This is the second article of the series and its a continuation of "Bitcoin and Money". It deals with the history of money along different time intervals.

The origins of money, Prehistory - IV century

In ancient times money played a very different role as we know it today. Before its birth, tribal societies to ensure the persistence of the village, collaborated to each other in primary activities to satisfy the basic physiological needs, such as hunting, gathering food and get a place to rest. The act of sharing was used as a tool to increase the chance of survival of the whole group, hence, first in the personal sphere through parental cares, and then more impersonally through shared resources and circular gifts, people replaced self-sufficiency with more sophisticated ways to exchange value. For example, donations were widely used as a mean of exchange with a sacred connotation: objects of value were used as decorative ornaments, gifts, or to celebrate religious festivities of births and weddings.

However, shared resources and donations were generally characterized by sentimental attachment and were closely tied to kin networks, hence, the possibility to make exchanges was limited by the circle of trusted people. An interesting thing about circular gifts is that, in certain cases, they can be thought as an early form of credit/debt, where the "give and take" of favors was a sort of morally binding accord between parts.

Though, when the range on gifts extended beyond people known personally, and as more individuals found a way to participate in the production of goods useful to others, the invisible hand of the market started to match supply and demand through the process of barter. However, such direct exchange was hardly better than pure self-sufficiency, because with barter little production could be carried on. The two basic problems were "indivisibility" and lack of the double coincidence of wants, that happened when a person desired to sell exactly what the other person wished to buy.

Hence, on one hand, the happy coincidence of wants might happen fairly infrequently between parts if trades were not synchronized - that is, the transaction should happen at the same time, the same place, and the same quantity. On the other hand, barter required some efforts for the calculation of exchange rates between objects. For instance, with two goods there is only one relative price, while with 100 goods there are 4950 prices which make it quite difficult to collect and remember all the information [1].

For these reasons, it was then spontaneously discovered that a more efficient way to exchange goods could be gained using an object as a medium of exchange and unit of account, through what is called an indirect exchange. Under indirect exchange, you sell your product not for a good which you need directly, but for another good which you then, in turn, sell for the good you want [2].

That time was when increased the emergence of money; with money, all the problems of indivisibility and coincidence of wants that plagued the barter society all vanished.

The chosen object as a medium of exchange was characterized by intrinsic value and exploitable utility, indeed the first intermediaries used as commodity money were typically food, such as grain, salt or animal breeding. Furthermore, the intrinsic value of objects resolved the problem found with early credit/debit systems mentioned above, where one could easily betray the agreement between the parts, due to the lack of jurisdiction. However, the mechanism of commodity money had also some limitations: it was constrained by the characteristics of the specific object, which in the case of food was difficult to divide, perishable or cumbersome, and thus, limited to nearby areas.

As a consequence, people needed a better instrument, that might be suitable to maintain value towards time and with better characteristics needed for the calculation of the economic activities. This necessity led to the abstraction of the concept of intrinsic value, followed by its transposition to material objects. Considering metals, they were the perfect candidate to overcome these problems because they were durable over centuries, easier to store, easier to transfer and divisible in small pieces allowing for easier calculations and the specialization of labor.

Though, some metals became more important than others because, apart of their appreciable external characteristics, they were rare to find and expensive to get.

In spite of their natural scarcity, precious metals were well distributed geographically, and, in proportion to most other metals, were easy to extract and elaborate. Indeed, it seems that "there is no center of population which has not, in the very beginning of the civilization, come to desire precious metals, in primitive times for they utility and peculiar beauty as in themselves ornamental, subsequently for plastic and architectural decoration, and especially for ornaments and vessels of every kind"[3].

The natural substance that came closest to these properties was gold, which does not rust, tarnish, or decay. Gold is particular because it is impossible to synthesize from other materials and because it is so chemically stable that it is virtually impossible to destroy [4]. Its authenticity and fineness are verifiable through melting, as it does not stop to shine after being melted. Early on, gold was therefore used both as money and as a metaphor for the divine soul, which is incorruptible and changeless [5], which explains also why this metal was so often used in ceremonies.

