TL;DR: Here I share my experience using two types of crypto cards in Peru: Lemon Cash and TONCard. Although I hold crypto in both, they differ significantly in terms of usability, privacy, and security. Lemon offers superior practicality, allowing me to use it easily with friends, local shops, and online businesses. TONCard, on the other hand, allows me to spend my crypto with complete anonymity, so I do not hand over my data to any bank, yet I can still pay anywhere, physically or virtually, that accepts VISA.

As you should already know, I am a freelancer in LATAM, living in Peru, a global gastronomic powerhouse with marvellous biodiversity. However, if there is one thing we lack, it is the technological advancement enjoyed by nations such as China, USA, Rusia, Australia or Singapoure.

Nevertheless, I have managed to adopt stablecoins in my day-to-day life. As I have dedicated myself to Copywriting specialised in Crypto and Web3, I believe I should set an example for others. I have now been using two crypto cards for three months: Lemon Cash and TONCard. While both function using crypto, they have distinct particularities that may be more valuable to some than others.

If you are a freelancer like me, based in LATAM or another developing region, and you earn in Stablecoins (USDT or USDC), this article will help you understand that not all crypto cards are created equal, and help you see which one is right for you.

Have you got your coffee ready? Let’s begin.

The Reason I Started Using Crypto Cards in Peru as a Freelancer

I can still remember it as if it were yesterday, seeing my first PayPal statement. I was horrified. I saw withdrawal charges of US$10 just for transferring my PayPal balance to my Scotiabank account (a Peruvian bank). In total, I had made three withdrawals... meaning they had essentially "robbed" me of 30 dollars just for accessing my own money.

Frustrated and disappointed, I began searching for cheaper alternatives. I found Payoneer, which charged a maximum commission of 3 dollars per withdrawal. It was a significant reduction compared to PayPal, but it still hurt.

To cut a long and boring story short, I opened an account on Binance and started receiving payments in my USDT wallet. My clients from Mexico, Russia, and Turkey paid directly to my address, and I received the funds in minutes. When I wanted to use that money, I sold it via P2P trading, and the funds would arrive in my Scotiabank account.

I used the Plin application to pay for everything. But Plin always seemed to fail me at night, especially during the most pressing situations. Sometimes I would be left waiting for half an hour for the system to fix itself... just awkwardly staring at the waiter, hahaha.

So I asked myself: Isn't there a way to spend crypto directly? I knew the Binance Card existed, but unfortunately, it is not yet available in Peru.

What Types of Crypto Cards Exist and How They Work in Peru

Then, as if summoned by my very thoughts, an advertisement reached my ears: Lemon Cash. It was a crypto card that promised the ability to receive and send cryptocurrencies, as well as the option to pay with both crypto and the country's local currency—in my case, Soles. Put simply, it works for paying with both crypto and fiat.

The second crypto card was TONCard. A new card that was almost the same as the previous one, but with something special: it does not ask for personal data. This was completely bizarre to me. And I mean that seriously, because I was accustomed to always handing over my ID card, email, bank account number, and a photo of my passport. Yet here, with just my Telegram account, everything was ready to go!

First type: Crypto Cards with Full KYC in Peru - LATAM (Like Lemon Cash)

Full-KYC cards are issued by regulated fintechs and exchanges. To get one, you must open an account, submit your ID and a selfie, and pass compliance checks. Once approved, you can spend your crypto or local fiat via Visa or Mastercard rails.

How they work: Your crypto (or Pesos/Soles) sits in a custodial wallet. You can set your primary payment currency (in my case, I use Peruvian Soles) and a backup currency (for which I hold USDT). So, when you make a payment, the application uses the currency you have configured first; if that balance runs out, it automatically switches to the backup currency using the app’s exchange rate.

Examples of crypto cards in LATAM:

-

Lemon Cash (Argentina / Peru) – This is what I am currently using now.

-

Ripio Card (Brazil / Argentina, etc.) – A prepaid Visa that lets you pay with either pesos or more than 20 cryptocurrencies, earning around 2% cashback in stablecoins or BTC/ETH for every transaction.

