A user’s view on the DeFi jungle

After the DeFi deep dive in part 2 and 3, we’ll now touch the surface again and delve into the (retail) user’s perspective on DeFi.

As you’ve seen it’s quite a “jungle” of DeFi opportunities out there. Sometimes, it is really hard to keep the overview. Let me try to pave your way through that jungle…

Photo by Maggie Collins on Unsplash

Photo by Maggie Collins on Unsplash

Let’s start with some tools and apps that really help with orientation.

Tooling for DeFi

One of my favorite DeFi tools is Zapper. Zapper first caught my attention with their DeFi Tutorials newsletter, but gradually created a site that I wouldn’t want to miss anymore. Zapper is not only valuable for DeFi investors — it helps with the management of Ethereum wallets in general.

With Zapper, you can just target an Ethereum address (it doesn’t have to be your own), analyze its token holdings and its involvement into different DeFi projects, liquidity pools and yield farms. Zapper supports all the major DeFi projects we discussed in parts 2 & 3 of this series, like e.g. Uniswap, SushiSwap, Curve, Yearn, Bancor, Synthetix and 1inch.

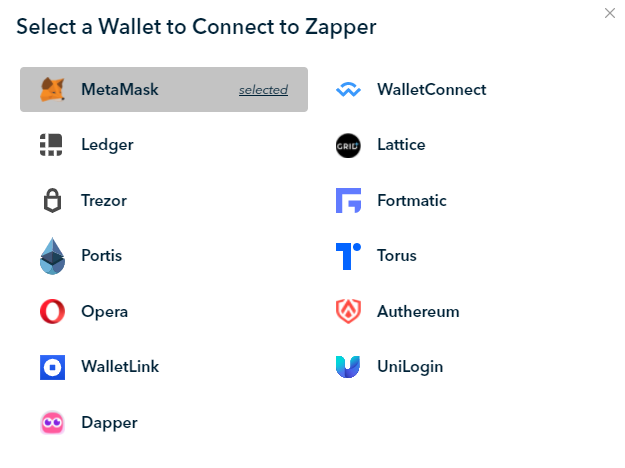

You can also work directly with all kinds of wallets like web, mobile, hardware and even smart contract wallets like Authereum.

Zapper supports all relevant kinds of ethereum wallets.

Zapper supports all relevant kinds of ethereum wallets.

A very handy Zapper feature is its bundling: You can add several Ethereum addresses and Zapper merges all your positions from different accounts together into one nice view — this works even for your transactions. That feature alone is worth a try.

Maybe the coolest thing: You can directly invest via Zapper’s slick UI. In some cases, Zapper offers even more input options than the underlying projects themselves. Always to your convenience: Zapper wraps or converts your tokens into the right one expected by the liquidity pool.

If you want to dive a bit deeper I recommend this Zapper tutorial by DeFi Dad:

Another solid alternative to Zapper is Zerion. Also a very nice user interface, simple and intuitive. You should give it a try!

I’m sure: Projects like Zapper and Zerion will attract more and more end users into DeFi.

Mobile options

By the way, DeFi isn’t restricted to a desktop experience and web sites. For security reasons, I’d always recommend to work with hardware wallets if you invest significant amounts. But you certainly can go mobile.

One of the most impressive mobile DeFi apps is Argent. It’s a mobile crypto wallet with very interesting social features — and an impressive on-ramp for DeFi projects — supporting some of the most prominent options.