Again, the malleability of metals ensured the great characteristics needed to function as money, and besides the fact that metals carried out some limitations in time and space for their saleability, they represented the best trade-off to make high-value exchanges with low cost of transactions, and low costs of hoarding [3]. Indeed, from the economic point of view, the scarcity ensured by precious metals was the solution, not only against perishable stores of values, but also against the depreciation of their relative value. If an object was easily reproducible or inexpensive to get, it would hardly have any value, as long as people found more convenient to produce or counterfeit that "easy-money", than use his own time in more productive activities.

This is the critical point to understand why, at the first place, most tangible physical goods were traded in terms of weight. Weight is the distinctive unit of a tangible commodity, therefore, trading took place in terms of units like tons, pounds, ounces, grams, etc., and gold was no exception.

Clearly, the free market chose as the common unit whatever size or shape of the money-commodity was most convenient. One might sell a coat for one gold ounce in England, or for 28.35 grams in Italy; both prices are identical. It should not be surprising that gold, or other money, were traded in many forms, since their significant feature was their weight. "At any rate, the important thing is that whatever the reason, the free market has found gold and silver to be the most efficient money [2]". Principally, gold was used for important transactions while silver, being relatively more abundant than gold, has been found more useful for smaller exchanges.

The relative supplies of and demands for the two metals determined the exchange rate between the two, and this rate, like any other price, has continually fluctuated in response to these changing forces. However, this ensured for primitive societies a more stable economic system needed for more complicate calculations.

The opportunity to retain value through time thanks to metal money, has enriched the communities of those times: by facilitating trade, motivating efficient production, and allowing the accumulation of capital to undertake large scale projects, weight-money has allowed a deeper specialization in all fields of the economy, with the result of a big jump in the ladder of human progress.

In this way, the independence of gold and other precious metals has consolidated their role of the reserve of value through thousands of years and has extended their role as a guarantee against devaluations.

Money in the Middle Age, V - XV centuries

During history, personal accumulation of properties - hoarding - was often viewed with disdain by religious ethics and governments, and made nearly impossible by redistributive processes designed to meet subsistence of the population. "The image was conjured up of the selfish old miser who, perhaps irrationally, perhaps from evil motives, hoarded up gold unused in his cellar or treasure trove - thereby stopping the flow of circulation and trade, causing depressions and other problems [2]". Furthermore, in most religions, the practice of lending money to other people was seen as an immoral act and called usury.

In these conditions was difficult to reach a consensus on a widely accepted and standardized mean of exchange - a sign of value - and, as a consequence, and because there was no choice, the need to rely on a central authority, that began to coordinate exchanges through the centralization of money issuance.

Perhaps this conception goes back to the King of Lydia which was one of the first empires that issued metal coins towards the sixth century BC, to the time when it was usual merely to certify the weight and the fineness of the metallic materials that universally served as money (Indeed, the English word "money" and the Italian word "soldo" are of Roman origin: in ancient Rome, the word monetor or moneta meant advisor, or a person who warns or who makes people remember [1], while the word solidum derives from the typical hardness of metals).

After some centuries, the minting prerogative of the ruler was firmly established under the Roman emperors, where was developed the concept of sovereignty, for which the right of coinage was one of the most important and essential parts of it.

This step is important from the point of view of the evolution of money because it changes the coin from being a unit of weight, to being a unit of account, which means that there is a difference between the commodity value and its specie value; the difference in these values is called seigniorage.

With this regard, F.V.Hayek, in one of his books titled "Denationalization of Money" wrote:

"As coinage spread, governments everywhere soon discovered that the exclusive right of coinage was the most important instrument of power as well as an attractive source of gain. From the beginning the prerogative was neither claimed nor conceded on the ground that it was for the general good but simply as an essential element of governmental power" [6, pag.29].

