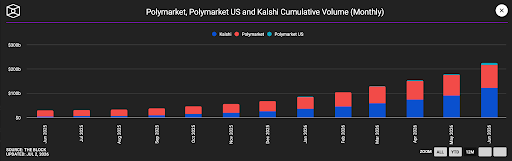

Prediction markets closed out June with the biggest month in the sector's history. Combined trading volume across Kalshi, Polymarket, and Polymarket US reached $44.8 billion, up 75% from May's $25.66 billion, according to The Block, with the FIFA World Cup doing most of the heavy lifting. Kalshi took the larger share by a wide margin; the platform’s June volume alone hit $31.5 billion, up 87.4% from $16.81 billion in May.

Image source: The Block

The volume is retail and World Cup-driven, but the same week offered a live case for why institutions ought to be watching closely: on June 15, a $64 million match market on Spain repriced real-time from favoring La Roja at 92% to zero after a shock 0-0 draw with Cape Verde, pricing information more efficiently than Goldman Sachs' own pre-tournament forecast model.

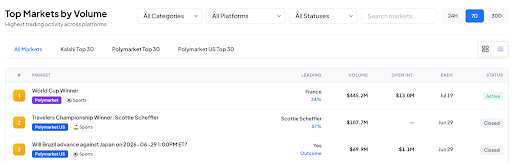

That said, liquidity depth remains one of the sector’s main institutional hurdles. Polymarket’s World Cup winner market recorded $445 million in trading volume over the past week, yet that turnover does not necessarily translate into executable size at a single price.

Image source: DeFi Rate

For larger institutional players, the question is not whether a market can generate headline volume during a global event, but whether they can build, hedge, and exit meaningful positions without materially moving the order book. That capability is improving, but it remains uneven outside the most heavily traded contracts.

Who Owns the Stack

Last week's story was prediction markets finding institutional distribution: Cboe listing exchange-cleared contracts, Tradeweb piping Kalshi data to institutional desks, Meta reportedly exploring the category. This week gave us the consumer-side version of that story.

The contest is evolving to which part of the stack each platform chooses to own; the customer relationship, the exchange, the data feed, the resolution process, or some mix of all four.

Meta foray into the space through Arena is a revealing example. NPR reported that Mark Zuckerberg discussed acquiring Kalshi last year before talks stalled, and that Meta is now building a standalone prediction product called Arena. But Arena is not currently positioned as a real-money exchange. According to the report, users would make play-money forecasts on news and online trends, while Meta’s AI systems would generate questions and determine outcomes.

That distinction matters. Meta does not need to own a regulated exchange to own discovery, attention and participation. A points-based product can turn prediction into a social and engagement layer first using the company’s distribution, behavioural data and AI systems to build the user habit before any real-money product enters the equation. The exchange, in that model, becomes an optional back-end rather than the starting point.

Meanwhile, DraftKings announced the launch of an in-house proprietary prediction markets platform dubbed DKeX. The move takes prediction markets further inside the company’s own product and regulatory infrastructure. DraftKings already has the sports audience, brand recognition and live-event engagement that standalone exchanges spend heavily to acquire. Owning the venue gives it more control over contract design, product iteration and the economics attached to that flow.

Then there's a third route: don't build the exchange, just plug into one. On June 29, London-listed broker Plus500 added CFTC-regulated Kalshi sports contracts to its US platform. Plus500 keeps the customer relationship and trading interface; Kalshi keeps the exchange underneath. It's a different bet than DraftKings' more order flow for Kalshi's existing infrastructure, rather than another proprietary venue splitting liquidity away from it.

World's launch inside Phantom as a fully on-chain prediction market is the crypto-native version of the same idea. Instead of acquiring users through a sportsbook or broker, World meets them where their wallet already lives; custody, trading, and identity in one place, with the wallet itself doubling as the front end for discovering and settling markets.

Kalshi, meanwhile, pursued the more familiar media-and-sport route this week. The company’s partnership with ADI Predictstreet puts the brand across World Cup stadium, television and online placements, alongside a co-branded tournament hub.

