Ripple’s XRP is an odd cryptocurrency (some might even it say that it isn’t a cryptocurrency, but we won’t address that today) in many respects.

There is an unusually high supply of the token (100 billion, some of which has been burnt) that is released by Ripple every now and then, the kind of move that has investors worried about its price. Among the top 10 coins by market cap, in my opinion, it is the most distinct of them to do so well in such a niche use case. And above all, it is a permissioned network where some entities - Ripple, mostly - have a significant amount of control, leading some to argue that Ripple and XRP are centralized in nature, which is something I have discussed before.

In short, Ripple and XRP is a bit of a mystery to newbie investors, who only invest in because it’s talked about so much and because it may appear as a “safe bet.” After all, if so many banks and companies can get on board with a crypto-oriented project like Ripple, then it must be legit, right?

That said, maybe we could do with some educating on what Ripple, XRP and the RippleNet is all about. That might give investors a better idea of what their position should be like and just so that they can get a sense of what a Distributed Ledger Technology can do for an industry.

What Does Ripple Do?

Source: Ripple

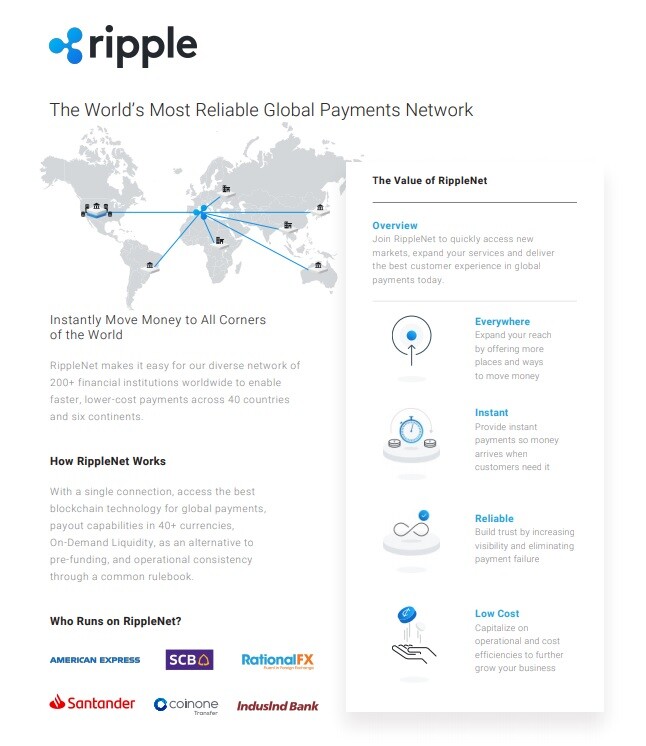

Ripple is the foundation that is behind the development and business expansion of the XRP token and its related products and services. The XRP is largely a token for enterprise use. XRP and the RippleNet, a network of banks that utilizes Ripple’s solutions to facilitate cross-border payments, are closely tied - both of which I’ll explain in a bit.

Ripple can be thought of as an upgrade of the existing financial payments framework. Currently, the world’s financial institutions use the SWIFT system as its go-to solution for transferring money worldwide. It is serviceable, and has done well to promote e-commerce growth and international accessibility for customers over the years, but it does come with disadvantages - disadvantages that have become apparent with the advent of DLTs that can execute financial transactions better in every imaginable way.

This, in my view, is Ripple’s raison d'etre. It is a fintech solution for the modern world, one that is showing rising growth in e-commerce, payments platforms, liquidity demands and international relationships. No longer do people depend on local markets, which offer only limited goods and services. We now look towards individuals and SMEs located across the world to obtain otherwise unavailable goods. And we use outdated financial systems which cannot keep up with this changing face of the world’s economy.

Ripple, which recently merged its xCurrent, xRapid and xVia products into one on the RippleNet, offers that solution for the new economy. It offers technological solutions that can support the volume and frequency of transactions that the world needs now and in the future, in a time frame of a few seconds, as opposed to a few days, and at a fraction of the cost.

While it primarily works with important financial institutions, through them, it can reach out to individuals and SMEs. One particular use case I would like to mention is remittances. Migrant workers, who travel to distant countries in the hope of making a better life for themselves and their families, now endure long wait times and significant cuts from their salaries in the process of sending money back home. This is not the case when the RippleNet is involved.

Ripple helps both large companies and individuals.

How Does it Work?

The RippleNet is a group of network validators - read financial institutions - on the network that utilize the network’s solutions to receive the aforementioned benefits of time and cost savings, as well as getting the additional benefit of liquidity sourcing. In the SWIFT system, messages are sent from one member bank to another until it reaches the destination, whereupon settlement is conducted between the source and destination banks (SWIFT is involved in the actual settlement of funds.)

Ripple works similarly, with members on the network acting as ‘Ripple Gateways’. If a user would like to transfer funds to someone in another country, he or she essentially tells the bank “I would like to transfer ‘X’ amount to ‘Y’ destination.” This money is converted into an IOU, which is represented by the XRP tokens. This information is sent to the destination bank, at which point the XRP representation is converted into the equivalent local currency sum. While the source and destination gateways may not trust each other directly, intermediate gateways can act as trusted recipients and senders for the two parties. It’s akin to the idea of mutual friends.

Unlike the SWIFT system, however, users can send both fiat and crypto funds. XRP may be the native token on the network, but any token can be used, if the payment gateways accept it. XRP is a bridge currency.

Is the RippleNet Kicking Off?

None of this is hoopla. Ripple has proven itself to be a legitimate solution to modern banking challenges, which is why over 200 financial institutions have joined the RippleNet. These members, which I have listed in another published article before, are no small entities and includes central banks, big corporations and some of the world’s largest remittance firms (many of whom have become Ripple’s partners).

Source: Ripple

Ripple has also been mentioned in several reports, including those by the World Trade Organization (WTO) and the International Monetary Fund (IMF). In contrast to a cryptocurrency like Bitcoin or privacy focused coins, Ripple and XRP do not have a reputation for being subversive, which perhaps makes it easier to sway incumbent entities in its favor. Ripple works with current entities - Bitcoin and others challenge it directly. This I believe gives Ripple a strong position for the future.

Conclusion

There is no reason not to invest in Ripple and XRP. The way it tackles serious problems in the payments industry is clever and much needed, more than anything. Banks and businesses will be happy to turn to Ripple for its solutions, which has already established liquidity and create a large network of banks. The ball's already rolling and Ripple is picking up a lot of momentum. Besides Bitcoin and Ethereum, there are few other tokens with as much likelihood of success as XRP.