Little did the global financial community anticipate a decade ago that Stablecoins in Latin America would become the world's testing ground for digital assets. As we enter 2026, the region’s financial landscape has undergone a transformation that is diametrically opposed to the speculative mania seen elsewhere. Here, the massive adoption of stablecoins stems not from a desire for quick riches, but from a pragmatic need for economic survival. While the rest of the world debated regulation, LatAm built a parallel infrastructure to do away with the inefficiencies of traditional banking.

For those of us living the reality of currency volatility and restrictive capital controls, fiat-backed stablecoins (primarily the US Dollar) have become the "de facto" standard for wealth preservation. This exhaustive report aims to shed light on an ecosystem that saw transaction volumes nearing $1.5 trillion between 2022 and 2025, a figure that stands as a testament to the region's accelerated crypto-literacy.

To provide a genuine "on-the-ground" perspective and get to the bottom of what is really happening, I’ve included testimonials from my professional network across Mexico, Colombia, Chile, and Argentina. These are seasoned freelancers and digital nomads navigating the 2026 economy in real-time.

Why read this?

-

For Freelancers & Nomads: It is a practical roadmap to financial mobility, provided that you know which protocols to trust. If you want to read this in Spanish, click here.

-

For CEOs, CMOs, & Founders: If you are looking to gain traction in this region, this guide offers a deep dive into user psychology. You will learn that success here hinges on understanding what scares local users and how to strike a chord with a market hungry for stability.

The Macroeconomic Engine: Why Latin America Leads in Real-World Utility for Stablecoins

To get to the bottom of the omnipresence of stablecoins in 2026, one must look beyond the technology and analyse the structural conditions that rendered them a logistical necessity. In North America or Europe, stablecoins are often viewed through the lens of institutional hedging; however, the use case in Latin America is diametrically opposed to this speculative approach. Here, they have evolved into the fundamental infrastructure layer for daily commerce, where financial survival hinges on access to hard currency.

Figure 1: The Macroeconomic Engine. This infographic visually contrasts the role of digital assets. While often a tool for institutional hedging in the Global North, stablecoins in LatAm, particularly Tether (USDT), have evolved into essential infrastructure for daily commerce and financial survival.

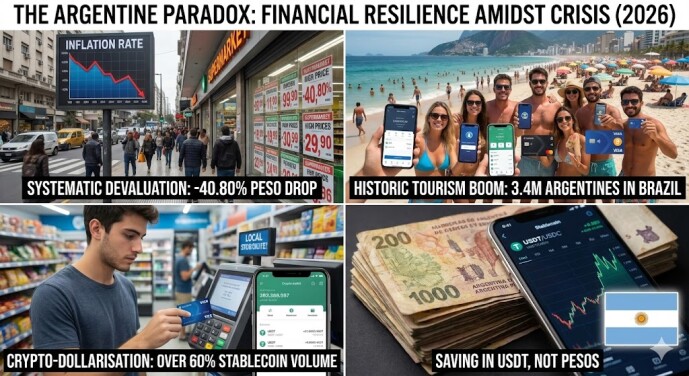

Inflation vs. Financial Resilience: The Argentine Paradox

The primary driver for retail adoption stems from the urgent need to preserve purchasing power. Notwithstanding the strength of other regional currencies in 2025, the Argentine Peso suffered a staggering -40.80% devaluation against the dollar. This systematic erosion wreaked havoc on local savings, effectively paving the way for "crypto-dollarisation": today, stablecoins like $USDT and $USDC account for over 60% of Argentina’s total crypto volume.

A fascinating metric for 2026 is the historic boom of Argentine tourists in Brazil. The fact that Argentina sent 3.4 million travellers to Brazil last year, representing a third of all foreign visitors, stands as a testament to the liquidity provided by digital assets.

-

My friend Hugo (a Travel YouTuber from Mendoza - Argentina) explains the shift: "We no longer save in Pesos; we accumulate USDT. We cross the border and pay with crypto-linked debit cards that settle in real-time. On my trip to Brazil, I used my crypto card without any problems to buy food, tickets, hotel, taxis, etc... it has the Visa logo, so I can use it anywhere in the world".

Figure 2: As annual inflation in Argentina has surpassed 200% in recent periods, the systematic destruction of the local currency's purchasing power has turned crypto-assets into an existential necessity. In this environment, stablecoins in Argentina, primarily USDT and USDC, now represent over 60% of the nation's total crypto volume.

The Remittance Revolution: Mexico’s Efficiency Play

Mexico provides a counter-narrative that runs contrary to the crisis-driven adoption seen elsewhere. The Mexican Peso ended 2025 with a robust +13.52% performance against the dollar, and its middle class grew by 8.0% between 2019 and 2024. Here, adoption is driven by operational efficiency rather than fear.

