Key takeaways

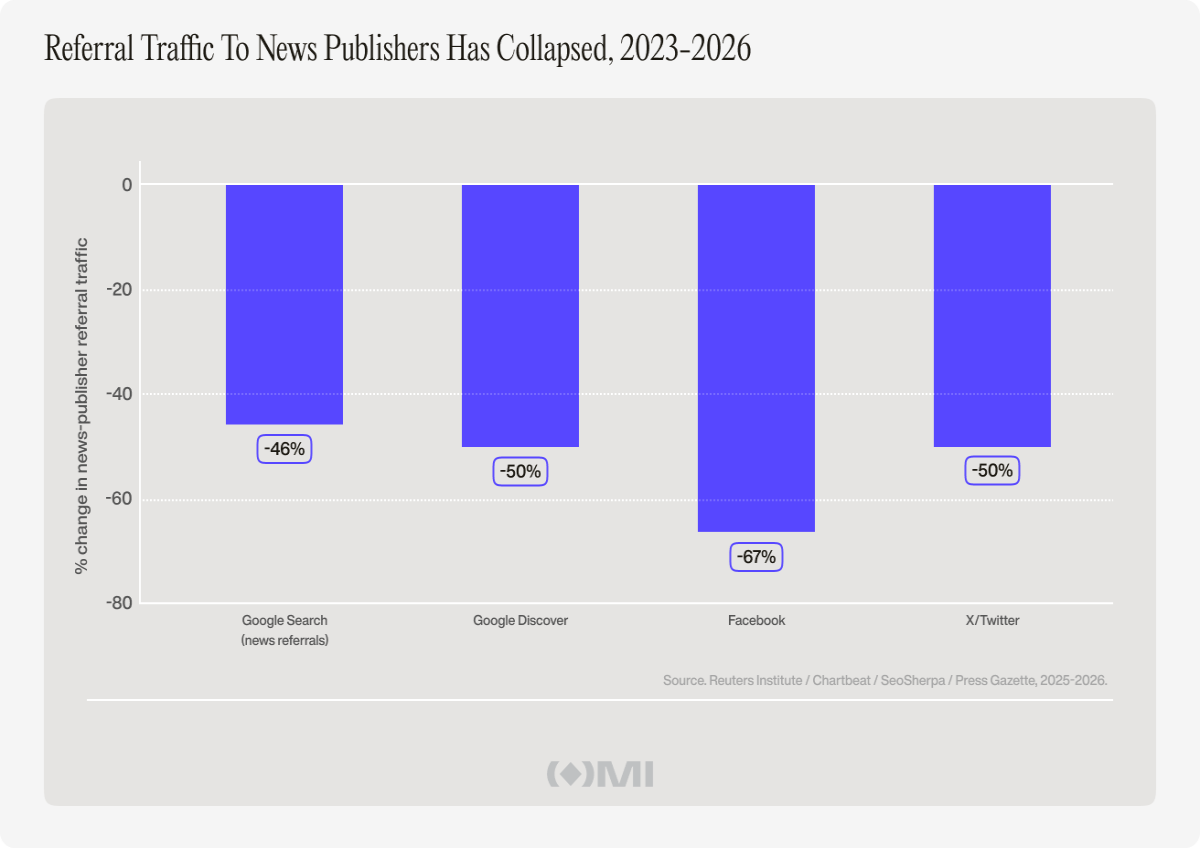

- News publishers face a referral-traffic collapse, with Google Search to news down 46%, Facebook down 67%, and X down 50% since 2023, alongside subscription-growth plateaus across all but the top 5 outlets.

- Prediction markets are the first new revenue category large enough to matter to a media company since digital subscriptions, with industry trading volume on track for $200 to $240 billion in 2026 and $1 trillion by 2030.