-

Belo Mastercard (Argentina) – An international prepaid Mastercard linked to the Belo wallet. Users can hold ARS, USD, USDT, USDC, BTC, and ETH, and spend in any currency while merchants receive local money.

-

Tulkit Pay Mastercard (Peru) – A Peruvian crypto wallet that requires ID verification. It lets you deposit Soles via bank transfer or local apps like Yape/Plin, buy BTC/USDT, and then pay in local currency with a physical or virtual Mastercard (I haven´t used that and neither my friends).

-

Crypto.com Visa Card (LATAM expansion) – This is a global crypto Visa card now available in Latin America, offering tiered rewards. Like other major crypto cards, it requires full KYC before issuing the card.

Second Type: Crypto Cards Without (or Very Low) KYC in Peru - LATAM (Like TONCard)

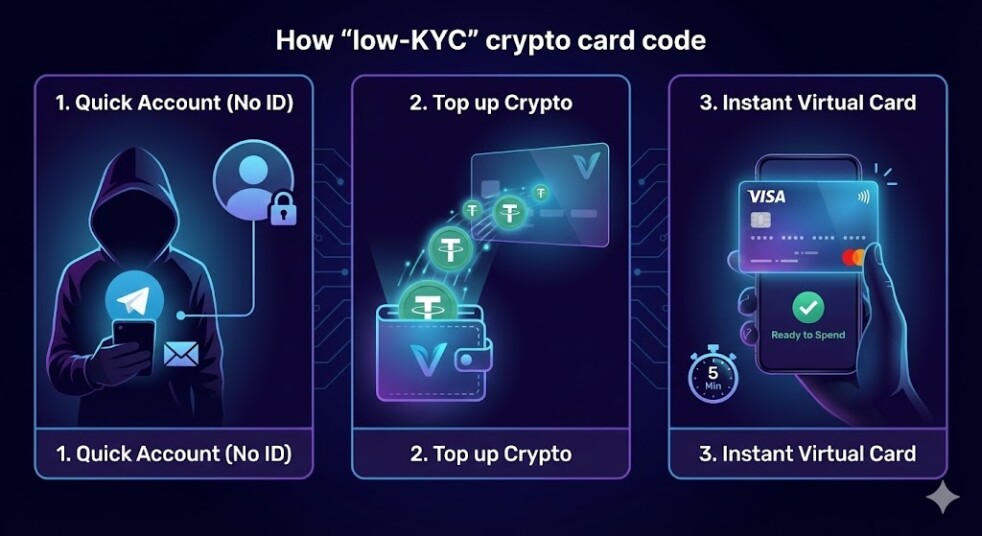

This type of cards minimise traditional ID checks. Some ask only for an email or wallet connection; others market themselves as no-KYC, often with lower limits and higher regulatory risk.

But how anonymous crypto cards work: First, you create a user account with your email or Telegram handle. Then, the provider generates a virtual crypto card and a wallet address for you. You send USDT or any cryptocurrency to that address to top it up (in my case, I recharge it from Binance, which is where I receive my money). In less than five minutes, it is ready to spend.

Examples of pseudonymous and anonymous crypto cards in LATAM:

-

TONCard – The crypto card I am currently using. - Pretty cool so far!

-

Xkard – A global “no-KYC” crypto card brand marketed as LatAm-friendly. It is reloadable with crypto and compatible with Apple Pay and Google Pay, focusing on fast onboarding and spending freedom, albeit with an unclear long-term regulatory status.

-

Bitsika Crypto Virtual Card – A virtual Visa card funded with Bitcoin or USDT, explicitly advertised as requiring no KYC to create or use the card. It supports Apple Pay, Google Pay, and PayPal for online spending.

-

BingCard – A service issuing virtual and physical crypto debit cards in minutes with no document upload. It can be recharged with BTC, USDT, ETH, or USDC and is often used for subscriptions and digital services, though it comes with transaction limits.

-

Buvei Virtual Cards – KYC-free, USDT-funded virtual cards positioned for private online payments and subscriptions. They offer quick issuance and global online acceptance but operate in a regulatory grey zone and are subject to changing rules.

