Don't let the word "Loss" scare you away from 56% APR! Most beginners stick to safe staking (5% APY) because they fear Impermanent Loss, but they are leaving money on the table. Today, I share my real experience yield farming with $3,000 on Uniswap, and how despite the “virtual loss” I faced temporarily, I stayed calm. Find out how I earned over $1,100 in passive income despite market volatility, and learn to set up your own yield farming strategy safely.

We’ve all been there. That precise moment when a substantial windfall hits your balance and you realise this surplus doesn't need to be liquidated immediately. That scenario played out for me earlier this year when I secured a commission from a Web3 project. I was out in the garden, tending to my tomatoes and basil, when a notification suddenly pierced through the music playing on my phone…

"Deposit Successful: 3,000 USDT"

I stared at the screen, smiling, letting the dopamine run its course. That feeling of immediate reward is undeniably addictive. However, once that initial rush dissipated, my rational brain took the helm.

This was capital I could have easily let lie dormant in a traditional bank, or simply left stagnating in my Binance spot wallet…

But any astute investor knows the fate of money that remains idle: inflation relentlessly erodes its purchasing power. Or worse, I might succumb to the impulsive urge to purchase gadgets I definitely don't need.

Determined not to let this opportunity wither, I finished watering my plants and hopped onto my laptop with a singular goal: to figure out how to put this capital to work.

Staking vs. Yield Farming: Why 5% APY Wasn't Enough

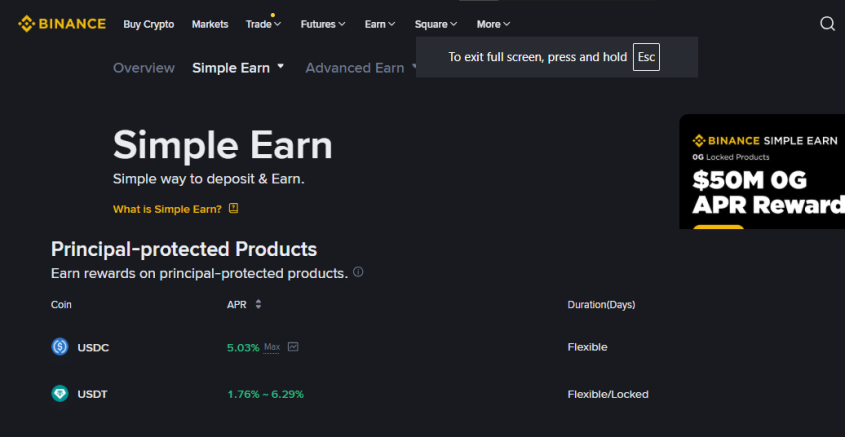

My initial port of call was the classic "Earn" or flexible savings section on Binance. I scanned the rates for USDT, which were hovering around 4%, perhaps 6% if I agreed to a lock-up period.

"The yields are underwhelming," I thought, frowning. "With a $3,000 principal, a 5% return generates a paltry $150 a year. That barely covers a decent dinner once every six months."

The safe but slow route: Binance Simple Earn offered me around 5-6% APR on stablecoins. Safe?

Yes. But compared to the potential of yield farming, it felt like watching paint dry.

I wanted more. I knew that in the crypto ecosystem, risk pays well. I’d already read a bit about yield farming. I knew that unlike simple staking (where you just lend your money to an exchange or a network), in yield farming, you become the market. You put up your money to provide liquidity so others can trade, and in exchange, you get a cut of the trading fees.

I conducted my due diligence and decided to eschew sketchy, high-risk platforms. I wanted to mitigate smart contract risk as much as possible, so I selected the undisputed heavyweight of decentralized exchanges: Uniswap.