In the initial phases of the economic activity, the centralization of power surely lowered the transactional costs of trades by coercing the acceptance of money. The government had also the means to ensure the fineness of the coins by the stamp of its recognized authority, indeed, the genuineness of metallic money "could be ascertained only by a difficult process of assaying, for which the ordinary person had neither the skill or the equipment [6]". These initial advantages, which might have served as an excuse for governments to appropriate the exclusive right of issuing money, certainly did not outweigh the disadvantages of a monopoly system. Hence, besides the fact that minting was an attractive source of revenue for the government, in most cases, central powers used their authority to prevent competition from providing alternative sources of money through compulsion, in a primitive system similar to "legal tender", which, in its strictly legal meaning, signifies a kind of money issued by some entity that a creditor cannot refuse in discharge of a debt (In some countries and in different period in history, the rejection of the government currency was treated as an enemy act and evenly punished with death). Despite never-ending harassment by governments, making conditions highly precarious, private coins have flourished many times in history. In fact, "when the government first began to monopolize the coinage, the royal coins bore the guarantees of private bankers, whom the public trusted far more, apparently, than they did the government [2]".

This is because in the long run, the government centrality carried out two orders of problems. The first problem concerned the power of the monopolist, which acted as a final judge for settlements, to censure inconvenient transactions of individuals, excluding them from the market. Secondly, the control over issuance allowed central authorities to manipulate the ledger in their own advantage. From this possibility, it followed a constant loss of the intrinsic value of the coins, due to inflationary policies used to finance public expenditures and wars, in the attempt to impose value on government coins. Indeed:

"During the Middle Ages, however, the superstition arose that it was the act of government that conferred the value upon the money. This doctrine of 'valor impositus' was largely taken over by legal doctrine and served to some extent as a justification of the constant vain attempts of the princes to impose the same value on coins containing a smaller amount of the precious metal. [...] But the superstition that it is necessary for the state to declare what is to be money, as if it had created the money which could not exist without it, probably originated in the naive belief that such a tool as money must have been 'invented' and given to us by some original inventor" [6, pag.31]

So, the inflation artificially generated from the act of coinage started to be seen as indirect taxation at the expense of the coin users, which had no other way than accepting that currency. Then, the attempt to convince the population that the currency would maintain the same purchasing power over time was a misconception due to forcing its usage rather than the will of individuals. Indeed, imposing a fixed exchange rate on something that derives its roots on personal subjectivity, has been fully displaced by understanding that money is the result of a spontaneous order of such undesigned institution, through a long process of social evolution.

This is because people have the tendency to adapt to circumstances, which means that forcing a behavior will, sooner or later, result in the search for alternative solutions to gain well-being. As proof of this, imposed coins with a defined value were constantly scraped by citizens to obtain flakes of the precious metal that made it up, which contributed to the devaluation of these coins.

Only because of trust placed in a third part was often betrayed, gold and other metals extended as a guarantee against the devaluation of money; this was possible thanks to their natural independence, because of the fact that they were difficult to inflate or censure, and because they acted as bearer instruments (A bearer instrument is a type of security issued in physical form to the purchaser. The holder is presumed to be the owner, and whoever is in possession of the physical object is entitled to payments.).

Thenceforth, thanks to the not very efficient management of the coinage by the state and the following crisis of the Roman Empire, for a long time precious metals were the only alternative that was encharged to compete with government money, which made them last simultaneously with the spread of paper currencies.

After the end of the Roman Empire, towards the XIII century, paper money became known in Europe through the accounts of travelers such as Marco Polo and then was adopted by bankers and merchants in the form of promissory notes, which can be thought as a predecessor to regular banknotes. Indeed, in this century and the following, it could be individuated the historical development of the banking system in Italy, in particular in Venice, Florence and Genoa, which then established many branches in other parts of Europe.