One catch worth noting in today’s letter: distribution rights do not automatically create a complete trading product. Polymarket’s recent Bundesliga partnership illustrates the point. The platform has secured U.S. branding rights, but the official data arrangement required for deeper live-market coverage has not yet been announced. As Finance Magnates noted, brand access and official data are separate assets; the latter can determine how many markets a platform can list, how quickly it can resolve them and how useful they are in-play.

Polymarket’s Investigation Tests the Federal Model

Two weeks ago, the Wall Street Journal's investigation into Polymarket's paid-creator campaign that reportedly featured dummy trading sites, undisclosed payments, videos depicting wins that would have been losses on the real platform raised the question of whether regulators would act. They now have, with the CFTC opening what's being described as an extensive investigation into Polymarket.

Congress is applying its own pressure in parallel. Sens. John Curtis (R-UT) and Adam Schiff (D-CA) sent a letter to CFTC Chair Selig, calling the fake-bets allegations "deeply troubling" and pressing on advertising standards, influencer-disclosure rules, age verification, and whether the agency has adequate tools to oversee the sector at all.

That it's bipartisan, and comes from senators outside the usual crypto-policy circle, suggests the marketing-practices question is no longer a niche concern.

Prediction-market operators have built their central regulatory argument around federal oversight: event contracts, they argue, belong under the CFTC rather than a patchwork of state betting rules. But that argument becomes harder to sustain when the customer-facing product looks indistinguishable from the kind of aggressive gambling promotion states are used to regulating.

Polymarket says it is auditing active promotional content but the real test is whether that produces visible changes. If the sector wants to be treated as financial-market infrastructure, that means its marketing standards, like its prices, surveillance and settlement, are about to be judged by the same credibility test, with a July 10 deadline as the next checkpoint.

Three States, Three Different Answers

While the CFTC works through its new federal framework for event contracts, states are already building their own answers and they are not all choosing prohibition.

Michigan took the hardest line this week. On June 29, a state judge granted a temporary restraining order blocking Kalshi from offering sports-event contracts to Michigan residents, making it the second state after Nevada to secure a court-ordered halt. Kalshi must now geofence Michigan users while the case proceeds, and says it will challenge the ruling.

North Carolina is testing a different model with its newly proposed budget that includes a proposed 6% tax on prediction-market operators’ net trading-fee revenue, while allowing CFTC-registered platforms to operate without a separate state licence. The measure is not yet final law, but it is notable because it treats prediction markets neither as fully exempt federal products nor as illegal gambling: it accepts their presence, then taxes them.

Kentucky sits at the other end of the spectrum. After the state moved against Kalshi, Polymarket and other operators, including through a new 14.25% excise tax, the CFTC itself recently sued Kentucky to stop enforcement of its gambling laws against federally regulated exchanges. Kentucky is the ninth state the agency has taken to court in defence of its claim to exclusive jurisdiction.

These developments reveal an important structural shift. The question is no longer whether states can slow prediction markets down. They already are through injunctions, taxes and litigation. The question is whether the eventual federal framework can create enough consumer protection and legal clarity to prevent every state from writing its own version of the rules.

For now, the market is scaling nationally while regulation is fragmenting locally and that gap is becoming one of the industry’s most important structural risks.

A Reminder the Infrastructure Is Still Young

Amid the volume records and valuation talk, Polymarket was also hit by a front-end supply-chain attack. A compromised third-party vendor injected malicious code into the platform’s website, leading users to approve fraudulent transactions. Independent estimates later put losses at roughly $3.1 million; Polymarket has said it is refunding affected users in full.

It is a smaller story than the regulatory pressure or the distribution race, but it is a useful check on the growth narrative. A sector now generating $44.8 billion in monthly trading volume still depends, in places, on third-party front-end infrastructure vulnerable enough to turn a website visit into a loss of funds.

The World Cup has shown that prediction markets can scale demand. The weeks since have shown the harder task: scaling the systems around that demand – liquidity, distribution, marketing controls, regulation and security – quickly enough to deserve it.