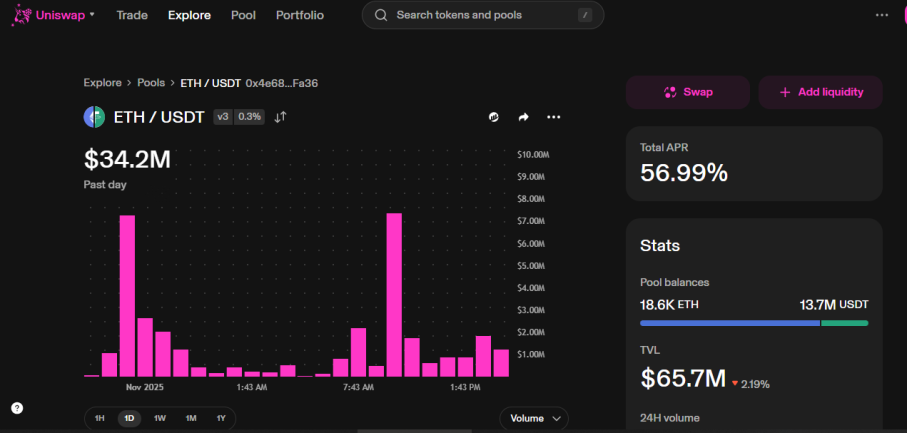

When I opened the interface, the metrics were reassuring. The ETH/USDT pool boasted deep liquidity, over $65 million, which instilled confidence. But what truly captivated me was the bright green figure on the right: a staggering APR of 56.99%.

The number that hooked me: A massive 56.99% APR on the ETH/USDT yield farming pool,

far outperforming the 5% offered by traditional bank staking

So I did the math in my head instantly: that was way more than 10 times what the Binance was offering! It was the perfect opportunity for my $3,000.

My plan was simple: take my 3,000 USDT, convert them into a liquidity position (half in ETH, half in USDT), and just sit back and watch my earnings grow thanks to yield farming.

I felt like a financial genius. I was just about to confirm the transaction when I spotted a term in the fine print…that was a warning that showed up in almost every serious tutorial:

"Watch out for impermanent loss."

(By the way, speaking of using crypto for daily stuff: if you are curious about how we actually use these assets down here in the 'testing ground', you absolutely cannot miss my latest deep dive: Beyond Speculation: The 2026 Definitive Guide to Stablecoins in Latin America. But I digress...)

How to Set Up a Yield Farming Position on Uniswap (Step-by-Step)

Here came the operational bit of the whole affair. I had my 3,000 USDT sitting in Binance. I’ve always been extremely picky about which stablecoins I hold, especially after researching the disasters I covered in The Stablecoin Graveyard: Where Your ‘Dollar’ Goes to Rot...but for this strategy, USDT was the necessary fuel.

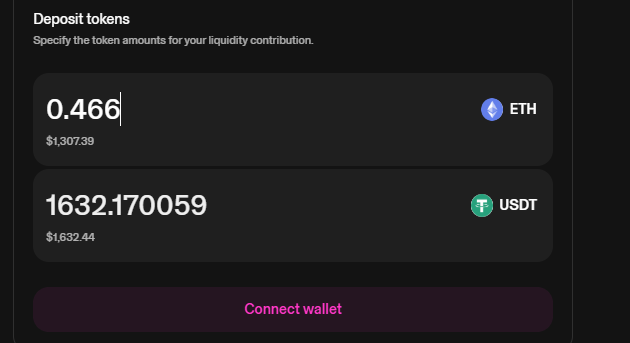

I couldn't just turn up at Uniswap with USDT alone. So, I did the maths in reverse carefully. Based on the range I picked, Uniswap asked for a specific mix: I needed approximately 0.466 ETH and about 1,632 USDT.

The ingredients: To set up the yield farming position within my specific price range, Uniswap required an unbalanced deposit of roughly 0.466 ETH and 1,632 USDT, not a simple 50/50 split

Key question: Can I send money from my Binance account to Uniswap?

Yes, it was possible. First, on my exchange, I bought Ethereum and sent it along with the USDT all of it to my Binance wallet.

Then I connected my Binance wallet to Uniswap. I made sure to follow basic crypto wallet security tips before connecting. Thankfully, it was dead simple.

In total, I was depositing about $2,940 in real value. I left the rest of the cash to buy fertilizer for my tomato plants.

(Ideally, I would have paid for that fertilizer with crypto, but the lady at the plant nursery is old-school. If she had a POS terminal, I would have definitely whipped out one of the plastic beauties I reviewed in my post about Crypto cards in latam. But alas, cash is still king in the garden.)