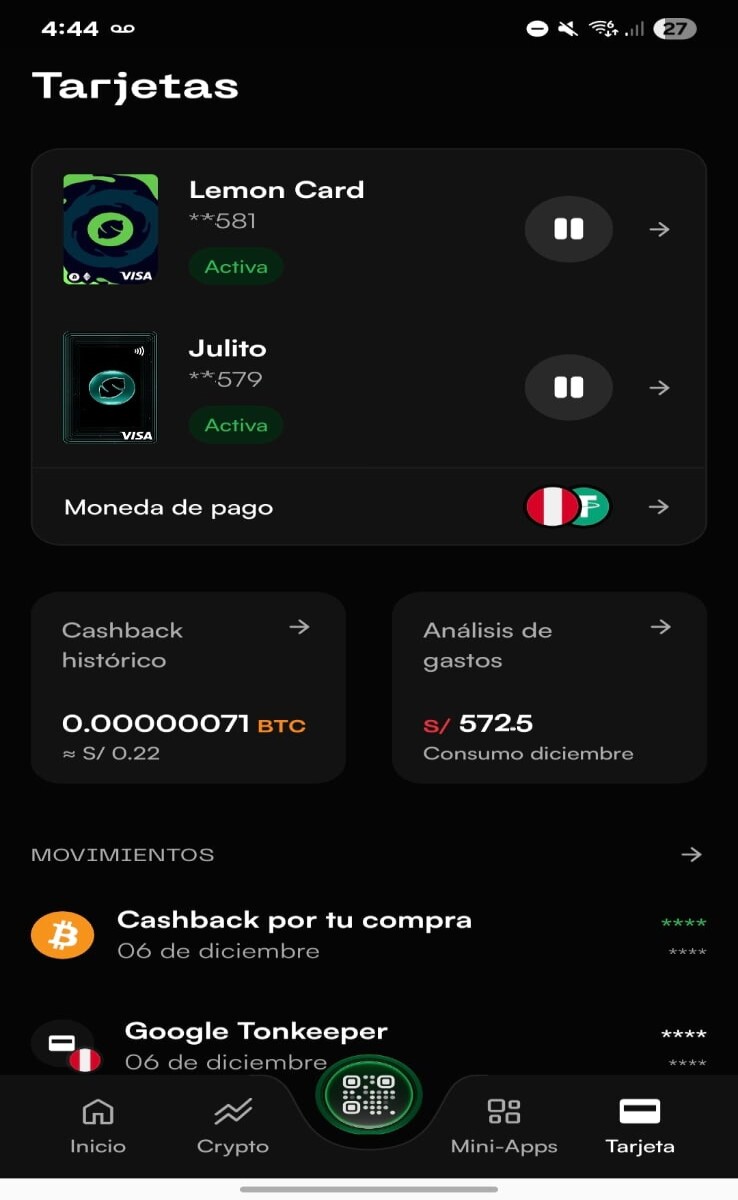

Lemon Cash Peru Review: How I Use This Crypto Card Every Day

For me, using Lemon Cash for payments is almost identical to using Plin or Yape. If I pop down to the shop for a couple of beers to watch the Peru vs. Chile match in the Copa América, I can pay the owner simply by using her mobile number or by scanning the shop's Yape or Plin QR code.

Opening My Lemon Cash Account and Passing KYC

As I mentioned earlier, these types of crypto cards ask for every single detail under the sun. That is precisely what "Know Your Customer" (KYC) is all about. To be honest, it was tedious taking selfies, typing out my card number, my email, my occupation, and declaring where the money I received came from... and they took 48 hours to validate my data.

This is because they must comply with the guidelines established by Peruvian fintech regulations. They hold my data... the downside is that if they suffer a data breach, I am in serious trouble. In reality, we are all in trouble because there are many ways that data can be used to ultimately steal your money.

Once my account was ready, I proceeded to create my USDT wallet address on the TRON network within Lemon. I used that address to send myself 100 USDT from my Binance account. My plan was simple: convert them into Soles and use them for my day-to-day expenses.

But there was one final step needed for maximum practicality and to use it anywhere: connecting it to my Google Pay wallet. With this, I could pay at any establishment that accepts VISA.

