There is very little time left in the year. It is now time to talk about the investment themes of 2025. Apart from conspiracy theories, there is a nice article from The Economist’s famous ‘The World Ahead’ series about the themes and sectors that may stand out in 2025. Let’s dig a little here. Even if a new war zone does not emerge in 2025, current geopolitical tensions will continue to affect the global economy. The weak growth trend will continue. World GDP is expected to grow by only 2.5%. While European economies are expected to strengthen, developing economies will have a stagnant year due to trade wars, climate change and technological challenges. Inflation and interest rates are expected to fall, but high public debt and defense budgets will limit governments’ spending capacity.

The Economist’s 10 themes are as follows:

Low Inflation and Increased Consumption: Falling inflation is encouraging central banks, including the Fed, to cut interest rates even further, encouraging consumers to spend.

AI Investments Accelerate: As IT spending rises to $3.6 trillion, companies are turning to AI technologies. Nearly 30% of large American companies are investing $10 million or more in AI. That rate was 16% in 2024.

A World Population Aging: While the population over the age of 65 has reached 12%, only 10% of global GDP is spent on healthcare. As human life expectancy increases, the need for healthcare investments is increasing.

Green Transformation and Energy Transition: Governments are supporting comprehensive green projects. While renewable energy sources are rapidly increasing, fossil fuels still meet more than four-fifths of energy needs. Low energy prices are the biggest obstacle to the energy transition.

Electric Vehicle Growth: The EV theme is the shining star of the automotive industry. However, range anxiety is driving many buyers to non-plug-in models.

Carbon Commitments in Airline: Airline orders are increasing at a time when airlines are pledging to reduce carbon emissions. With the number of international tourists reaching 1.6 billion, tourism accounts for 5-8% of all greenhouse gases.

Housing Market Concerns: Housing markets are on the radar of policymakers and regulators. While house prices are high globally, they are falling in China.

Green Policies and Metal Demand: Global metal prices are up 7.5%, driving demand for everything from car batteries to cables. This is creating high demand for metals such as copper and steel.

Infrastructure Spending is Increasing: Environmental targets are driving infrastructure investment worldwide. Fixed capital investment has reached $28 trillion, accounting for a quarter of global GDP.

Green Transformation in Shipping: The shipping sector is including 40% of its carbon emissions in the EU’s emissions trading system. Additionally, geopolitical developments affect the maritime industry.

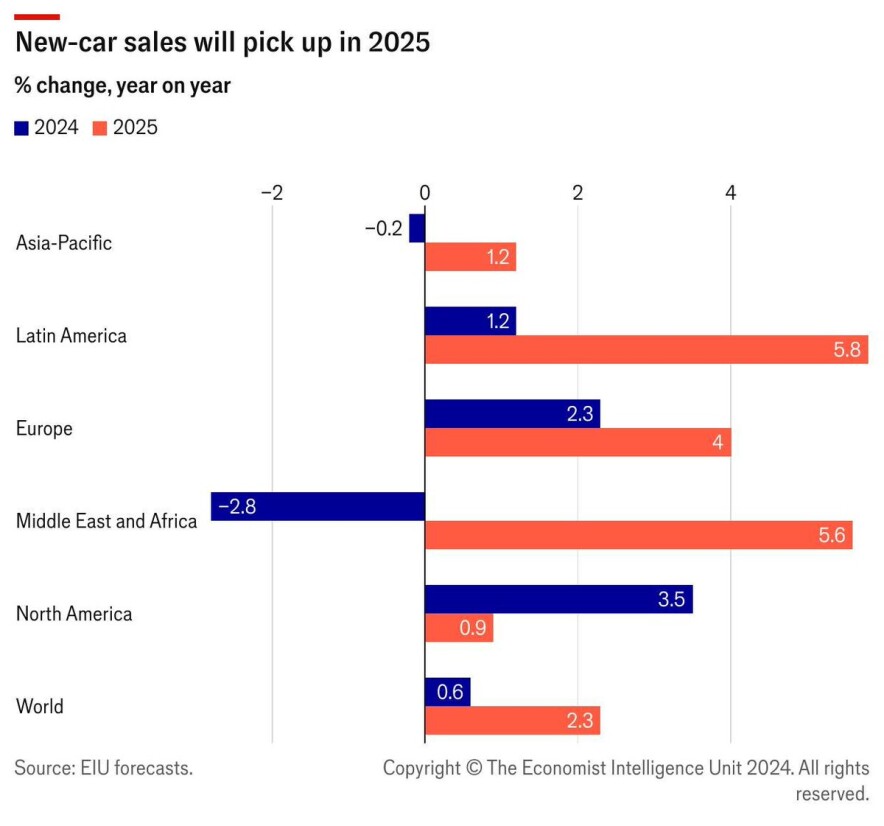

Let's go into detail about the sectors. They started with automotive. After the recession in 2024, global new vehicle sales are expected to increase by 2% in 2025. Truck sales will increase by 4% due to infrastructure projects. Although electric vehicle sales will increase by 25%, high prices and range concerns will direct many buyers to traditional models.