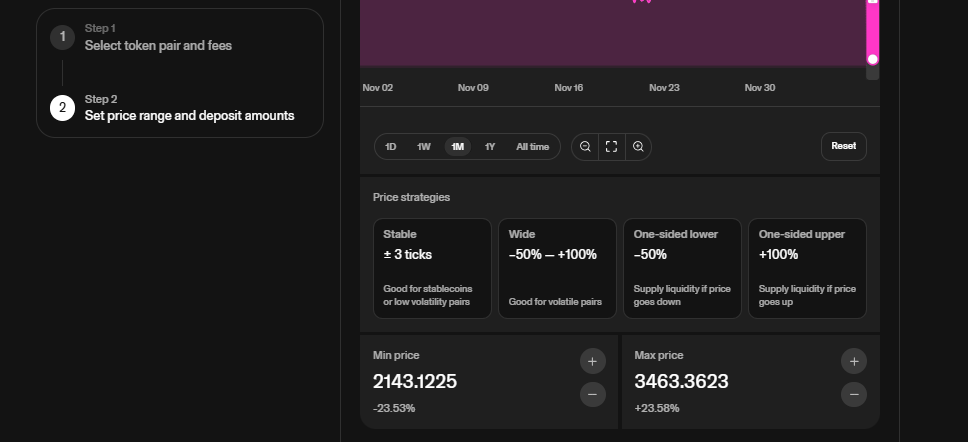

Defining my territory: Instead of providing liquidity for any price, I set a specific range ($2,143 - $3,463).

This "concentrated liquidity" boosts yield farming efficiency but increases the risk of impermanent loss if the price escapes the zone.

So, what exactly is my "position" now? My position was not exactly 50% ETH and 50% UDST. As you can see in the last image, it consists of 0.466 ETH ($1,307) and 1,632 USDT.

Impermanent Loss Explained: A Real Calculation Example

Pay special attention to this part because it is crucial if you are really interested in Yield Farming.

We call “Impermanent loss” a temporary reduction in the value of your position compared to simply holding the tokens in a wallet. It happens when the price of your deposited tokens changes compared to when you entered the pool.

Because the protocol is automated, it is programmed to constantly rebalance your assets. Essentially, the system sells the token that is going up in price and buys the one that is going down to maintain the correct ratio.

The "loss" is the difference between what you have now in the pool versus what you would have had if you just did nothing.

If you did not understand that perfectly, do not worry. I did not understand it at first either. But that is exactly why I am here. Let us look at my personal case to see how impermanent loss works in the real world when things get out of control and the market surprises us.

After reading this, you will have a crystal clear understanding of how this mechanism can affect you when investing in Yield Farming.

Spicy Situation 1: Impermanent Loss when The price of ETH rockets (Up to $4,900)

Between August and September 2025, the price of Ethereum absolutely flew. Everyone saw it. It eventually smashed right through my upper limit of $3,463.

As it climbed, my position automatically sold all my 0.466 ETH in exchange for USDT, just as it was programmed to do.

- The Result: I was left standing there with 100% USDT and 0 ETH inside the pool.

- The "Loss": This was the painful part. If I had simply kept both assets in my Binance wallet, they would have been worth nearly $3,915 ($2,283 in ETH and 1,632 USDT).

However, because the pool sold my ETH prematurely (capping out at $3,463), my position was stuck holding only about $3,084 in USDT.

The difference? A painful $831. That is the Impermanent Loss. If I had panicked and clicked "Remove Liquidity" right at that moment, I would have realized that loss permanently.

The breakout: The red circle marks the moment ETH's price smashed through my upper limit. While the market celebrated the rally, my yield farming robot was busy selling my ETH too early, crystallising the "loss" against holding.

Fictional Scenario: Impermanent Loss When The price of ETH crashes (Down to $2,000)

In order to illustrate the contrary situation let's suppose that the price of ETH drops. If the market started bleeding and broke through my lower limit of $2,143, my position would have done the reverse: using my 1,632 USDT to try and stop the fall by buying up "cheap" ETH.

- Result: I would be left with 100% ETH and 0 USDT. Specifically, I would end up holding about 1.13 ETH (worth $2,260).

- The "Loss": If I had simply held both assets in my wallet on Binance, I would still have my safe 1,632 USDT cushioning the fall. My total value would be $2,564. But in the pool, I lost that safety net. My robot spent my dollars buying a falling asset, leaving me with a portfolio worth only $2,260.

In this case, the impermanent loss would be $304. But of course, I wouldn't do anything, because I don't want this "loss" to become materialized. I would just focus on my other activities and wait for the market to stabilize.

The simple conclusion: Impermanent Loss is basically the opportunity cost of having a robot that constantly rebalances your money when you invest in yield farming. This is exactly what DeFi 2.0 innovations are all about: giving you granular control over your assets.

So why did I accept the risk?

Because as long as the price of ETH dances between $2,143 and $3,463, I’m the king. Every time someone buys or sells within that range, ka-ching!. A cut of that 0.3% fee goes straight to me.