The economic activity was having a reinaissance and in concomitance with the expansion of markets and trades, it was developed the double entry book-keeping, one of the main innovations that provided the elements necessary for the creation of credit and banknotes, which then uncoupled entrepreneurs from feudal constraints [10]. For instance, goods were supplied to a buyer against a bill of exchange, which constituted the buyer's promise to make payment at some specified future date, and deposited gold was supplied by promissory notes, that were redeemable for the same metal in other places.

The main purpose of these methods of payment was its convenience for both issuers and users: its production was a way cheaper and was not constrained by the physical impossibility to divide it into smaller pieces like gold, which made the system of payments more flexible. In turn, merchants got rid of the inconvenience of transporting heavy metals to trade, often subject to robbery, which therefore were deposited for safety with goldsmiths in one town, in change for these promissory notes that could be redeemed in another town. Also because for larger transactions, it was expensive to transport several hundred pounds of gold. After a while, fewer and fewer transactions moved the actual gold, and this early form of credit became both a medium of exchange and a store of value, as long as the bill was endorsed by a credible guarantor and redeemable with gold in a bank.

"Moreover, as banks grew and confidence in them developed, their clients found it more convenient to waive their right to paper receipts and, instead, to keep their titles as open book accounts. In the monetary realm, these have been called bank deposits. Instead of transferring paper receipts, the client has a book claim at the bank; he makes exchanges by writing an order to his warehouse to transfer a portion of this account to someone else, in what is called a check". [2, pag. 21]

In short, money was not so much "used up" as simply transferred from one person to another. In this way, warehouse receipts for money came more and more to function as money substitutes. It should be clear that, economically, there was no difference between a banknote and a bank deposit; both were claims to ownership of stored gold and both were transferred similarly as money substitutes.

So with time, contrary to canonical religious institutions, the richness and success of entrepreneurs acquired the value of religious vocation, where the accumulation of wealth became the sign of God's faith. As a reaction, the emergence of banks and other means of finance then provided the possibility of ignoring the complex social consequences of entrepreneur's activities and credits, which concentrated on their isolated profitability, bringing the birth of protestant ethic and capitalism, towards the XV century [10]. However:

When paper money in various forms begins to be significant, the history of coinage is an almost uninterrupted story of debasements of the continuous reduction of the metallic content of the coins and a corresponding increase in all commodity prices [3].

In fact, at that time, the main problem was not the appearance of a new kind of money with a different denomination, but the use as money for paper claims needed to redeem precious metals.

Money in the Modern Age, XVI - XIX centuries

The development of the banking system spread from Italy to northern Europe towards the XV and XVI centuries. New banking practices and financial innovations promoted commercial and industrial growth by supplying means of payment that were more contingent on commercial needs. Commodity money, that was safely deposited in goldsmith's reserves, was used as a collateral to the nominative notes representative of the quantity of gold or other coins; the goldsmith charged no fee, or even paid interest and applied the discount rate on these deposits (Provided that the buyer was reputable, the seller could then present the bill to a merchant banker and redeem it in money at a discounted value before it actually became due).

The promissory notes issued by the bank were a form of representative money that could be converted into valuable metals by application to the bank, hence, the credit/debit started to become a bearer instrument that circulated as a safer and more convenient form of money. "The receipt entitled the owner to claim his goods at any time he desired, while the warehouse earned profit no differently by charging a price for its storage services [2]".

However, by the end of the XVI century and during the XVII, the traditional banking functions of accepting deposits, money-lending, money changing, and transferring funds were combined with the issuance of bank debt that served as a substitute for gold and silver coins.

In this framework, several banks known as commercial banks specialized in credit creation, while others as issuing institutes which also lent money to institutions and to the government to finance public debt. Since the promissory notes were payable on demand, and the loans to the goldsmith's customers were repayable over a longer time period, this was an early form of fractional reserve banking.