Emission reduction efforts will remain in focus. Norway will be the first country to aim for all new vehicles to be emission-free by 2025. China will exceed its targets in this area by achieving half of global electric vehicle sales. Chinese manufacturers will gain strength internationally. For example, BYD aims to sell 1 million vehicles outside of China, while VinFast will focus on the Indian and Indonesian markets. However, the high tariffs applied to Chinese vehicles complicate the plans.

In the West, companies such as Volkswagen and Tesla will develop more affordable electric vehicle models. The year 2025 seems to be the scene of significant changes in terms of green transformation, new technologies in automotive, and global economic balances.

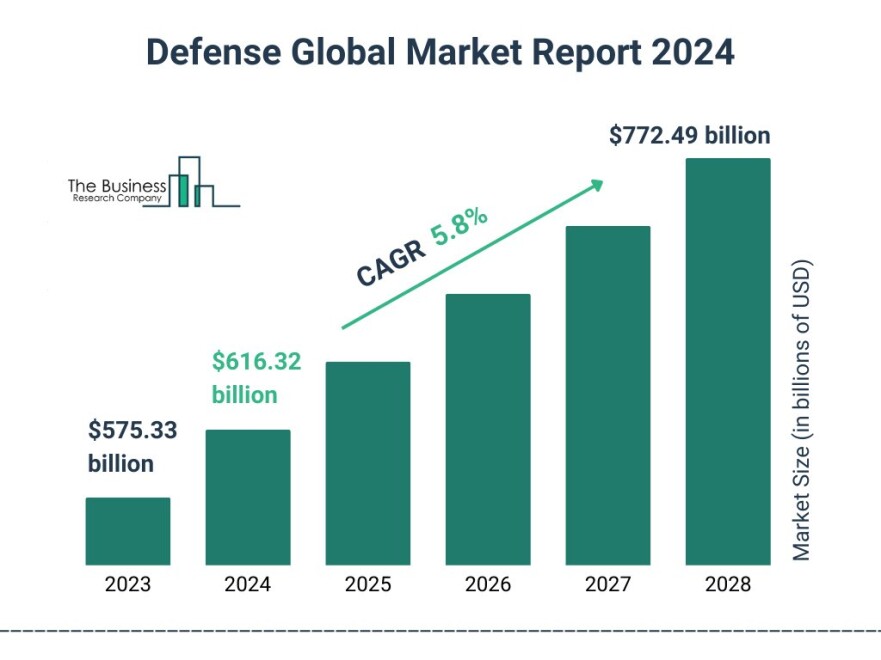

One of the themes I believe in in 2024 was the defense sector, I'm sure some will remember. I've mentioned it many times both here and in publications. We will also talk about defense spending in 2025.

The wars in Ukraine, Lebanon and Gaza are expected to increase the demand for weapons, but defense spending will not be distributed equally among countries. The US, which has the world's largest defense budget, will increase its military spending by 4% to $884 billion. However, China, as the second largest defense spending country, will increase its budget faster.

NATO will discuss exceeding the current 2% GDP defense spending target set for member countries and increasing it to 2.5%. However, one-third of the member countries could not even meet the current target. The alliance will prepare a comprehensive strategy against Russia and provide $43 billion in support to Ukraine. In contrast, Germany plans to halve its aid to Ukraine in order to save money. The EU, concerned that the US's commitment to NATO may weaken, will give more importance to defense.

In 2025, defense and military spending will reshape global geopolitical balances. Increased military activities, especially in NATO and the Asia-Pacific region, will trigger advances in defense technologies and broader strategic steps. While the US continues to maintain its strong stance, moves by China and other regional powers will keep tensions high on the world stage.

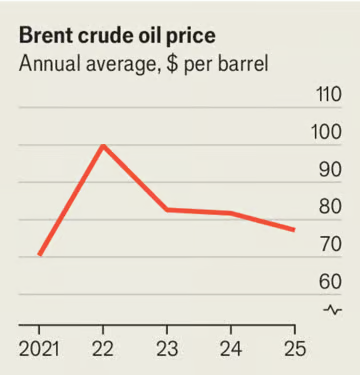

Although the energy transformation has come a long way, the share of fossil fuels in production is still very high. Energy consumption is expected to increase by 2% in 2025. More than 80% of this consumption will come from fossil fuels, which will increase carbon emissions by 1.7 times the 1990 levels. Although coal use will decrease in Europe and North America, India and Russia will continue to depend on coal. China's coal consumption is expected to reach its peak.