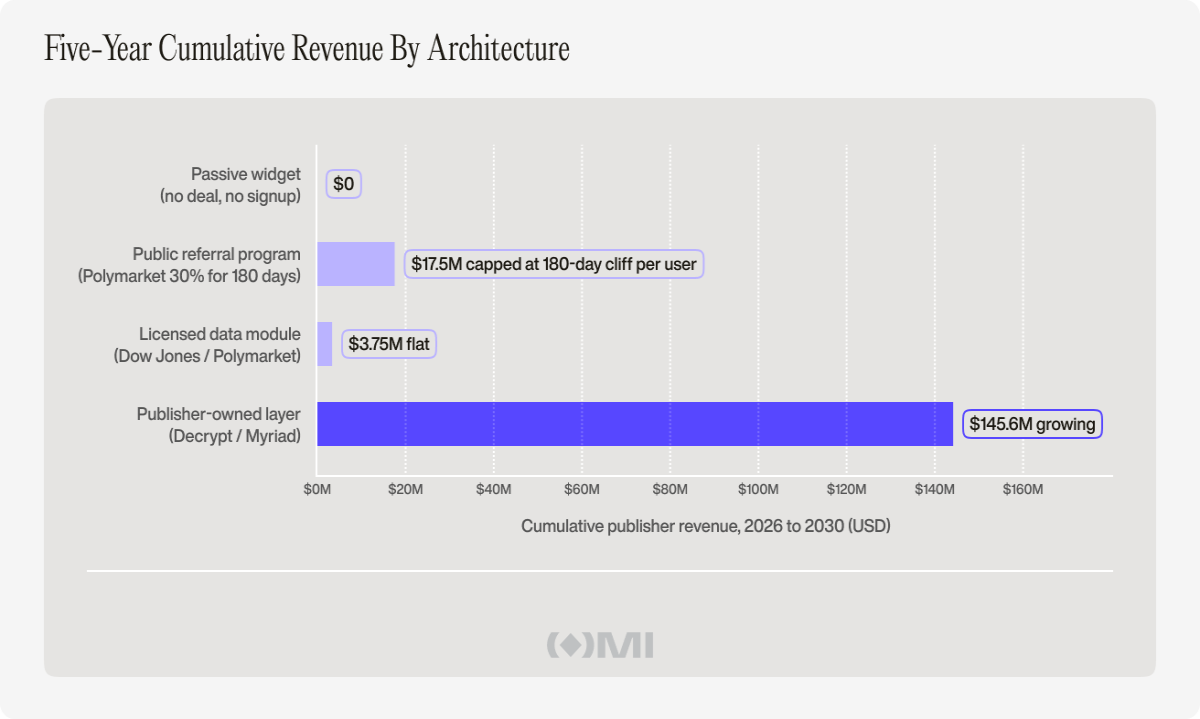

- Publishers who own the market layer earn approximately 8x more cumulative revenue from the same audience as publishers using Polymarket's public referral program, because the program's 180-day cliff caps capture at roughly 12% effective versus 100% permanent.

The revenue crisis

Between Q1 and Q4 of 2025 alone, Google web search referrals to news publishers fell from 51% to 27% of total inbound traffic, a 46% percent decline in a single year, driven by AI Overviews and zero-click results consuming news content directly inside Google's surface.

Reach plc reported that Google Discover traffic dropped 50% in H2 2025. Facebook referrals to publishers have declined by more than half since January 2023, with Chartbeat data pointing to declines exceeding 60% at major outlets, and X has lost approximately half of its news-referral volume across the same window.

Reuters Institute publishers expect a further 43% drop by 2029.

On top of that, subscription growth has flattened, with publishers citing stagnation as their top challenge, rising 383% year over year.

Pew Research puts US newspaper print ad revenue at $47.4 billion in 2005 and under $6 billion in 2023.

Local TV advertising peaked above $20 billion in 2020 and now sits below $17 billion.

Programmatic CPMs run $3 to $20, compressed for five years by duopoly share gain.

The curve is accelerating downward.

What changes when the trade stays on the publisher's surface

People still form opinions about events and still want to express them. The expression now happens on TikTok, X, and YouTube rather than on publisher websites. A prediction market embedded inside an article changes that geometry. It transforms a reader's opinion into a financial action that must happen on the publisher's surface, because the action only makes sense in the context the article provides.

Every news event is now a tradable instrument, and the publishers that occupy the airspace between the event and the trade earn a share of the resulting volume. A reader of a Bitcoin price story is already forming a probability estimate. Until just recently, that estimate ended at the close of the article. From 2025 forward, it is expressed as a real-money trade, settled on-chain or through a CFTC-regulated exchange, with the publisher as the introducing surface.