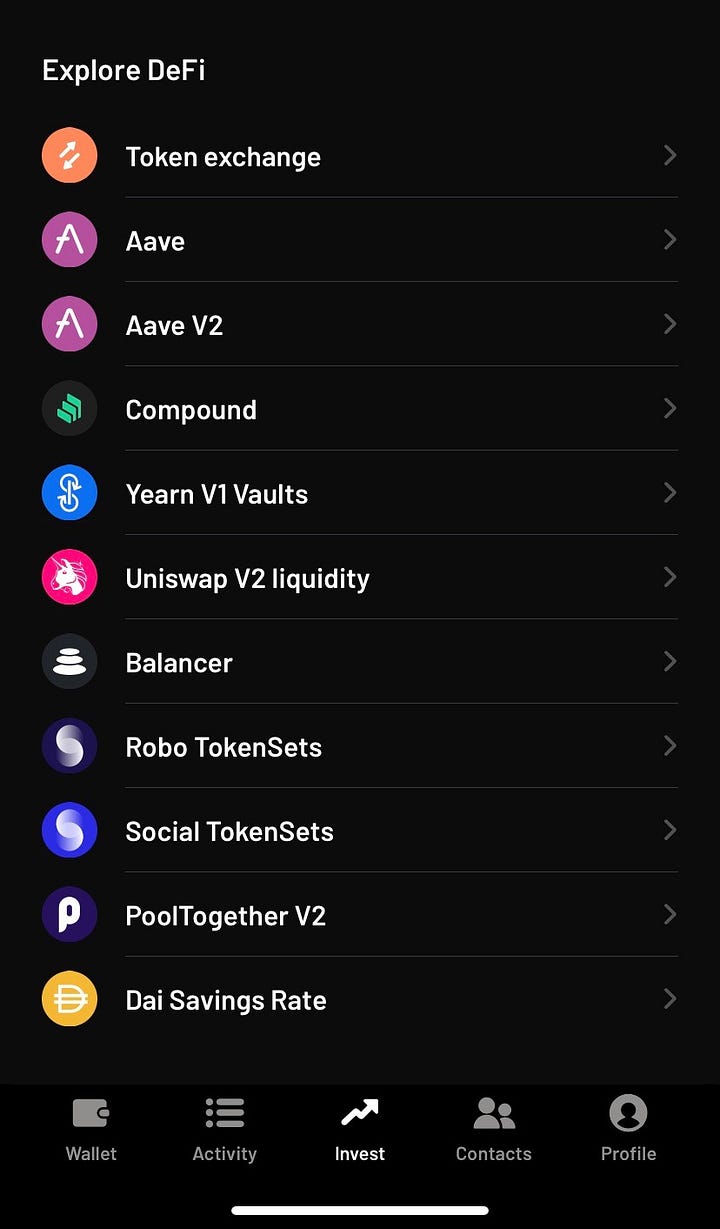

Sometimes, a screen-shot might say more than a thousand words. If you read through the earlier article parts, these project names should ring a bell:

Mobile app Argent supports a lot of DeFi projects

Mobile app Argent supports a lot of DeFi projects

I expect most of the popular mobile crypto wallets to enter the DeFi space very soon.

The cost-side of DeFi

While everybody in DeFi talks about high yields, there is certainly significant cost involved that gets often neglected. You’ll rarely read about that aspect on most DeFi pages. In the end, we are in blockchain-land — and blockchain transactions cost money — sometimes serious amounts money — especially for retail investors. DeFi is currently thriving on Ethereum, so we have to consider Ethereum’s transaction costs and native gas price. These costs fluctuate.

In times of high traffic like now (2020–12–29), we talk about a gas price of 40–100 gwei (find more on gwei here). That easily results in transaction costs between 5 and 10$ for normal trades. DeFi transactions with more complex smart contracts are usually a bit more costly (transaction cost on Ethereum is determined by code complexity of the involved smart contract functions).

In theory, you’ll have at least three transactions per DeFi investment that you have to trigger and pay for:

- Usually you need to approve a token on a DeFi project’s smart contract before you can invest. (This is usually a bit cheaper than the rest)

- Then, you send tokens to the DeFi smart contract (start of investment).

- At the end, you fetch back your returns.

That alone would mean an investment of 10–20$ at current price levels.

In practice, you’ll have many more transactions.

Remember the yield farming examples from part 3?

- If you stake your LP tokens to earn more yield — that’s another transaction.

- If you vote on the DeFi project’s DAO — that’s a transaction.

- If you want to fetch additional rewards — these are usually (recurring) transactions — often weekly like on Synthetix.

So, if you are cautious and don’t bet too much money on the one “DeFi horse” (which I would always recommend — especially for beginners) these transaction costs can easily eat up all of your yield.

So, the simple strategies like splitting up your investment and spreading smaller sums across many different DeFi projects won’t lead to higher yields. You will certainly minimize risk and learn a lot, but cost might easily spoil the fun.