Paying in Soles With the Lemon Cash Visa Card

I must mention that Lemon Cash does not suffer from the problems that many digital wallet users complain about with Plin and Yape: network failures, duplicated payments, or money that never reaches the recipient. So far, the app has not failed me in that regard.

-

I go to the market to buy fresh vegetables and pay with my crypto Lemon Cash by scanning the QR code.

-

I go to the butcher to buy chicken, beef, and pork, and I pay with my crypto Lemon Cash by scanning the owner's QR code.

-

I go to the petrol station to fill up my blue Volvo, and I pay with my crypto Lemon Cash card using the POS terminal that accepts VISA.

-

I can buy fresh fish to prepare my ceviche (with plenty of chilli) by paying with my crypto Lemon Cash card, scanning the business's QR code.

-

My friend wants me to send him 10 Soles to pay for the rental of the football pitch; I pay him using his mobile number.

-

If I wish a traditional emoliente, I can pay the owner using his QR.

As you can see, Lemon Cash works for practically everything. That is why I hardly ever use Plin directly anymore... and whenever someone sends money to my Plin, I immediately transfer it to my Lemon.

Pros and Cons of Lemon Cash for Freelancers in Peru - LATAM

By now, you are probably charmed by Lemon Cash due to all its possibilities, but I must warn you the risks or potential issues.

Why You Should Never Use Lemon Cash if You Live in Peru

It is not a bank and, therefore, does not offer a deposit insurance fund. As you know, any Peruvian holding a sum of up to PEN 120,000 in a formal bank is covered by this sort of insurance in case the bank becomes insolvent or goes bankrupt. Conversely, if you hold more than 50,000 in Lemon and it runs into financial trouble, your cryptocurrencies have no backing whatsoever.

Furthermore, being a platform with strict identity verification (KYC), it centralises millions of user data points. This information is valuable and makes them a prime target for hackers. Just imagine it:

-

Email addresses

-

Card numbers and expiry dates

-

Your mobile number

-

Your home address

-

Source of income

-

Fingerprints

-

ID number (DNI), full names, date of birth...

Imagine all of that in the hands of hackers. Okay, no... let’s not imagine it; it would be catastrophic. But clearly, it opens many doors to Phishing attacks, identity theft, and impersonation, which would allow attackers to access other accounts or perform financial transactions in your name.

Imagine receiving an email saying: "Congratulations, your loan has been approved," and you had absolutely no idea about it!