Oil consumption will also continue to increase. OPEC+ countries will continue to cut production to keep Brent oil prices high in 2025. However, non-OPEC oil production (Brazil, Guyana, USA) will increase rapidly.

Renewable energy sources will make great progress and will constitute 14% of total energy supply. Wind and solar energy will meet one-sixth of electricity production. Carbon-free nuclear reactors will be commissioned in China, India, South Korea and Turkey, bringing the total number of reactors worldwide to 447.

Green hydrogen is the new theme in energy. China will exceed its national green hydrogen production target of over 200,000 tons. Inner Mongolia and Gansu regions in particular plan to build production capacities that will double that target. However, new pipelines will be needed to transport this green hydrogen to densely populated areas in eastern China.

The growth of the insurance sector in the financial sector is expected to accelerate. Life insurance premiums are expected to reach $3.1 trillion, while non-life insurance premiums are expected to reach $4.8 trillion. The digitalization of the banking sector will continue. In 2025, there will be only 3 million ATMs in the world, compared to 2 billion credit cards. The boundaries between banks and financial technology (fintech) companies will become even more blurred. The Philippines will allow new digital banks. Spain's BBVA will open a digital bank in Germany. Brazil will make progress with its central bank digital currency, Drex. The EU will make a decision on switching to a digital euro. The US dollar will continue to dominate despite China's efforts to increase the international use of the yuan.

A quiet year is expected for food. Prices of most agricultural commodities are expected to fall in 2025 as food supplies increase. The food, feed and beverage index prepared by the Economist Intelligence Unit (EIU) is expected to fall 25% from its peak in 2022. Beverages and sugar are the most likely to lead the decline, while oilseeds and grains will be more resilient.

Despite Ukraine’s difficulties, wheat production will recover. India will ease restrictions on rice exports as global prices fall. Even cocoa prices, which have been rising rapidly for the past two years, will be a quarter of a percent, pleasing chocolate lovers. Meanwhile, American beverage manufacturers will continue to postpone plastic consumption targets.

Globally, consumers will spend $11.5 trillion on food. This figure is about a 6% increase from 2024. Despite the increase in vegan food sales, people will eat more fish and meat. However, as food sales accelerate, food company profits will fall from their highs in recent years.

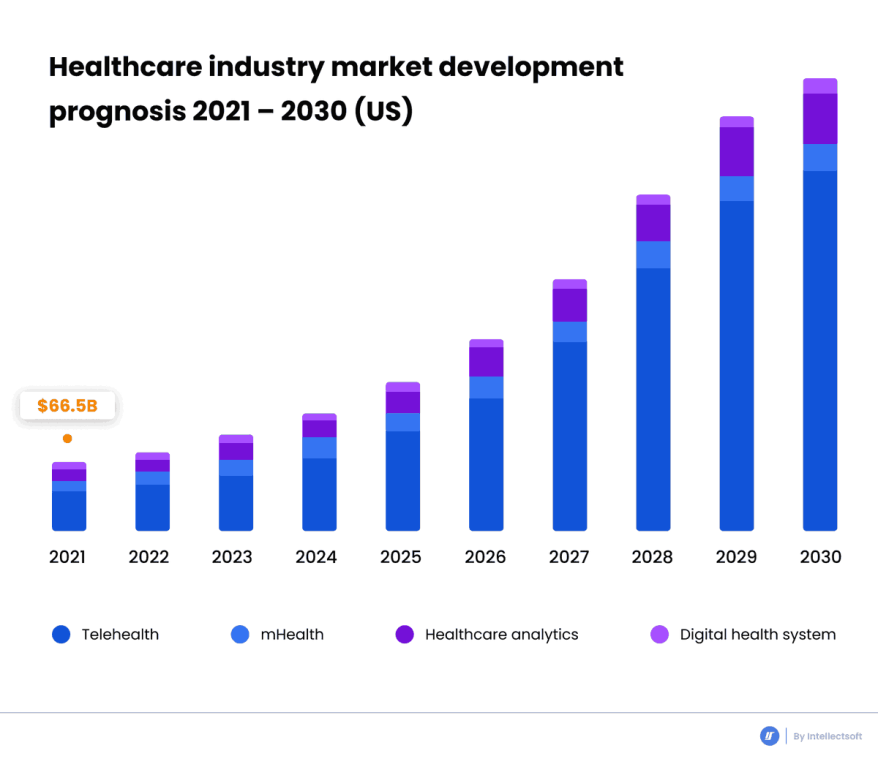

One of the strongest themes for the coming period is health. Healthcare systems will be under serious pressure by 2025 due to aging populations and strained staff. Almost 12% of the world’s population will be aged 65 and over. However, only 10% of global GDP will be spent on health, down from 11% during the COVID-19 pandemic. Global health spending will total $11 trillion, nearly half of which will be in the United States.