- Invisible Infrastructure: According to Reuters, Mexico processes over $63.3 billion in annual remittances. Stablecoins now represent 36% of all crypto purchases in the country, a figure that is conducive to a more fluid cross-border economy.

The Professional Use Case: My friend, Ariel, an Appointment Setter in Mexico City, highlights the friction of legacy banking: "I work for US-based startups and I cannot wait three or five business days for a SWIFT wire to receive my money in my banking account from Paypal... Since I use Binance my situation has completely changed. Stablecoins allow me to receive funds in minutes with negligible fees".

For the 32% of Mexicans excluded from the traditional banking system, stablecoins are their first real encounter with global financial inclusion.

Stablecoins in Colombia: Hedging Against Political Volatility

Notwithstanding the Colombian Peso’s (COP) emergence as one of the region’s strongest performers in 2025 with a +14.32% appreciation, domestic sentiment remains at odds with the charts, governed by a high "political risk premium." For a global Founder, understanding Colombia requires recognizing that macro currency strength often belies the micro-anxiety of its digital workforce. The COP is notoriously susceptible to political rhetoric, oscillating violently between $3,700 and $5,000 based on a single legislative announcement.

The Talent Anchor: For my friend, Fabian, a copywriter in Cali serving global travel agencies, stablecoins are a tool for "mental decoupling."

-

Operational Predictability: By earning in $USDT, Fabian avoids the "rollercoaster" of local exchange rates, ensuring his business overheads remain predictable, irrespective of domestic noise.

-

Banking Friction: Despite the currency's strength, users frequently face impediments from legacy gateways like Mercado Pago, citing vague "security reasons" that can freeze funds for days.

Strategic Growth: This friction has paved the way for institutional interest; Tether recently invested in Orionx to bridge the gap in stablecoin liquidity across Colombia, specifically targeting remittances and B2B treasury.

Infrastructure: Furthermore, with Visa launching USDT-compatible cards, the barrier between "digital dollars" and daily spending has been rendered obsolete for the Colombian freelance class. For the 2026 market entrant, Colombia demonstrates that stablecoin adoption is no longer just about hedging; it is about financial autonomy for a workforce that has outgrown its local banking infrastructure.

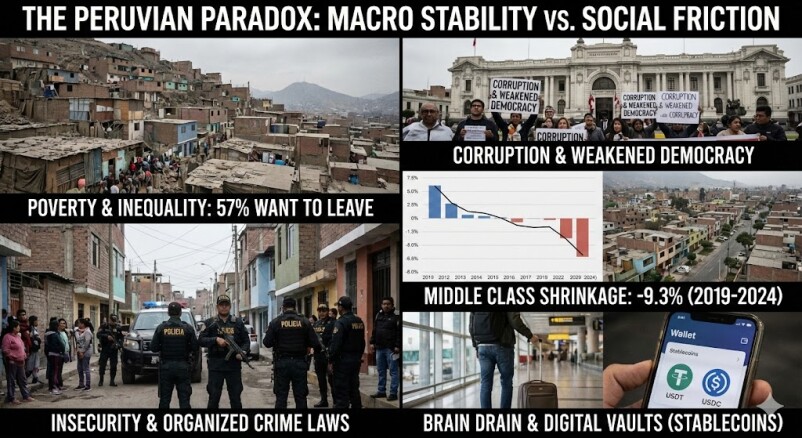

The Peruvian Paradox: Macro Stability vs. Social Friction

As a resident of Peru, this section is deeply personal. On paper, the country is a fiscal fortress, ending 2025 with $100 billion in International Reserves (RIN). However, these macro statistics often merely paper over a fractured social reality. In terms of poverty, corruption, serious weakening of democracy, and the passage of laws that favor organized crime, the country is seriously battered.

The disconnect is stark:

-

The Brain Drain: 57% of Peruvians express a desire to leave, a statistic that speaks volumes about the lack of opportunities and rising insecurity.

-

Economic Erosion: While Mexico’s middle class grew, Peru’s middle-class population dwindled by -9.3% between 2019 and 2024.

-

Stablecoins as a "Digital Vault": In Peru, we don't use stablecoins to escape a failing currency, because obviously our Peruvian Sol (PEN) remains stronger than ever, but to safeguard capital outside a local system plagued by crime and data breaches. Clearly, the adoption of Stablecoins in Peru is merely starting. Only a very few percentage of people use it on a daily basis, I dare to say that 1/10 citizens use it or understand what is a stablecoin and how it works,

Figure 3: The Peruvian Paradox Visualized. Beyond the stable macroeconomic data lies a fractured reality defined by systemic corruption, insecurity, and a shrinking middle class. This infographic illustrates why only a few Peruvians are adopting stablecoins (USDT/USDC) not as an inflation hedge, but as essential "digital vaults" to protect assets from institutional failure and facilitate the ongoing "brain drain."