The TONCard Review – A Web3 Virtual Crypto Card for Anonymous Global Payments

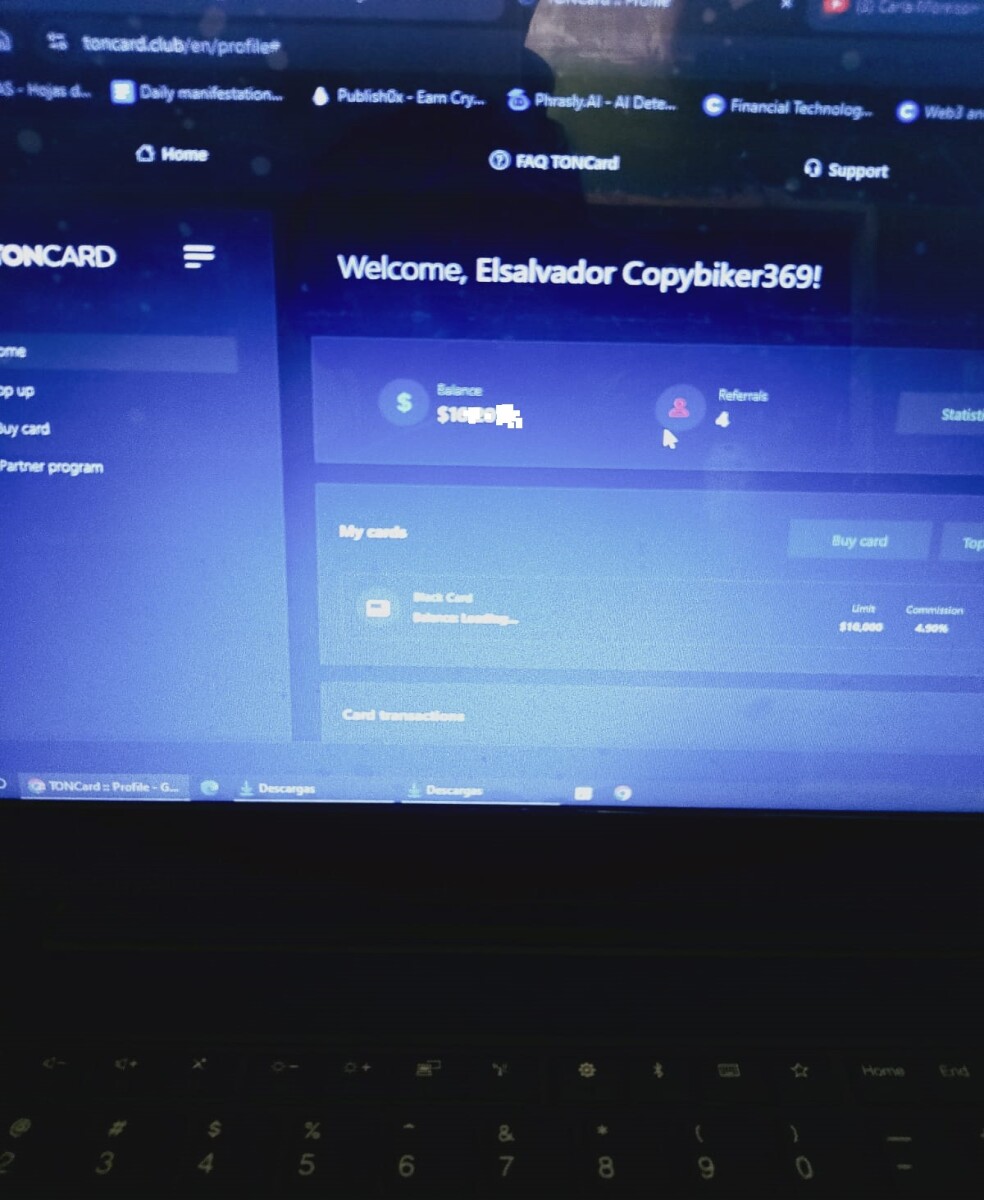

This crypto card shattered my paradigms. Opening the account was so, so simple that it almost seemed illegal. Truly! To create my account, I had the option to use my Telegram account, Google email, or another type of email. In my case, I chose the first option. It was the only piece of data they asked for.

Once my account was ready, I had to choose which type of card I needed. There were three options, but I only wanted the most basic one to test how well it worked, so I allocated a small amount to use for my daily expenses.

How I Top Up TONCard with USDT From My Favorite Exchange

Finally, I settled on the basic card, which has a one-off fee of 10 USDT. So, I sent 50 USDT to it from my Binance account.

Once I had my card and my first balance of 50 USD, I was able to name the card; in my case, I named it "El Salvador Copybiker". That is to say, it is pseudonymous.

It is not a physical card; it is 100% digital.

What I Pay With TONCard: Subscriptions, Travel, Online Services

Normally, I only use it to pay for flight bookings, my Meta Ads bill, Netflix, YouTube Premium, etc., from my computer... but it offers a more interesting option: connecting it to your Google Pay wallet.

After that, I am ready to spend at any shop, supermarket, or restaurants like Pollería to share a delicious Pollo a la Brasa with friends. Always asking if they accept VISA.

Pros and Cons of TONCard for Crypto Natives

TONCard markets itself as a crypto Visa card that prioritises privacy and anonymity.

Why do I like using TONCard in Peru?

-

I can use my crypto directly without it passing through a national bank, saving me a lot of time and absurd commissions.

-

My personal data is not exposed, and even better: I spend without having to answer to anyone.

-

No one is going to close or block the account for "suspicious activity".

-

I keep my balance in dollars, and my money goes further due to the exchange rate.

Why wouldn't I use TONCard for my purchases in Peru?

Just like Lemon Cash, it does not have a deposit insurance fund, unlike banks.