Indeed, Goldsmiths and banks soon discovered that some notes were permanently in circulation so that the gold they represented was never withdrawn. For this reason, banks were tempted to use other people's money to earn a profit for itself; they could lend the excess of reserves or issue additional receipts as loans, in the form of gold money, promissory notes or in the form of checking accounts, until they were trusted to be financially stable and able to redeem metals coins. However, in this way, more warehouse receipts were printed than gold existed in the vaults and hence invalidated because they did not represent 100% of their face value in gold.

"In short, there were some receipts with no gold behind them therefore banks started to be effectively insolvent, since they could not possibly meet their own obligations if called upon to do so [2]".

In this system, issuers of the notes had to keep only a small part of commodity money as reserves - hard cash, that was the quantity necessary to provide liquidity for who wanted to withdraw resources. With the development of markets, however, there were three limits on the advance of the substitution from metal money to paper receipts.

One was the extent that people use these money warehouse instead of gold; if one, for some reason, did not want to use a bank, the counterpart would have to transport the actual gold. The second limit was the extent of the clientele of each bank; the more transactions took place between clients of the same bank, the less gold would have to be transported. Third, the clientele must have confidence in the trustworthiness of their banks [2]. This posed a limitation on the quantity of money a bank could have provided to citizens, which nevertheless had not avoided the huge increase of the monetary base in circulation and the intensification of business cycles during an expansive phase.

This is because of the effect of what is called money multiplier; credits borrowed by entrepreneurs, being effectively money, were deposited in other banks increasing their reserves and, therefore, the power to issue other credits, leading to the expansion of the money in circulation.

At the time when the economy was growing, a large number of credits in circulation initially fostered the market activity, but at some point, these credits should be paid back. With the inversion of the economic cycle - in a phase of recession, repaying loans became more difficult for entrepreneurs, thus, banks were reluctant to give new credit and the monetary base shrank, worsening economic conditions which led to financial bubbles. Since banks issued notes far in excess of the metal reserves they kept on deposit, managing credits in circulation became too complicated, causing the loss in public confidence and loss in faith in the ability of the banks to pay their debts.

When many individuals tried to redeem their gold with banknotes at the same time, if in response a bank could not raise enough funds, it would either go into insolvency or default on its notes; this situation is called "bank run" and caused the bankruptcy of many early banks. These initial financial crises and the use of banknotes issued by private commercial banks led to their gradual replacement by the issuance of banknotes authorized and regulated by national governments and the creation of central banks, with the aim to control and mitigate this phenomenon. This practice continued through centuries until central authorities were granted the sole right to issue banknotes and the power to decide the measure of account for international trades, such for instance in the cases of England, Scotland and later in the United States. Private banks, hence, were prohibited from issuing notes and they could only grant deposits for their customers; the citizens could conceivably make a run on the Central Bank, but this was most improbable.

By the end of the XVII century, the banking activity was also becoming an important source for the funding requirements needed to deal with public expenditures and the combative European states. On the other hand, the exchange rate of gold and silver, known as bimetallism, was imposed by governments in the form of price controls, where they placed a maximum of one type of money in terms of the other, causing shortages - disappearance into hoards or exports- of the currency suffering the maximum price (artificially undervalued), and its replacement by the overpriced money. This is because the market ratio, like all market prices, inevitably changed over time, as supply and demand condition change.

Nevertheless, the development of mechanical physics and scientific discoveries, combined with the huge amount of the monetary base entered in the society with the fractional banking system, in the initial phases of the economic boom allowed for better means of production for entrepreneurs and allowed the born of cultural movements, first with the age of Renaissance in the XV-XVI centuries and then with the age of Enlightenment in the following two centuries.

The responsibility for establishing and regulating the system of money in a country became more and more the matter for governments, but other public or private institutions, such as central banks and the financial system, played an increasingly crucial role in the success of the creation of national currencies [1].