My Personal Alpha Strategy: I do not let my capital lie dormant in a domestic bank, that would be a crime! My 2026 financial roadmap is entirely on-chain:

Binance Earn: For a steady 4% passive yield.

Aave Staking: Providing a robust 6.2% return.

Uniswap Yield Farming: Utilising more aggressive liquidity pools that yield up to 35%.

When I need to make a purchase, I simply transfer funds to my Lemon Cash wallet and pay by scanning QR, POS contactless, or simply using the phone number. In 2026, retail friction has been phased out; digital wallets (Yape, Plin) are now ubiquitous, meaning the infrastructure for a crypto-powered lifestyle is already fully operational.

Figure 4: Bridging the Gap to Daily Commerce. This collage highlights the practical application of fintech platforms like Lemon Cash, enabling users to spend their crypto holdings seamlessly. It offers visual proof that stablecoins in Latin America have evolved beyond speculative assets into essential tools for everyday transactions, from buying groceries to filling up a gas tank.

B2B Adoption and the "3.5% Premium": The Hidden Engine of Digital Growth

To discern where the "serious" capital flows in 2026, one must look beyond retail users and focus on the Affiliate Marketing and Media Buying sectors. Professionals like Marcela, my dear friend based in Antofagasta, Chile, often manage advertising budgets peaking at $20,000 USD per campaign. For them, traditional banks are not partners; they are bottlenecks.

To the uninitiated, a 3.5% loading premium on stablecoin-funded virtual cards might appear exorbitant. However, for a high-volume founder, this fee is deemed a perfectly reasonable "continuity insurance".

Why does the B2B sector embrace this premium?

-

Protection Against "Security" Paranoia: Legacy gateways like Mercado Pago are prone to rejecting international payments for vague "security reasons," holding funds for up to seven days. In a $20k campaign, such a delay is tantamount to bankruptcy. Stablecoins in Latin America provide immediate, final settlement.

-

The Spectre of Arbitrary AI Bans: We’ve witnessed numerous instances of Stripe accounts being shuttered without warning by automated risk models, often on a Sunday when support is unavailable. Using $USDT-funded cards mitigates this deplatforming risk.

-

Overcoming BIN Discrimination: The industry has long been hamstrung by failures where virtual cards from Revolut or Wise were rejected simply due to their country of origin (BIN mismatch). Modern crypto cards allow businesses to circumvent these regional barriers, offering seamless global liquidity.

-

Resilience Post-Prisma 2025: The 2025 Prisma/Visa glitch, which duplicated transactions and exhausted credit limits across the region, served as a grim wake-up call. Market leaders realised that relying on centralised ledgers was a risk they could no longer afford.

For these entrepreneurs, the 3.5% fee isn't a cost; it’s the price of autonomy. It is the difference between a business that scales 24/7 and one that remains at the mercy of a local bank manager’s whims. Without stablecoin infrastructure, Latin America’s digital export economy would simply grind to a halt.

Adoption of Stablecoins in Latin America 2026

The adoption of stablecoins in LatAm is far from monolithic. In 2026, the region represents a highly nuanced mosaic where each market is underpinned by unique regulatory frameworks, inflationary pressures, and financial cultures. What serves as a multi-billion dollar institutional play in Brazil is a vital tool for survival in Venezuela.

Below is a strategic analysis of the primary markets, featuring the voices of those navigating this landscape in real-time.

Brazil: The Institutional Juggernaut and the "Real Digital"

Brazil stands as the unrivaled behemoth of the region. By mid-2025, the country recorded approximately $318.8 billion in crypto value received—a staggering figure that accounts for nearly a third of the regional total. However, the rationale here diverges significantly from its neighbors: it is not one of survival, but of deep-tier integration.

-

Market Structure: In stark contrast to other LatAm nations, Brazil’s market is heavily institutionalised. Traditional giants like Itaú, Nubank, and Mercado Pago have mainstreamed access, offering crypto custody directly within their banking apps. The average user eschews the complexity of a "cold wallet"; instead, they seek exposure within their trusted financial ecosystem.

-

The Drex Factor: The advent of Drex (the Digital Real) by the Central Bank has compelled private stablecoin issuers to integrate with Pix, the country’s seamless instant payment rail. This has given rise to a hybrid ecosystem that is arguably unparalleled globally.