But that is precisely why I only top up the monthly amounts I plan to use. I know I will use a maximum of 500 USDT per month, so that is what I send. If anything were to happen, my exposure would be limited.

Its use is limited only to businesses that accept Visa. This does hurt because I cannot pay anyone via Yape or Plin. But it’s fine, as almost millions of establishments in my country now accept Visa.

Understanding Which Crypto Card is Better for you: Lemon Cash vs TONCard

If You Live in Peru and Earn and Spend Mostly in Soles

If your salary lands in a Peruvian bank account and almost everything you pay is in Soles, a pure stablecoin card like TONCard rarely makes economic sense. You would need to convert PEN → USDT → USD every time, adding FX spreads, network fees, and extra steps just to end up paying for the same groceries or rent.

In that case, it is usually wiser to keep using local rails like Yape, Plin, and your regular debit card, and maybe have Lemon as a backup. You can move Soles from your bank to Lemon, try Bitcoin or stablecoins in small amounts, and still pay in local currency without becoming “full crypto”.

If You Are a Freelancer in LATAM Paid in Stablecoins like USDT or USDC

For freelancers and remote workers paid directly in USDT or USDC, the picture changes completely. Your “native money” is already stablecoins, so sending them to TONCard and spending via Visa can be very efficient, avoiding repeated conversions into local fiat and long waiting times with banks.

Here, it can make sense to use both Lemon and TONCard. Lemon acts as a regulated, KYC-verified hub where you can cash out to banks, earn yield, or swap between coins. TONCard works as the privacy-friendly spending rail when you just want to tap your phone in a restaurant or pay online without involving your local bank.

If You Want to Live as “Bankless” as Possible

“Bankless” here means minimising your dependency on traditional banks and living mostly in stablecoins and crypto wallets. If that is your goal, a pseudonymous card like TONCard fits better than a full-KYC fintech: you top up from your wallet and spend without sharing your full financial life with a local bank.

The trade-off is important: less bank visibility usually means less formal protection and more regulatory uncertainty, and it is harder to prove income for things like mortgages or business loans. Lemon, on the other hand, keeps you inside the regulated system. So going bankless with TONCard is a lifestyle choice, not a free upgrade—freedom comes with more personal responsibility.

FAQ: If You Are Thinking of Getting Your First Crypto Card in Peru - LATAM

What is the best crypto card to use for crypto in the world?

The best card is the one that matches how you get paid. If your income is fiat, use a regulated crypto card that communicates well with your bank. If your income is USDT or USDC, look for a card that you can top up directly from your wallet without ten extra conversions.

Can the tax authorities see all your transactions within your crypto Card?

Short answer: assume yes. With full-KYC cards like Lemon Cash, the answer is yes. Since you submitted your ID and personal details to open the account, these companies operate like regulated financial institutions. They record every transaction and are legally obliged to share that data with tax authorities if requested.

With anonymous cards like TONCard, the issuer cannot report you because they simply do not know who you are. However, you are not completely invisible. If you link the card to your personal Google Pay or provide your ID number (DNI) at a shop to receive an official invoice (boleta), you voluntarily create a link between that crypto spending and your real identity.

What happens if I buy $100 worth of Bitcoin inside my crypto wallet or crypto card?

If you buy $100 of Bitcoin within Lemon Cash, you now own a small slice of BTC. If the price rises, you can sell later and perhaps pocket a profit. If it drops, you lose value on paper. That is the game. Plan your entries, do not panic, and never invest your rent money.

Is a crypto card a credit card?

Usually, no. Most crypto cards are prepaid or debit-style cards. You must load them with your own money first, then spend. There is no classic “credit line” like a bank card. While there are some crypto credit products out there, most people in LATAM use the prepaid model.

Is it good to have a crypto card?

Used wisely, it is a killer tool. You can get paid in stablecoins, keep control of your money, and still pay in any shop that accepts Visa or Mastercard. The danger lies in forgetting that it is still real money: overspending in crypto hurts exactly the same as overspending in fiat.

✍️ Written by El Salvador CopyBiker — Crypto Content Specialist.

Helping your audience actually understand your Web3 product (no PhD required).