"Yet, purely hard money did not leave too much scope for governmental inflation. There were limits to the debasing that governments could engineer, and the fact that all countries used gold and silver placed definite checks on the control of each government over its own territory. The rulers were still held in check by the discipline of an international metallic money." [2, pag.32]

Which means that, at that time, the banknotes issued by the state were constrained by the reserves of gold, that stabilized the exchange ratio in a system called "Gold Standard" (A gold standard is a monetary system in which the standard economic unit of account is based on a fixed quantity of gold). For a long time, the states held gold reserves in their central banks to ensure the credibility of their currency system [1], with different ratios and influence on different countries. In this system, the governments guaranteed a fixed exchange rate with gold or with other currencies convertible to gold, hence, some countries began to peg their coin units to the gold standards of the most influential nations such as the United Kingdom and the United States.

Meanwhile, social movements led up to the first and second industrial revolutions during the period of transition between manufacture processes to the division of labor and retribution in the form of salary. The rate of the speed of new innovation accelerated, bringing initially the development of steam trains and railroads, which opened the possibility to new trades and reduced considerably the space constraint, and then the mass production of steel and electricity, which further increased the economic activity.

Through the XIX and early part of XX, the Gold Standard was widely used, however restrictions imposed on the issuance of notes were in contrast to the regulation of the monetary policies required by the growing nations, therefore causing heavy fluctuations on the market and forcing some countries to temporarily abandon this system.

"This was the classic cyclical pattern of the nineteenth century; a country's Central Bank would generate bank credit expansion; prices would rise; and as the new money spread from domestic to foreign clientele, foreigners would more and more try to redeem the currency in gold. Finally, the Central Bank would have to call a halt and enforce a credit contraction in order to save the monetary standard. %There is one way that foreign redemption can be avoided: inter-Central Bank cooperation. If all Central Banks agree to inflate at about the same rate, then no country would lose gold to any other, and all the world together could inflate almost without limit. With every government jealous of its own power and responsive to different pressures, however, such goose-step cooperation has so far proved almost impossible" [2,pag.37].

The high leverage of the monetary base caused the loss of most of the hard savings of people, starting a war currency of nations, where the banking system of a country was penalized if not using the fractional system. Indeed, the monetary expansion in one country caused losses of gold to the citizens of other countries, while countries that expanded faster were in danger of gold losses because, in moments of uncertainty, citizens called upon their banking system for gold redemption.

Nevertheless, there was a way to avoid the checks on monetary expansion. Central Banks, by pumping reserves into all the banks, could make sure that they all expanded together, and at a uniform rate. Because all banks were expanding, there was no redemption problem of one bank upon another, and each bank found that its clientele was the whole country. This, of course, ensured that the Central Bank could not fail, since its notes became the standard money. In short, government has finally refused to pay its debts, and has virtually absolved the banking system from that onerous duty. "With every government jealous of its own power and responsive to different pressures, however, such goose-step cooperation has so far proved almost impossible [2]".

Within Europe, economic and military challenges created a system of nation-states, and ethno-linguistic groupings began to identify themselves as distinctive nations with aspirations for cultural and political autonomy. This nationalism would become important to people across the world in the XX century with a strong consolidation of central banks, such for instance the federal reserve, created in 1913.

Then, governments and banks persuaded the public of the justice of their acts; anyone trying to get his money back during a crisis was considered "unpatriotic", while banks were often commended for patriotically bailing out the community in a time of trouble. "Inexorably, the gold flowed into the Central Bank reserves where, more "centralized," it permitted a far greater degree of inflation of money-substitutes [2]".

For instance, in the United States, the Federal Reserve Act compelled the banks to keep the minimum ratio of reserves to deposits and, since 1917, these reserves could only consist of deposits at the Federal Reserve Bank, which means that gold could no longer be part of a bank's legal reserves but it had to be deposited in the Federal Reserve Bank directly.