The question is whether publishers own that surface or merely host it. Newspapers linked out to Craigslist and Monster in the late 1990s on the assumption that the link itself was a service to the reader. Within a decade, the link had absorbed $20 billion of annual classified revenue. The choice now facing every news publisher is the same one.

Combined Polymarket and Kalshi volume reached approximately $23.82 billion in April 2026, against $55.34 billion for full-year 2025.

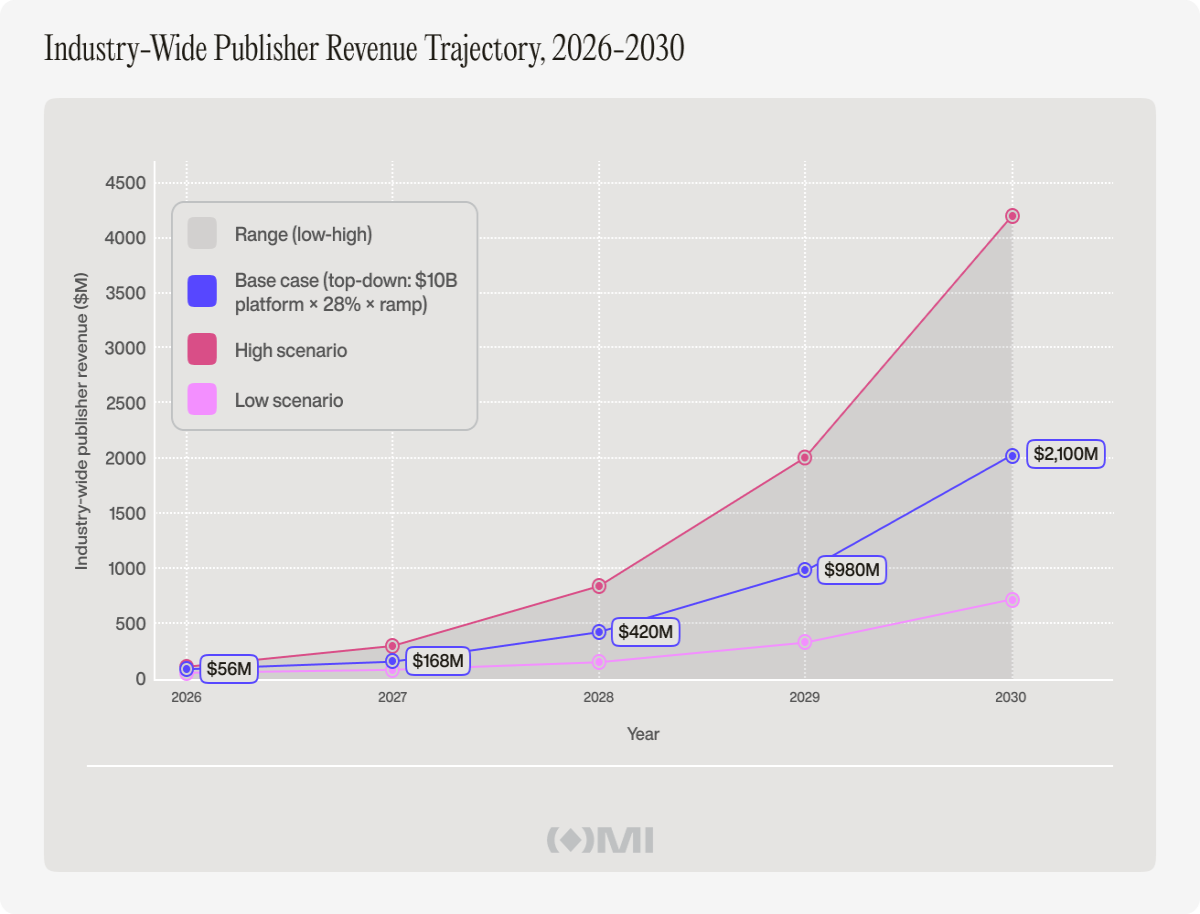

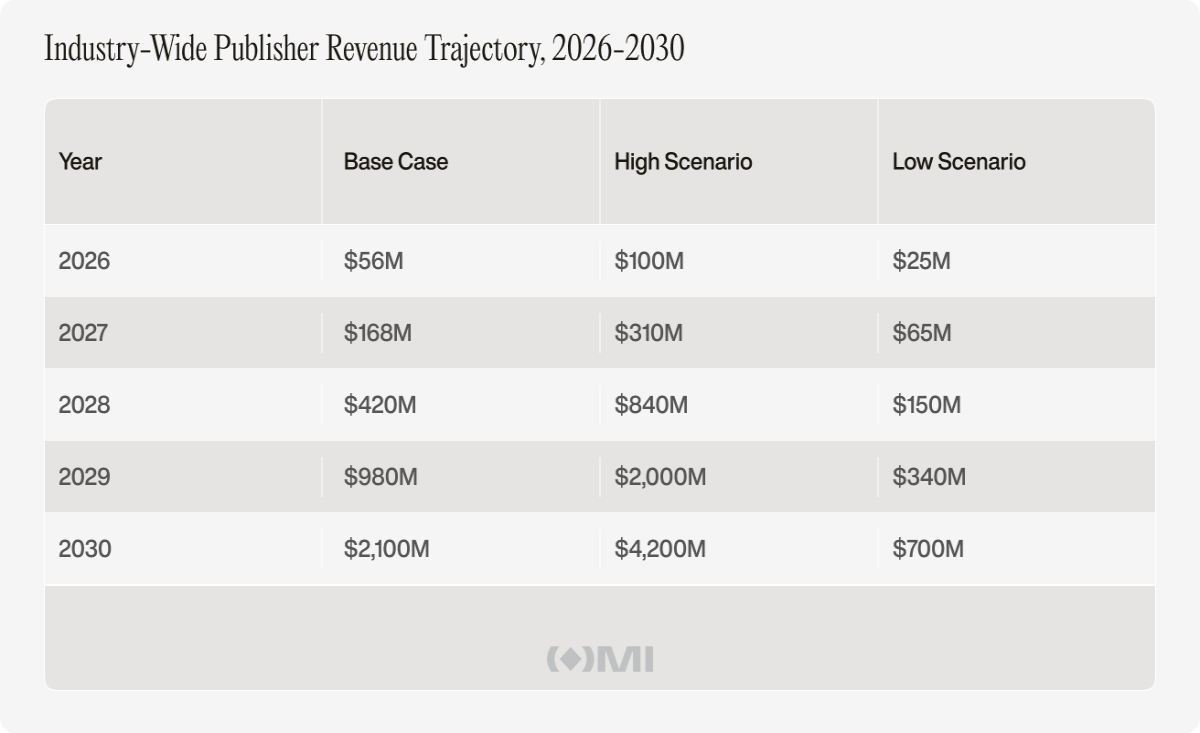

The industry is on pace for $200 to $240 billion annualized in 2026, with April’s $30 billion print representing the upper bound. Bernstein projects $1 trillion in annual volume by 2030, and Citizens Bank foresees $10 billion in annual platform revenue.

At a 28% publisher revenue share modeled on Coinbase and Binance affiliate programs, the total available pool reaches approximately $2.8 billion in 2030, of which roughly 75% is captured at realistic integration rates, producing the $2.1 billion base case below.

Four architectures of capture

There are four architectures by which a publisher can connect its content to a prediction market, and the choice of architecture is the single most important commercial decision a media company will make in the coming years. The architecture is what determines whether the publisher remains the leaflet pointing toward someone else's marketplace or becomes the one.