-

B2B Dominance: Over 90% of crypto flows in Brazil are stablecoin-related, primarily spearheaded by B2B cross-border settlements and high-net-worth individuals seeking USDT exposure without limiting their liquidity within the digital financial system.

Argentina: The Middle-Class "Financial Bunker"

Argentina remains the world’s quintessential laboratory for grassroots crypto adoption, with a total volume of $93.9 billion. Here, using stablecoins is far from a "fintech hobby"; it is a massive flight to safety.

-

Pattern of Use: Argentines do not "invest" in USDT; they inhabit the ecosystem. The local Peso is treated akin to a "hot potato", converted into stablecoins the moment it hits a bank account. Indeed, had it not been for the widespread accessibility of these digital lifeboats, the purchasing power of the middle class would have been irrevocably decimated.

-

The Milei Era: Under President Javier Milei’s administration, the legal recognition of crypto for formal contracts (such as property rentals) has legitimized the sector, pulling stablecoins out of the "blue" (informal) shadows and into the light of formal commerce.

-

Street Reality: With inflation closing 2025 at 31.40%, digital wallets have superseded the traditional "money-under-the-mattress" strategy. They have become the essential tool ensuring that a worker's monthly salary does not dissipate before their next visit to the supermarket.

Mexico: The Remittance Bridge and the Entry of Global Giants

Mexico presents a nuanced hybrid market with a volume of $71.2 billion. Whilst its "Fintech Law 2.0" provides regulatory clarity, the market’s bedrock remains the massive $63.3 billion US-Mexico remittance corridor.

In Mexico, stablecoins act as "transit currency." My friend Ariel (CDMX) leverages these rails to transmit value across the border in minutes, capturing the strength of the "Super Peso" for local spending. However, 2026 marked a tectonic shift with the entry of global payment incumbents.

-

The Market Signal: The launch of Visa stablecoin payments via the Bridge infrastructure (acquired by Stripe) has proved to be a paradigm shift. Adoption is no longer a niche pursuit; when a standard Visa card allows you to spend your USDT in LatAm at any merchant, the friction of "crypto" is rendered negligible.

Colombia and Peru: Resilience and the Cultural Barrier

These two nations illustrate the fascinating disconnect between top-tier macroeconomics and ground-level adoption hurdles.

The Remote Talent Hub: Colombia has positioned itself as a mixed market with surging interest in DeFi. Whilst political noise creates currency swings, the remote workforce has effectively decoupled from the local economy. Major players like Tether have recognised this, investing in local exchanges to bolster liquidity for B2B services. Here, the appetite for risk is higher, driven by a tech-savvy youth demographic.

Peru: The Trust Deficit and the "Logo" Bias: Peru presents a distinct behavioral anomaly in the region. Unlike its neighbours, adoption here is hindered not by a failing currency, but by a deep-seated cultural reliance on traditional banking. Despite the Sol (PEN) being the region's strongest currency, stablecoin adoption remains niche, confined to a very small vanguard of developers, freelancers, and astute remittance senders.

-

The "Logo" Barrier: The average Peruvian exhibits extreme reticence toward any financial instrument that lacks the "institutional seal" of a major bank (like BCP or BBVA). This risk-averse mentality means that platforms without a physical branch are viewed with suspicion. Consequently, millions continue to absorb exorbitant fees from legacy couriers simply because they fear the "digital unknown."

Take my cycling friend, Madellín (32).She sends $200 USDT monthly to her son studying in Buenos Aires. "I've been using Binance for two months now," she told me. "I send the money instantly and save the $5 fee Western Union charged me for years. I’d have saved a fortune if I’d known about this sooner."

Madellín represents the slow awakening of a demographic that is realizing the "safety" of banks is costing them dearly.

Venezuela: The Economy of Absolute Survival

Venezuela remains the region's most volatile case study. The recent capture of Nicolas Maduro has triggered a geopolitical earthquake, yet for the financial markets, the aftermath has been characterized not by relief, but by profound uncertainty. Contrary to the hope that political change would instantly restore faith in the Bolívar, the resulting power vacuum has caused local banking operations to enter a state of gridlock.

In this chaotic interim, stablecoins have morphed from a tool of resistance into the only functional infrastructure for daily survival.

-

The "Transition Spike": On-chain data reveals that in the weeks following the regime's collapse, stablecoin volume surged by 45%. With traditional banks paralyzed by audits and leadership purges, USDT became the de facto clearing mechanism for imports, food distribution, and medical supplies.