Speaking of risk — it’s about time to work on that topic…

The risks in DeFi

Photo by

Photo by The possibilities to generate yield with DeFi are endless.

The same is true for the participants’ risk exposure.

So, let’s discuss some of the risks investors are about to take. Later we’ll discuss some potential mitigation strategies.

1. As we’ve discussed, DeFi projects are very(!) young. All these projects use smart contracts that are managing large amounts of valuable assets. Because of the enormous competition, test cycles are very short. These systems are obviously an intriguing target for attackers who constantly try to find vulnerabilities. Yes, most of these projects undergo security audits, but in the end it is freshly written software — and software always has bugs (I’ve been a programmer — please trust me with this statement). These risks are obvious and you’ll regularly read about DeFi hacks like in this article summarizing the most prominent DeFi hacks in 2020. Please do inform yourself carefully before you invest any serious money.

2. Another dangerous aspect in DeFi is its ultimate strength: The ability to “plug and play” and interact via tokens between different DeFi projects is at the same time increasing the attack vector. It’s nearly impossible to test all possibilities. Some hacks go exactly in that direction. Hackers can also “plug and play” their attacks — especially with new concepts like flash loans.

3. Besides the obvious risk with malicious actors like hackers, DeFi also handles “young assets” like we discussed with e.g. governance tokens. It is yet to be seen what their true market value is once incentive programs have run out and which platforms thrive.

4. Then there are the regulatory risks. Government institutions might sue certain projects (like we just saw with Ripple) or freeze accounts if projects are not truly decentralized. That might hit even well-known and widely trusted projects like Tether’s $USDT or Circle’s $USDC — es you can see here.

5. And finally, you need to consider tax issues which are very different depending on your country of residence — but very relevant. Most interactions with DeFi projects might be “taxable events” in your jurisdiction. It is very wise to think about that early on, keep track on every step you take and search professional support.

Risk mitigation

Of course, there are interesting mitigation strategies for most of the risks mentioned above. Ever thought about insurance? Projects like Nexus Mutual help to cover users’ risks in smart contracts and custodians. Yearn just announced close cooperation with Cover protocol — another smart contract insurer (who themselves suffered from an exploit while I am writing this article — crazy).

Nevertheless I’m sure: We’ll see a lot of innovation in insurance — driven by DeFi. (Remember: we now got tokens, can use them as containers for insurance policies, trade them etc.).

Screenshot from Nexus Mutual

Screenshot from Nexus Mutual

In general, it is dangerous to invest in the hottest newest projects with the highest APY. Always remember: You’ll get a high APY because you expose yourself to high (asset/platform) risk.

It’s always a good idea to double-check the coverage rate for a DeFi project on platforms like Nexus Mutual — even if you don’t intend to buy coverage. You’ll easily see the maturity of the project (high coverage cost usually means “young DeFi project”).

It’s also wise to choose proven and somewhat battle-tested decentralized assets, like $ETH or $DAI for your first DeFi adventures. Remember: these DeFi projects will try to lock you in with your investment. So, plan for the long-term and chose solid base assets.

But, no matter how careful you choose — you won’t eliminate all the risks luring in a young industry that handle millions and billions of dollars…

Heads up

Photo by

Photo by That’s it for part 4 . We‘ve covered again quite some ground. I hope you’ll give some of the tools a look — or even a try. It’s definitively worth it!

In the meantime, I’ve published the following articles in this little series:

- Part 1: How DeFi will innovate our financial ecosystems (Intro)

- Part 2: The rise of DeFi

- Part 3: The amazing parts of DeFi

- Part 4: The user's view on the DeFi jungle

[this article] - Part 5: DeFi opportunities for retail banks

- Part 6: DeFi lessons for Central Banks

- Part 7: Bringing it all together

Disclaimer: This article is not intended to be an investment advice of any sort. Do your own research and search for professional support if you intend to invest in one of the projects mentioned in this article.

Further reading: If you liked this story, you might also want to check out the start of this series or my earlier work about “Democratizing the digital markets” or “DeFi — an ecosystem made for whales?!?“

You are also welcome to follow me on Twitter or get in touch via LinkedIn (but please tell me your reason to connect and how you found me).