Governments with insufficient tax revenue suspended convertibility repeatedly, to allow the devaluation of the currency for political purposes or if they faced heavy demand for gold. With the start of World War I, many countries began printing more and more money in order to finance the cost of the war at the expense of all citizens. In Germany, for instance, the number of banknotes issued by the Reichsbank grew from 2,593 million in 1913 to a total of 92,844,720.7 billion banknotes in circulation in 1923 [1], leading to a phenomenon called "hyper-inflation". In other countries, such as the United States, Britain and Italy level prices doubled, tripled and quadrupled respectively.

With more money circulating, most countries suspended the convertibility of their currencies into gold in 1914, as its increased quantity was no longer balanced by the national gold reserves, and recovered towards 1927, in a period of relative stability, but also subject to deflation. This state of affairs, with the expansion of credits/debts, jointed with banking crisis and the low levels of economic activity due to high unemployment, led the 29 of October 1929 to the great depression, when the ongoing national rivalries exacerbated the economic turmoil forcing again countries off the gold standard (As an example of the pressure of monetary policies, after the crisis, the American president Roosevelt in 1933 emanated the executive order 6102 which declared illegal and prosecutable the possession of any form of Gold.), and helped precipitate into the world war two.

After the second world war, the influence of governments on central banks increased, becoming the principal instrument to sustain government policies for their goals. Nevertheless, this system was revived again at the 1944 international conference held in Bretton Woods, where nations agreed upon pegging their currencies to the US dollar, the only currency convertible to gold at a fixed price of 35 USD per ounce [1]. The Bretton Woods monetary system is therefore sometimes called the Gold Exchange Standard, where trade imbalances were corrected by gold reserve exchanges or by loans from the International Monetary Fund, an institution created for that purpose.

Finally, in recent history, this system was abandoned again leaving space for fiduciary money (fiat), which is accepted as a legal tender, although many central banks still held substantial gold as reserves. Since the creation of the Federal Reserve, one century ago, the US dollar has lost over 90% of its purchasing power, but other currencies have performed worse.

Money in Contemporary Age

In 1971, under the United State's presidency of Richard Nixon, the Gold standard collapsed definitively declaring the end of convertibility of banknotes to precious metals and leaving the space only for fiduciary money - fiat money, which is money without intrinsic value and regulated by governments and monetary institutions with the aim to be a unit of account with a stable value [1].

With fiat money and the actual banking system, few improvements are developed in the modern system of payments and money. As we have seen, through history, the cheque, an instrument comparable to the bill of exchange, took the function of clearing instrument between parts, managing liquidity of deposits. Then, the information revolution which brought computers and the internet, made cheap to store this unit of account or to pay bills electronically, finally substituting cheques with debit cards, credit cards or prepaid cards.

Another form of electronic money is often referred to "e-money", which can be connected with these cards and, starting from 1990, has been used on the Internet to purchase goods or services. "A consumer gets e-cash by setting up an account with a bank that has links to the Internet and then has the e-cash transferred to her PC, which could use to buy goods and services [8]".

However, since 1971, modern money is preeminently state-money all over the world, and the liabilities of state central banks acquire the status of "valuata money" or base money, because of the coercive power of the state, and in particular its ability to levy taxes on its citizens payable in its own currency.

The main purpose of controlling the money supply is to allow agents in a currency area to calculate things such as the costs, prices, wages and income, in the same units of money, thereby improving the reliability of the value of money. A central bank introduces new money into the economy by purchasing financial assets, lending money to financial institutions or by controlling the interest rates, expanding the total reserve of the "broad money". By virtue of its monopoly, a central bank is able to manage the liquidity situation in the money market and influence money market interest rates. This allows deciding on the level of short-term interest rates to ensure that inflationary and deflationary pressures are counteracted and that price stability is maintained over the medium term [1].