Concerns about infectious diseases will push governments to sign pandemic agreements. China and India will increase the number of obesity drugs by producing cheaper versions. Novo Nordisk will try to turn its weight-loss drugs into heart treatments. With the emergence of more expensive new treatments, drug sales will reach $1.7 trillion. Vaccination efforts will progress in 2025. Bavarian Nordic will produce 10 million mpox vaccines. Scientists will test a single-dose vaccine for bird flu and coronaviruses, and deliveries of mRNA vaccines for cancer could begin, it has been said.

The AI craze will continue. Total IT spending is expected to rise 8% to $3.6 trillion by 2025. But that’s still behind the 14% jump in 2021 triggered by the pandemic.

Investment in data centers and their revenues will increase, with more companies looking to leverage large language models like ChatGPT. According to consulting firm EY, about 30% of businesses in the U.S. will invest $10 million or more in AI by 2025, compared with 16% in 2024. The investment frenzy could be over the top in some cases.

On the hardware side, competition in chip manufacturing will intensify. Nvidia, the leader in AI chips, will try to hold its own against rivals like Arm and Google. Governments will race to lure chip manufacturing facilities home to protect their supply chains. Taiwan-based TSMC hopes to open its first U.S. facility, which has been long delayed. US-based Micron will launch its first chips produced in India.

A good year is expected for commodities. Especially for base metals. The EIU’s base metals index is expected to rise by 7.5%, exceeding its peak in 2022. Demand for electrical cables and batteries will push copper prices higher. Infrastructure investments will support zinc while also supporting steel, iron ore and aluminum prices. Tin will gain value as electronics consumption increases. Gold, which is seen as a safe haven, could have another strong year in times of uncertainty. The outlook for industrial metals may not be encouraging. With the emergence of new battery types in the automotive sector, nickel, cobalt and lithium prices are expected to rise more slowly.

Falling real estate interest rates will support markets, but global city centres are likely to remain quieter than before the pandemic.

Office rentals will rise as more employers demand their employees to be in the office for several days a week. Stores in prime locations will be resilient, but warehouse rentals will remain flat as the e-commerce boom cools. Tourist cities will remain vibrant, but hotel construction will be slow, except in the Gulf states and India.

Falling mortgage rates will make home loans cheaper. But supply shortages will still keep house prices and rents out of reach for many. Governments will encourage more construction, especially in Europe. The UK government is renovating some green areas to provide 1.5 million new homes.

Construction activity is picking up in the Netherlands, while Spain’s weakening housing market is also expected to improve. With more housing, the average number of people per household will fall to 2.4 in Europe and 3.3 globally. Europe is more wary of housing bubbles.

In China, housing prices are set to fall by 4% despite government efforts to stabilize the troubled sector. Globally, real estate loans are expected to reach $2.1 trillion. Three-quarters of these loans will be in the US.

It will be a tough year for the logistics sector. Tensions in the Middle East will continue to disrupt maritime traffic through the Suez Canal, the shortest link between Asia and Europe. Shipping companies will continue to reroute their ships around Africa’s Cape of Good Hope, lengthening journeys.

Regulatory hurdles are also on the way for carriers. From 2025, they will have to pay for pollution under the EU’s emissions trading system, which will cover 40% of their emissions in 2025 and increase to 100% by 2027. The EU’s heavy regulation will also tighten rules that allow tariff-free trade for low-value goods. This could reduce the impact of e-commerce, which has been a major advantage for air cargo, on cross-border trade.

Let me finish with tourism. International tourism trips will reach a new record of 1.6 billion in 2025. China’s outbound tourist numbers will account for a tenth of the total, finally surpassing pre-pandemic levels. Thailand will benefit from easing visa requirements. Similar action is expected from Indonesia.

China will ease rules for visitors entering the country. Asia’s share of tourism spending will reach 37%, putting it on par with Europe. Europe will attract more than half of international tourists. More than 60 countries, including the EU, the UK and the US, will charge tourists a $7 “visa exemption” fee.

Some Middle Eastern and African countries, such as Saudi Arabia and Zambia, will welcome more tourists thanks to hotel investments. The UK will mandate greener aviation fuels. But the global tourism sector will continue to emit 5-8% of greenhouse gases. China’s Comac will introduce its C919 aircraft, taking market share from Airbus and struggling Boeing. The most striking tourism development of 2025 will be Indian tourists. In 2025, the number of Indian tourists traveling abroad will increase by 17%, reaching 29 million.