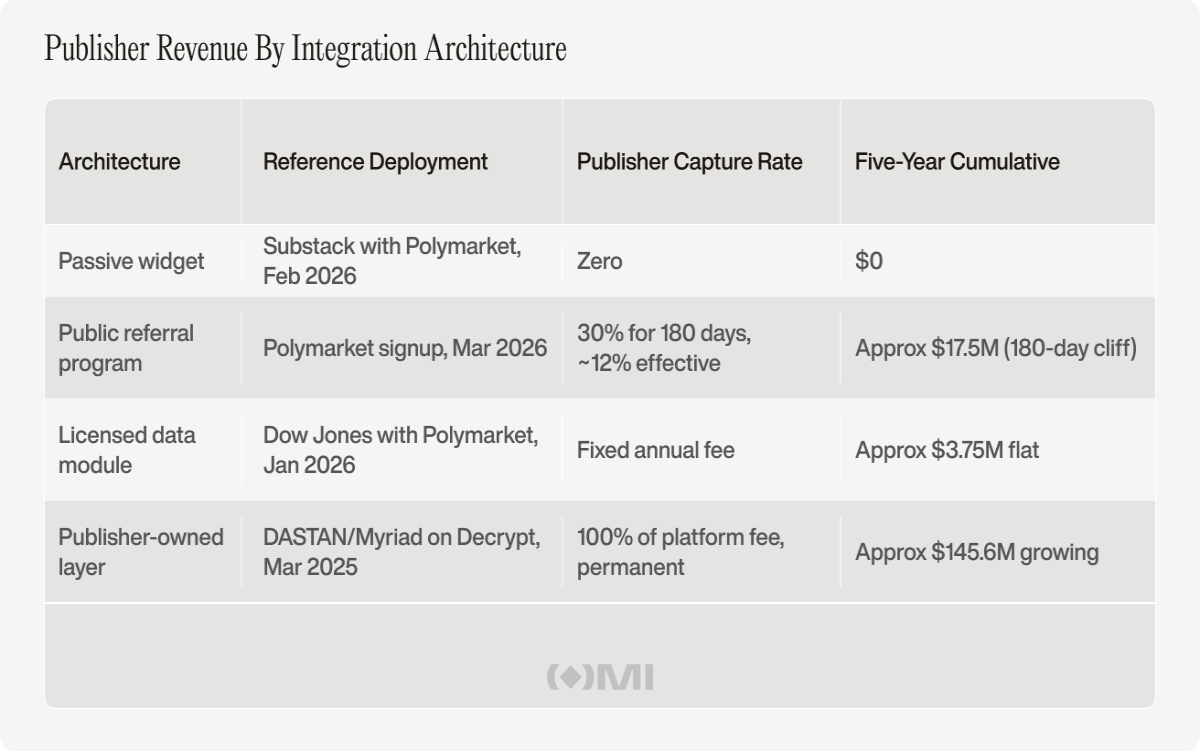

The first architecture is the passive widget, used by Substack since the Polymarket integration in February 2026: authors paste a URL, a live odds card renders, the click-through opens Polymarket in a new tab, and the publisher receives nothing.

The second is the public referral program. Polymarket launched a tiered structure in March 2026 that pays 30% of trading fees from directly referred users for the first 180 days, plus 10% on indirect referrals, with a $10,000 lifetime-volume threshold per trader.

The third is the licensed data module, used by Dow Jones across WSJ, Barron's, MarketWatch, and IBD, paying a fixed annual fee.

The fourth is the publisher-owned layer, exemplified by DASTAN's Myriad on Decrypt and Rug Radio, earning the full platform fee on volume routed through the publisher's surface.

The 180-day cliff reduces the public referral program's capture rate from 30% to approximately 12% on a steady-state basis. Each trader produces fees only inside a 6-month window before the rate drops to zero on subsequent activity.

For an outlet with an 18-month average user trading lifetime, which is a fair anchor against the crypto-exchange user-retention benchmark of 14 to 22 months, the effective annual rate is 30% × (6/18), close to 10%. At a CoinDesk-scale audience, this produces approximately $17.5 million in five-year cumulative revenue, well above the licensed fixed fee but well below (8x) the $145.6 million achievable on owned architecture.