-

Voice from the Ground: Elena, a wholesale food distributor in Maracaibo, describes the current limbo: "Some people celebrated the capture, but the banks stopped working the next day. Nobody accepts Bolívares now because we don't know who is in charge of the Central Bank. Today, if you don't have USDT in your wallet, you cannot restock your inventory".

Venezuela proves that in times of extreme turmoil, legacy finance freezes, but the blockchain never sleeps. Stablecoins are currently bridging the chasm between the fall of a dictatorship and the reconstruction of an economy.

Demographics and Professions: Who is Powering the Stablecoin Shift in 2026?

The adoption of digital assets in Latin America has successfully moved beyond the exclusive purview of developers. As we enter 2026, the ecosystem has permeated the broader economic fabric, encompassing a diverse cross-section of the population, from C-suite executives to gig economy workers.

To gauge the current demand for USDT in LatAm, one must first analyse the stark socio-economic divergence: while Mexico’s middle class grew by 8.0%, Peru’s contracted by -9.3%. This disparity dictates whether a user’s adoption is predicated on operational efficiency or absolute financial survival.

Figure 5: Beyond the Niche: The Mainstreaming of USDT. This collage visualizes the horizontal expansion of stablecoin adoption in Latin America by 2026. No longer just for developers, digital assets have become essential tools for operational efficiency and financial survival across a broad spectrum of the workforce, from high-earning digital marketers and remote interpreters to essential gig economy workers across the region.

Generational Segmentation: From Savings to DeFi Speculation

The regional demographic profile has matured, revealing distinct patterns of interaction with the blockchain:

-

Millennials (Ages 25–40): This cohort remains the lynchpin of the ecosystem, with a crypto ownership rate of 21.9%. They are the architects of "Embedded DeFi"; for instance, over 130,000 users now capitalise on Lemon Cash’s "Earn" feature (leveraging protocols like Aave) to generate yields on their deposits, seamlessly bypassing technical barriers.

-

Generation Z (Ages 18–24): These are the digital natives of the Gig Economy. They frequently opt for payments via Binance Pay to circumvent the prohibitive fees associated with legacy platforms like PayPal for smaller projects (ranging from $100 to $500 USD).

-

Gen X and Boomers (Ages 45–65+): In jurisdictions like Argentina and Venezuela, adoption in this segment is purely defensive. Using simplified fintech interfaces, retirees now seek to insulate their nest eggs from annual inflation rates that wreaked havoc on purchasing power in 2025.

Professional Profiles and the "Crypto Payroll" Paradigm

The rise of the "Crypto Payroll" has engendered a new socio-economic class in LatAm: professionals who operate within a dollarised economy whilst residing in local-currency jurisdictions.

As illustrated above, stablecoins in Latin America have standardized global parity for the remote workforce. By receiving USDT or USDC, freelancers save between 3% and 5% compared to traditional SWIFT or PayPal rails, effectively "earning" an extra $30 to $50 on every $1,000 invoiced.

The Spectrum of Crypto-Paid Professions: Contrary to the popular belief that this is the exclusive domain of software engineers, 2026 data reveals a burgeoning diversity in roles settling via blockchain:

-

The Tech "Old Guard": Naturally, Smart Contract Engineers and Full-Stack Developers remain the highest earners, often commanding salaries upwards of $5,000 USDT monthly. For them, receiving crypto is not a preference; it is an industry standard tantamount to a hygiene factor.

-

The Creative & Operational Expansion: The most significant shift in 2025 was the proliferation of non-technical roles. We are now witnessing a predominance of:

-

Community Managers & Moderators: Managing Discord/Telegram communities for Web3 protocols.

-

KYC/Compliance Analysts: Local lawyers or legal experts hired by global exchanges to navigate regional regulations.

-

Virtual Assistants & appointment Setters: A massive cohort in Colombia and Argentina, utilizing platforms like Ontop or Bitwage to receive micro-payments that would be rendered unviable by SWIFT fees.

-

The "Hybrid" Payroll Model: A trend that has gained traction among forward-thinking HR platforms (like Deel or Ontop) is the "Split Payment" feature. This allows a graphic designer in Brazil, for example, to allocate:

-

60% to a local bank account (Pix) for rent and groceries.

-

40% directly to a non-custodial wallet (USDC) for long-term savings.

This model has proven instrumental in onboarding the "crypto-curious" demographic, as it mitigates the volatility risk while offering an entry point into digital assets.

The Rise of the "Stablecoin Yield Farmer" in LATAM

In 2026, a more sophisticated user archetype has emerged: the professional who has moved beyond passive "holding" to active "farming." Recent market data highlights strategies where users are achieving a 27% average APR on their stablecoins by leveraging lending protocols like Uniswap and aggressive liquidity pools.

