’s closest competitor, which one may not even be able to genuinely say is a competitor, is Stellar Lumens (XLM), which was launched by Jed McCaleb, who, as we mentioned, co-founded Ripple itself.

While Stellar is indeed working with banks and IBM to launch stablecoin solutions, it may not be in good faith to say that it is a true competitor to Ripple and XRP. Rather, Stellar is focused more on the void that has been formed by Ripple in its use case: retail usage.

Stating that it intends to “unlock the world’s economic potential by making money more fluid, markets more open and people more empowered”, Stellar has built solutions that are far retail oriented. This includes SatoshiPay, which eliminates the problems associated by digital advertisers by allowing users to make micropayments for online content. It has also built a decentralized exchange called StellarX. That being said, it has worked with IBM to create the IBM World Wire, a solution that helps financial institutions send any currency across the world quickly and conveniently.

Stellar is similar to Bitcoin in that it is intended for individuals to make quick and cheap payments to anyone in the world, but much quicker and cheaper.

Perhaps a greater threat to Ripple and XRP is the trend of banks forming their own solutions - which Ripple has dismissed, at least in the case of JP Morgan Chase and its JPM Coin. Banks may indeed decide to come up with their own modern solutions to modern banking problems, but with Ripple and RippleNet already in existence, perhaps they may just decide to stick with Ripple.

Conclusion

Ripple and its XRP token is certainly one of the projects that have the most potential for growth. It has survived for many years and entrenched itself into the market and enterprises - the latter being especially important, as this tends to precede mass adoption.

Whether or not the XRP token will come to its former heights of $3, or even higher, is more of an open question. Perhaps Ripple is just laying the foundation by cementing its place in the enterprise market first, before providing more use cases to retail market in due time.

Regardless, XRP remains one of the tokens to keep an eye on, and a decent choice for the long-term HODL.