The unit economics

What numbers did we use:

- Engagement rate, crypto outlets: 6%-8% of monthly visitors

- Engagement rate, finance outlets: 3%-5% of monthly visitors

- Conversion rate, engaged user to placed trader: 22%

- Trades per active trader per month: 8

- Average trade size: $100

- Platform take rate: 1.4%

- Publisher referral share: 30%

- Publisher-owned capture: 100% of the platform fee

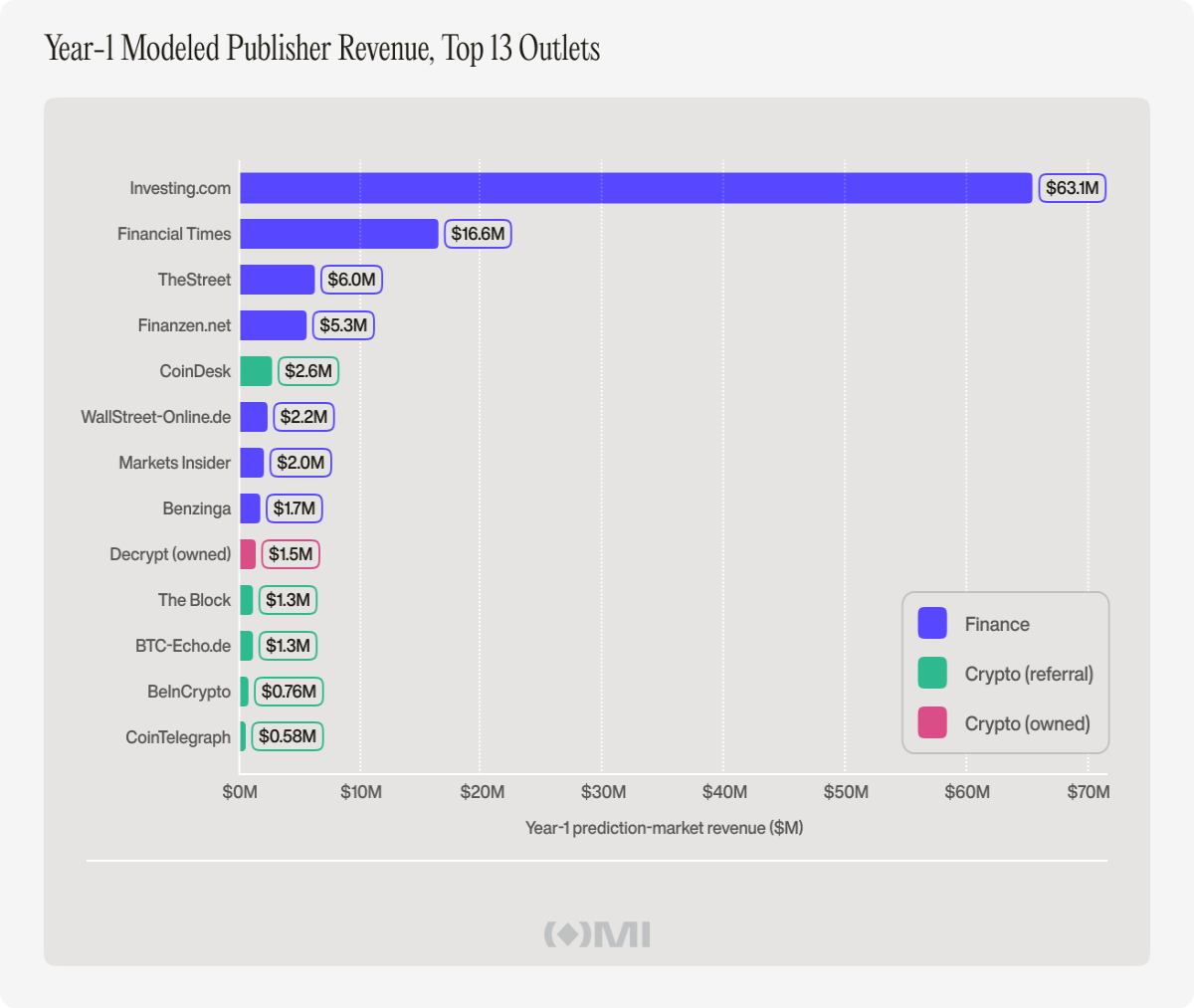

Investing.com tops the cohort at $63.1 million year-one. The Financial Times produces $16.6 million, TheStreet $6.0 million, and CoinDesk $2.6 million on referrals.

Decrypt generates $1.5 million from roughly 1 million visitors using its own architecture. If CoinDesk replicated Decrypt's architecture, year-one revenue would reach approximately $8.5 million, a 3.3x increase from the move to 100% capture.

The 5-year outlook

The industry projection uses two methods that read together.