So when commercial banks need banknotes for their clients, because they and have to fulfill minimum reserve requirements (i.e. deposits) with the central bank, they could ask a central bank for credit. The monetary base is at the liability side of the central bank and composed by several monetary aggregates, that as a whole define the money supply. Because central bankers are not totally in control of the supply of money and because they cannot be sure which of the monetary aggregates is the true measure of money, each one decides a general definition of broad money.

For instance, the Federal Reserve defines the money supply as "a group of safe assets that households and businesses can use to make payments or to hold as short-term investments", where the U.S. currency and balances held in checking accounts and savings accounts are included in many measures of the money supply [9].

There are several standard measures of the money supply considered by the Fed, including the monetary base, M1, and M2:

- The monetary base: the sum of currency in circulation and reserve balances (deposits held by banks and other depository institutions in their accounts at the Federal Reserve).

- M1: the sum of currency held by the public and transaction deposits at depository institutions (deposits from the public, savings and loan associations, savings banks, and credit unions).

- M2: M1 plus savings deposits, small-denomination time deposits (those issued in amounts of less than $100,000), and retail money market mutual fund shares.

These measures are changed through time, contemporary to the exploration of new tools raised by the banking sector. Indeed, the increasing demand for financial instruments gradually led to high fluctuations in interest rates. This change in the economic environment would have stimulated a search for profitable innovations by financial institutions that might have helped in lowering the internet rate risk. "Two examples of financial innovations that appeared in the 1970s and that confirm this prediction are the development of adjustable-rate mortgages and financial derivatives [8]".

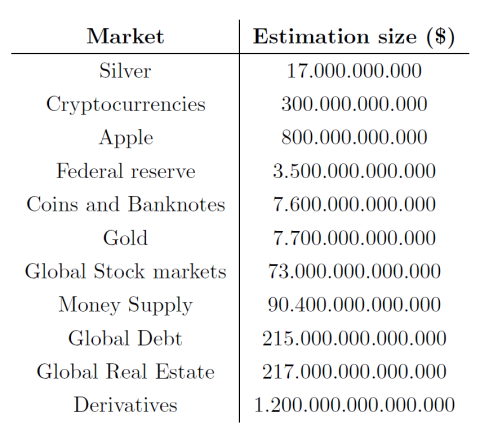

These values are taken from the infographics of a reaserch project published by Jeff Desjardins [7].

A derivative is a contract between two or more parties that derive its value from the performance of an underlying asset, index, or entity; some examples of derivatives are the futures contracts, the forward contracts, options, warrants or swaps [7]. These kinds of contracts, along with developments on finance, are increased exponentially compared to the size of the real economy and the exact amount of this market is not known and could be only estimated. To understand their dimension and the dimension of the monetary base, we could compare the capitalization of different markets around the world, which are shown in the above table.

In this regard, collateralized debt obligations and credit default swaps are two derivative types that are now famous for their roles in the 2008 financial crisis, when the whole system has shown to be broke; with the failure of the Lehman Brothers, it followed a waterfall of defaults, leading to the collapse of the world financial system and to the biggest crises of all times, until now.

Index:

- Cryptocurrencies for friends who don't care about cryptocurrencies

- Bitcoin and money

- The history of money

- The characteristics of money

- Economic thought

- Technological development before Bitcoin

- The white paper

- Building blocks of the blockchain

- The Nakamoto consensus

- Some crypto-economics

References:

[1] - European Central Bank. Why price stability.

[2] - M. Rothbard. What has government done to our money?

[3] - C. Menger. The Origins of Money.

[4] - S. Ammous. The Bitcoin standard.

[5] - C. Eisenstein. Sacred Economies. Money, gift and society in the age of transition.

[6] - F.V.Hayek. Denationalization of money.

[7] - J. Desjardins - All the money and markets in one visualization.

[8] - S. Mishkin. The economics of money, banking and financial market.

[9] - Federal Reserve. What is money supply?

[10] - W.S. Andersen. A theory of social and economic evolution