For an executive or senior consultant with a $50,000 USD fund, this translates to roughly $1,121 USD in monthly passive income. This figure is significant not merely because of its volume, but because it dwarfs the local minimum wage in most LatAm nations.

-

The "Carry Trade" of the People: We are witnessing a democratization of the "carry trade." Users accrue capital in stablecoins and allocate it to high-yield DeFi protocols, effectively creating a self-sustaining income stream that outstrips any traditional savings account offered by local banks, where rates often struggle to match inflation.

-

The Risk Profile: Unlike the "degen" gamblers of 2021, this 2026 cohort is risk-aware. They utilise insurance protocols and diversified pools, viewing DeFi not as a casino, but as a high-performance savings account that has finally leveled the playing field between Latin American savers and global capital markets.

Real-World Utility: From Caracas to the São Paulo Metro

While in some countries like Peru they have barely heard about stablecoins, in Venezuela and Brazil citizens use them to buy everything from essential items to mundane utensils.

-

Venezuela (The Structural Alternative): In cities like Caracas and Maracaibo, USDT has become ubiquitous. From small neighbourhood kiosks to large import firms, merchants use Tether to settle invoices and hedge against persistent inflation. They cite a newfound "financial peace" in their daily operations, as the ability to transact instantly in hard currency has mitigated the anxiety of holding depreciating Bolívares.

-

Brazil (Daily Efficiency via Pix): Adoption here is defined by seamless interoperability. Users like JoseDryBit are closing out 2025 by paying for public transport (metro and buses) using the DOC stablecoin directly via Pix. This demonstrates that on-chain banking is no longer a parallel system but is becoming fully integrated into the region's most efficient local payment rails.

-

Peru (The Remittance Revolution): The case of Madellín in Lima serves as a microcosm of a macro trend. By bypassing legacy intermediaries, the $5 saving per transaction may seem scant in isolation, but when aggregated across millions of users, it represents a massive shift in capital efficiency. This "Remittance Revolution" is effectively siphoning profits away from usurious traditional institutions and putting them back into the pockets of families who need them most.

Best Stablecoins in LATAM this 2026

As we enter 2026, the Latin American stablecoin ecosystem has matured into a global powerhouse, processing an astronomical $1.5 trillion in cumulative volume over the last three years. This growth is not driven by mere speculation but by a fundamental shift in how the region interacts with money. Users have moved beyond "crypto fashion"; they now discern their digital dollars based on specific risk profiles and operational utility.

Now, I have to be crystal clear with this. More than 90% of the market is dominated by USDT and USDC. These, without fear to mistake are the most important Stablecoins in Latin America. However, there are others that are being merely used by a tiny group of people.

1. Tether (USDT): The King of "Street" Liquidity

USDT maintains its hegemony with a regional market share hovering between 45% and 50%. It remains the undisputed de facto reserve currency for the informal economy and retail savings, serving as a bulwark against monetary erosion.

-

The TRON Factor: Its dominance is largely underpinned by the TRC-20 network, which allows for near-instant settlements with gas fees costing mere pennies. For the average user, this low friction is paramount.

-

A Tool for Survival: In Argentina and Venezuela, demand is inelastic. Families convert their wages to USDT immediately to mitigate the daily depreciation of local currency. As analyst @Juna_es noted on X, USDT provides a sense of "financial peace" for daily business operations, from small grocery stores in Buenos Aires to import firms in Caracas, where liquidity is of the essence.

2. USD Coin (USDC): The Institutional "Crypto Payroll" Standard

While USDT rules the street, USD Coin (USDC) has established itself as the lingua franca for the corporate and regulated banking sectors. With a global market cap of ~$76 billion at the start of 2026, it is the asset of choice for those prioritising transparency over anonymity.

-

Global Payroll Rail: For employers in the US and Europe, USDC is the "safe" option for paying LatAm contractors via platforms like Deel, Ontop, and Bitwage. Its stringent compliance standards make it the preferred conduit for formal salaries.

-

B2B Corridors: It serves as the engine for cross-border trade between Mexico and the US, reducing settlement times from days (via SWIFT) to minutes, effectively streamlining international commerce.

Insights from the Ground (Mexico City): My friend Ariel, an appointment setter for a Florida-based consultancy, explains the reality: "When I started working remotely, bank fees and PayPal commissions were a nightmare; I felt like I was losing a full Netflix subscription every time I got paid. Now, I receive my salary via Deel directly in USDC. For me, it’s about the peace of mind that comes with an audited, serious asset that my local bank won't flag because the source of funds is transparent."