The top-down method anchors against the Citizens Bank $10 billion 2030 platform revenue forecast, applies a 28% publisher share modeled on crypto-exchange affiliate programs, and adjusts for an integration ramp from 15% of major outlets in 2026 to 75% by 2030. This produces $56 million in 2026 and $2.1 billion in 2030 base case.

The bottom-up method applies the unit economics above to a cohort of 60 crypto and 30 mainstream financial outlets at median scale with the same integration ramp, and lands within $5 million of the top-down 2026 estimate.

The revenue will not divide evenly

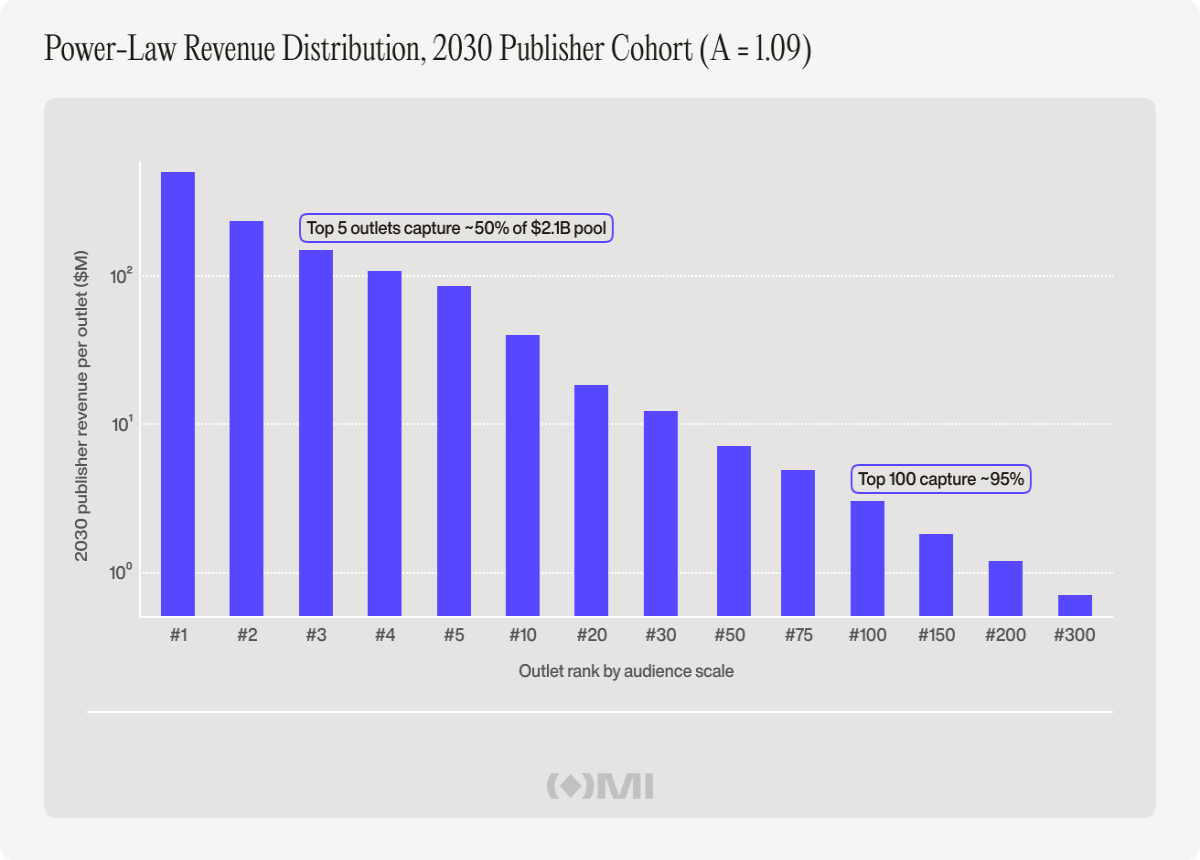

Attention in the media is not normally distributed. The top 1% of online publications capture more than half of all referenced traffic in the United States, and the same dynamic governs subscription, ad pricing, and editorial recruitment. The prediction-market revenue line will follow the same curve.

