Bringing it all together

By now, we’ve covered DeFi full circle and brought many pieces together. I tried to pave your way on that bumpy road. You still need to walk carefully, but you should have collected basic knowledge about DeFi.

Photo by Jeffrey Blum on Unsplash

Photo by Jeffrey Blum on Unsplash

Firstly, we analyzed the increasing pressure from blockchain-born tokenized currencies and financial instruments upon the existing financial ecosystems. We’ve seen pressure coming from different angles and bringing fundamental change to financial markets.

Secondly, we dived deep into different DeFi use cases and their characteristics. We analyzed several DeFi ingredients, starting from borrowing and lending over AMM and liquidity providing to “stable swaps” and yield farming.

Next, we went up again. We took the point of view of a DeFi (retail) user and gave orientation in that DeFi jungle. We had a look at several tools and discussed the major risks involved with DeFi and what to do about them.

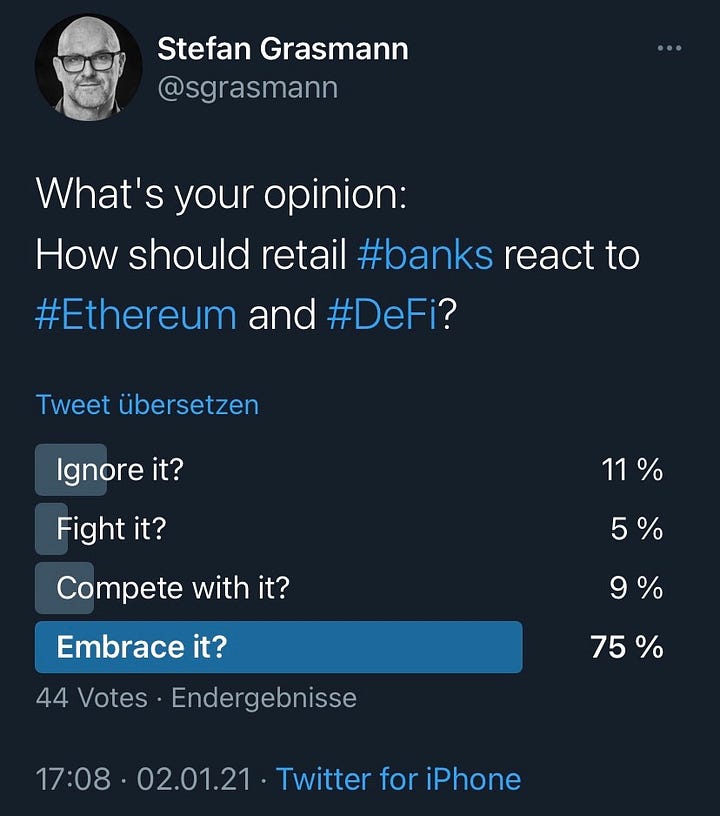

Then, we took the perspective of retail banks: What to do about DeFi?

Ignore it? Fight it? Compete with it? Embrace it?

My twitter bubble agreed to my arguments:

Finally, we even asked the crazy question: Isn’t this DeFi infrastructure suitable as foundation for central banks and their future currency? We saw, this could be an option.

In the meantime…

It took me about four weeks to write this series. In the meantime, interesting things are happening — paying into many of my statements:

Transaction costs are rising significantly on Ethereum. It’s even more problematic to “try out” DeFi with small amounts of money since transaction costs easily eat up big parts of your potential profits.

Scaling solutions like optimistic rollups (discussed in part 6) now gradually go live with their layer two solutions for Ethereum. DeFi projects like Synthetix move their staking features and reward distribution to layer two. This reduces transaction cost dramatically and makes their product more attractive for small investors.

Meanwhile, “traditional finance” splits into two camps: Those like JP Morgan predicting Bitcoin at hundreds of thousands of dollars — and those like UBS claiming that crypto investors might lose all their money.

We note: things are getting interesting now! More and more people start to understand that this innovation is hard to neglect any longer.

…one more thing

I hope you’ve enjoyed our ride through these seven articles and that you’ll take away some new ideas what you could make out of all of this for yourself. I would be very happy if you felt the urge to try something out for yourself, and if you understood the underlying reasons why all of this has immense power. Let’s reiterate on that:

Photo by Kaique Rocha from Pexels

Photo by Kaique Rocha from Pexels

This new financial world is open by default, anyone can join. This is not only a mindset, but it’s also built deeply into the technical foundations. There is a blockchain, yes. But that in itself is not enough! Standardized tokens upon these blockchains are THE THING! They are already used as digital currency, but also for access to certain features, rewards, governance, voting. They enable financial “plug&play” (remember money legos from part 2). They drive an enormous competition — and ultimately innovation at breakneck speed. Combine that with open source. Add the transparency of smart contracts — everyone can see their competitors’ on-chain code.

All of that results in an open innovation arena we’ve probably never seen before.

We currently see the impact of token ecosystems upon the investment area. It will certainly impact all financial instruments and money systems. I’m sure it will spread further to neighboring industries:

- We already witness that access to data gets packed into data tokens and sold via new data marketplaces leveraging DeFi tools like Balancer.

- We already see digital art backed by tokens and linked to DeFi.

- We already see gaming assets packed into tokens and sold via DeFi.

- We already see real estate that gets tokenized and sold on DeFi tools like Uniswap.

- We will see standardized insurance policies packed into tokens and used as collateral in DeFi.

Maybe most of this will be gradually abstracted away from everyday users. But it is certainly a superpower if we understand how blockchains and tokens work, if we’ve witnessed tokens transact on Etherscan and roughly understand what’s going on behind the scenes. It will be as beneficial as it is to know how the Internet works.

Photo by

Photo by The end

That’s it. You should by now be ready to get your own hands “dirty” with DeFi and start your own experiments. 👍

- Part 1: How DeFi will innovate our financial ecosystems (Intro)

- Part 2: The rise of DeFi

- Part 3: The amazing parts of DeFi

- Part 4: The user's view on the DeFi jungle

- Part 5: DeFi opportunities for retail banks

- Part 6: DeFi lessons for Central Banks

- Part 7: Bringing it all together

[this article]

Disclaimer: This article is not intended to be an investment advice of any sort. Do your own research and search for professional support if you intend to invest in one of the projects mentioned in this article.

You are also welcome to follow me on Twitter or get in touch via LinkedIn (but please tell me your reason to connect and how you found me).