Local Currency Stablecoins: The Giants of Internal Commerce in LATAM

While dollar-pegged giants monopolize international flows, Latin America has cultivated a unique ecosystem of indigenous stablecoins. In 2026, we are witnessing a clear bifurcation: users hold USD assets (USDT/USDC) for long-term wealth preservation, but increasingly rely on local-currency tokens for domestic operational velocity.

Top 3. Brazilian Real-Pegged Stablecoins (BRZ, cREAL, BRL1)

Brazil is the region’s institutional trailblazer. Here, local stablecoins aren't just for early adopters; they are being pushed by traditional heavyweights like Itaú and neobanks like Nubank.

-

The BRL1 Consortium: This isn't a solo effort. BRL1 is a strategic consortium backed by Bitso, Mercado Bitcoin, and Foxbit, designed to provide a secure, overcollateralized digital Real for institutional treasury.

-

The "Pix" Symbiosis: Their massive adoption is underpinned by seamless integration with Pix. These tokens act as the bridge between traditional banking and DeFi, fueled by the 2023 Virtual Assets Law (BVAL) which gave corporations the legal "green light" to treat digital assets as cash equivalents.

-

Motivator: Beyond payments, neobanks are using these tokens for loyalty and rewards programs, where users earn yield on their Real-pegged balances.

Top 4: Mexican Peso-Pegged Stablecoins (MXNB, MXNe)

In Mexico, tokens pegged to the peso (like MXNB and MXNe) are experiencing exponential growth scenarios. They have carved out a niche by focusing purely on domestic operational efficacy and alleviating the friction of everyday payments.

-

The SPEI Ramp: Their competitive edge lies in direct integration with Mexico's SPEI interbanking system. This provides incredibly streamlined on/off-ramps for fintechs, making them the preferred conduit for B2B operations that require blockchain speed but local currency denomination.

-

Everyday Utility: While their total volume pales in comparison to USDT, their transaction count is surging. They are being adopted for payroll and supplier payments where using a volatile crypto asset makes no sense, and traditional banking is too sluggish.

- Institutional Push: Mexican fintech laws have matured, allowing payment processors to use peso-stablecoins to lower the cost of cross-border B2B transactions by up to 50%.

Top 5: Argentine Peso-Pegged Stablecoins (wARS, ARGt)

In Argentina, a land historically fixated on the dollar, a fascinating counter-trend has emerged. Local players like Ripio and Twin Finance are spearheading the adoption of peso-pegged stablecoins like wARS and ARGt.

-

Transactional Speed, Not Savings: Let's be unequivocal: nobody in Argentina is using wARS to accrue wealth (that is the role of USDT). These tokens are utilized strictly for transactional velocity. They allow users to circumvent slow, expensive, and often frozen traditional banking rails to execute payments.

-

The "Bridge" Asset: They serve as a crucial, ephemeral bridge for instant liquidity. This allows users to step out of the dollar ecosystem for a specific payment and immediately step back in, mitigating exposure to the physical peso's volatility.

CMO Insight: The "secret sauce" for adoption in 2026 isn't the technology, it's Embedded DeFi. When a user in Brazil earns "stablecoin points" in their banking app, or an Argentine freelancer gets a "instant settlement bonus" for using digital pesos, the barrier to entry disappears.

Figure 6: The Shift Toward Domestic Digital Fiat. This visualization captures the 2026 reality of new Stablecoins in Latin America the strategic use of BRZ and BRL1 via Brazil's Pix system, MXNB's integration with Mexico's SPEI for corporate payroll, and the use of digital pesos like wARS in Argentina for transactional velocity.

The DAI Paradox: Why DeFi Ideology Fails in Latin America

Within the Latin American stablecoin ecosystem, there exists a striking sociological dissonance: while the cypherpunk narrative of decentralisation should, in theory, resonate with populations that harbor a deep distrust of local banks, the empirical reality is that DAI holds a negligible market share compared to the giants USDT and USDC.

What exactly is DAI?

Unlike its centralised competitors, DAI acts as an algorithmic fortress. It does not derive its value from physical dollars sitting in a bank vault. Instead, it operates through the Maker Protocol (now evolved under Sky), which locks crypto-assets, such as ETH or WBTC, on the blockchain to over-collateralise every coin issued.

The Roadblocks: Why Latin American users eschew DAI?

Comprehensive adoption studies reveal that in a "survival economy," practical utility invariably trumps ideological purity. These are the critical factors stifling DAI’s growth:

-

The "Gas" Barrier: DAI is native to the Ethereum network (ERC-20), where transaction fees can oscillate between $2 and $15 USD. For a user in Venezuela or Argentina needing to settle a micro-payment for lunch, this cost is prohibitive. Meanwhile, USDT on the Tron network offers transactions for mere pennies, making it the only viable option for daily commerce.