Impermanent Loss represents the temporary difference in value between holding tokens in a liquidity pool versus holding them in a wallet. It occurs when the price of deposited tokens changes significantly compared to the time of deposit.

Conclusion for Impermanent Loss: Patience Pays Better Than Panic

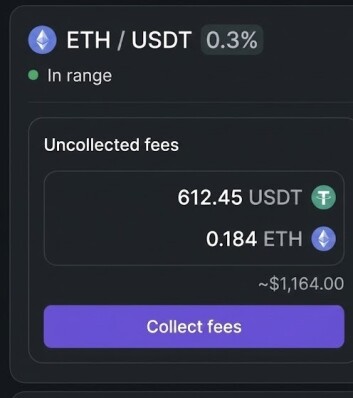

Today, nine months post-deployment, I maintain my position active. The result? I have accrued approximately $1,164 in fees so far.

Did I transform into the next Warren Buffett? Hardly. But did I grapple with anxiety when I saw my position "losing" against a simple holding strategy? Undoubtedly. There were moments of acute doubt and bitter regret—especially when ETH rallied miles outside my range. I was haunted by the opportunity cost, thinking I could have made thousands if I’d just left my ETH dormant in Binance.

Patience pays off: Despite the scary fluctuations caused by impermanent loss, the accumulated trading fees generated over $1,164 in passive income after 9 months.

However, the most valuable lesson I gleaned wasn't about finance; it was about behavioral psychology.

Impermanent Loss only crystallizes into a real loss if you capitulate to the volatility on your screen. If you panic and "jump off the rollercoaster" halfway through, withdrawing your liquidity precisely when you are in the red, you turn a theoretical paper loss into a permanent financial injury.

By maintaining my composure and letting time and mathematics do their heavy lifting, those incremental 0.3% fees I collected day after day eventually compounded, effectively offsetting the temporary divergence.

So, if fortune blesses you with surplus capital and you seek lucrative passive gains, my advice is this: give yield farming a go. Calibrate your range, respect the risks, and above all, mitigate your anxiety.

This game is about understanding that a bountiful harvest—much like my tomatoes—requires a long investment horizon, care, and unwavering patience.

Yield Farming for Beginners: Your Questions Answered

1. Is Yield Farming actually better than a traditional savings account?

Absolutely, if you can handle some volatility. While traditional banks might offer you a meagre 4% or 5% annually , Yield Farming on decentralized exchanges like Uniswap can offer significantly higher returns—in my case, I saw an APR of nearly 57%. However, unlike a bank, these returns come from real trading fees, not interest rates, so they fluctuate with market activity.

2. What happens if the market crashes? Do I lose my $3,000 due to impermanent loss?

Not necessarily. This is where Impermanent Loss comes in. If the price of Ethereum drops, the automated system rebalances your portfolio by buying more ETH with your USDT. Your total dollar value might decrease temporarily on screen, but you haven't actually "lost" the money unless you panic and withdraw your funds at that moment. If you wait for the market to stabilise, the accumulated trading fees can often offset these temporary dips.

3. Is my money "locked up" like in a fixed-term deposit?

No. One of the biggest advantages of DeFi (Decentralized Finance) over traditional banking is liquidity. You are the owner of your funds. Even though I planned to let my position grow, I could have clicked "Remove Liquidity" at any second and moved my funds back to my wallet. There are no penalties for early withdrawal, giving you total control over your assets.

4. Can I start Yield Farming with stablecoins to avoid risk?

Yes, and it is a popular strategy. In my case study, I used a mix of ETH and USDT because I wanted exposure to Ethereum's growth. However, if you are strictly looking for passive income without the price volatility of crypto assets, you can provide liquidity to stablecoin pairs (like USDC/USDT). The APR might be lower than 56%, but the risk of Impermanent Loss is virtually zero since the prices of both assets stay pegged to the dollar.

5. How exactly do I get paid the interest if I do Yield Farming?

You don't get a monthly bank statement. Instead, you earn trading fees in real-time. Every time someone trades ETH for USDT (or vice versa) within your selected price range, you get a cut of the 0.3% transaction fee. These earnings accumulate in your position. In my experience, even when the market moved against me, those fees kept adding up, generating over $1,100 in passive income over time

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Cryptocurrencies are volatile assets; always conduct your own research (DYOR) before making decisions.

✍️ Written by El Salvador CopyBiker — Crypto Content Specialist.

Helping your audience actually understand your Web3 product (no PhD required).