The $2.1 billion publisher pool implied by the 2030 base case will not divide evenly across the cohort. The top 5 outlets, by virtue of audience power-law concentration, absorb roughly half of it. The next 15 absorb another quarter. The remaining four-fifths of the publisher count divides the final 25%.

The power-law exponent applied here is approximately 1.09, anchored to observed traffic-concentration data across the Outset Media Index Q1 2026 cohort and tuned to produce the top-5 share of approximately 50% that the audience data supports.

In dollar terms, the Bloomberg-class outlet at rank one earns approximately $486 million in 2030. The Wall Street Journal and Financial Times ranked two and three, respectively, earning $146 to $228 million. The CoinDesk-class outlet at rank 20 earns $18 million.

Architecture matters disproportionately outside the top 20. A rank-50 outlet on third-party referral earns approximately $7 million. The same outlet on owned architecture earns approximately $34 million on the same audience. For mid-tier publishers, architecture is the only available lever.

The passive widget trap

The most common error a publisher will probably make in this transition is the passive widget without even the public referral program sign-up. The architecture is appealing for the wrong reasons: no engineering work, no editorial coordination, no compliance overhead, and no commercial negotiation. The Substack-style paste-in is the textbook case.

A reader sees a live odds display, clicks it, and is taken to Polymarket in a new tab. Without the publisher having signed up for the public referral program at the time of the embed, every dollar of trading revenue that follows accrues to the platform with zero share routed back. The publisher has trained its audience to leave the property to express opinions on the publisher's content, and earned nothing for the introduction.

So adding a Polymarket widget without at minimum the public referral program signup is a bad strategy. It is unpaid distribution work performed on behalf of a competitor. Any embed deployment should require a measurable revenue share, dashboard-level access to the trading data, and acknowledgment that the public referral program with its 180-day cliff is a floor.

Publishers without leverage to negotiate beyond the public program should still operate it, but should plan the migration to owned or co-branded architecture inside the user-acquisition window the public program creates.

Three tiers of market integration

Markets attach to articles in three tiers. The tier determines editorial overhead, integration complexity, and revenue potential:

- Tier-1 markets are evergreen and price-driven: Bitcoin daily and weekly close, Ethereum price by week, S&P 500 direction. They auto-populate from article topic tags and require no editorial decision.

- Tier-2 markets are event-driven and article-triggered. A new AI model release auto-surfaces a benchmark market, a Fed preview surfaces the rate-cut market, and an earnings preview surfaces the EPS-beat market. These require a CMS integration that maps article entities to open markets via API.

- Tier-3 markets are publisher-created and proprietary, available only to outlets running owned architecture, generating proprietary liquidity, and building retention around the outlet's forecasting track record. Tier-3 is the only tier that earns full economics and compounds reader loyalty around the publisher's analytical brand.

The conflict publishers must solve before regulators do

A publisher that owns a prediction market on a story it covers has a financial interest in how that story is framed. If The Block creates a market on a spot ETH ETF approval and earns the platform fee on volume routed through its surface, it earns more from contentious outcomes than from clean ones, which creates an incentive to frame coverage in ways that sustain rather than resolve uncertainty.

So, we propose that 4 mitigations should become industry standard:

- First, a Chinese wall between editorial and trading, modelled on research-trading separation inside investment banks.

- Second, disclosed market positions for journalists covering topics with active associated markets surfaced at the article level.

- Third, market-creation authority held outside the newsroom, with editorial veto on topics aligned with breaking news.

- Fourth, third-party oracle settlement on outcome determination.

Time is running out

Media businesses spent 20 years searching for a revenue stream large enough to replace what was lost when the internet absorbed classifieds and the duopoly compressed display advertising. Prediction markets are the first category in two decades large enough to matter, and that places the publisher at the natural distribution point in the value chain.

As of publication in May 2026, our near-term deadline is 2028. Publishers that have selected an architecture, signed a deal, or deployed a white-label backend before 2028 operate inside a price-discovery process that still favors them. Publishers that have not negotiated against the standardized terms that follow.

The lesson of the classifieds precedent is that the publishers first to adopt do not always win, but the publishers last to adopt always lose.

P.S. this research originally appeared on Outset Media Index (OMI) Substack page.

Outset Media Index is powered by Outset PR