-

P2P Liquidity Friction: On platforms like Binance P2P—the "central banks" of the region’s informal markets—DAI’s order books are skeletal. While a user can liquidate USDT for local currency in seconds, DAI users face wider spreads and fewer counterparties. It is not uncommon to find DAI trading at a discount (e.g., $0.991 vs $1.00), forcing users to absorb a slippage that is unacceptable when moving essential funds.

-

Cognitive Overhead: This is perhaps the highest wall. The concept of "a dollar in a bank" (USDT/USDC) is intuitive. Explaining that DAI maintains its value through collateralised debt positions (CDPs) imposes a heavy cognitive load that is difficult to justify to a business partner during a financial crisis.

-

The "Sky" Identity Crisis: The 2025 rebranding to "Sky Protocol" and the introduction of the USDS token generated massive ambiguity. For the average user, the introduction of "freeze functions" in USDS eliminated DAI's main selling point (censorship resistance), leaving them with a product that was harder to use than Tether but offered no distinct advantage.

My friend Ariel (Mexico City), tells me about his experience using DAI "Look Julio, here in Mexico, USDT and USDC are the standard, BUT, I’ve been offered payments in DAI before, but I hesitate. It feels esoteric.

More importantly: if all my expenses are in fiat or card payments, why would I fill my wallet with an asset that requires an extra swap?

I’d just have to convert it to USDT to send it to my VISA card. That's an unnecessary redundancy, so I always demand payments in USDT or USDC."

2026 Horizon: The Future of Stablecoins in LATAM

As we gaze into the remainder of 2026, it becomes evident that the Latin American stablecoin market is no longer in a phase of discovery, but of structural entrenchment. The region is evolving along three strategic axes that will define the next decade of emerging market finance:

From Speculative Frenzy to Survival Infrastructure

The era of crypto as a "casino" has been definitively eclipsed by the era of utility. 2026 marks the psychological pivot point where users have ceased seeking tokens that promise to "go to the moon"; instead, they demand assets that simply ensure their purchasing power remains on solid ground.

The narrative has shifted from wealth creation to wealth preservation. In this context, stablecoins have graduated from being a niche fintech experiment to becoming the bedrock of operational efficiency for the working class.

The Era of "Invisible" DeFi

We are witnessing the total abstraction of the blockchain. The complexity of keys, gas fees, and protocols is rapidly disappearing behind sleek user interfaces.

-

The "Mullet" Strategy: Apps like Lemon Cash and Belo have perfected a hybrid model: "Web2 in the front, Web3 in the back".

-

Automated Yield: Users are increasingly engaging with protocols like Aave not through direct interaction, but via "savings accounts" in their local apps that automatically route capital to yield-bearing contracts. The average user is agnostic to the technology; they care only that their balance grows in real-time, insulated from technical friction.

The Great Regulatory Bifurcation

A profound schism is redrawing the regional map. A clear line has been drawn between the "sunlit" regulated markets and the "grey" survival economies.

-

The Institutional Path: In Brazil and Mexico, frameworks like Drex and BVAL are pushing liquidity toward compliant assets like USDC, integrating them deeply into the banking core.

-

The Shadow Efficiency: Conversely, in Argentina and Venezuela, USDT will continue to reign in the shadows. Here, it acts not merely as a currency, but as the lubricant of the real economy, thriving precisely because it operates outside the purview of state controls that have failed to tame inflation.

In 2026, the question is no longer if stablecoins in Latin America will be adopted, but how deeply they can be integrated before the legacy financial system is rendered obsolete.

The On-Chain Lifestyle in 2026. By 2026, retail friction has been phased out as crypto cards in Latin America become ubiquitous. This visual represents a financial roadmap that is entirely on-chain—utilizing stablecoins in Latin America for everything from high-yield staking on Aave (6.2%) to daily purchases made via contactless POS or QR scans in local markets. In Peru, these cards act as "digital vaults," protecting capital from local systemic risks while providing instant liquidity for the 2026 economy.

Ready to Capture the $1.5T LatAm Opportunity?

Navigating Latin America’s financial friction requires more than just translation. I help Web3 founders and global fintechs build authority and penetrate regional markets through data-backed content strategy. Having delivered over 40 deep-dives for brands like Molecula.io and KeyTether, I provide the strategic bridge between your product and the LatAm user.

✍️ Written by El Salvador CopyBiker — Crypto Content Specialist.

Helping your audience actually understand your Web3 product (no PhD required).