Continuing on the topic of real utility from the previous blog, there's a lot that can be learned from the phenomena of GameFi and FitFi ecosystems. In a nutshell, they seem like a brilliant idea. Instead of paying to use an exercise tracking app or to play a game, get paid!

Decentralized ecosystems, where there is the absence of an owning power whose sole purpose is to profit from the utility they provide for others, remove the "middleman" and distribute a portion of the profits to the users. This makes a great deal of sense given that the users are the ones who are needed to sustain and grow the value of the ecosystem -- the so-called "network effect" based on Metcalfe's Law.

So why did such projects like Axie Infinity and STEPN suffer from a severe drop in their respective token values?

The answer is straightforward:

- Their offering of real utility was supplanted to a large extent by financial utility, or the motive to gain profit.

Seeing how this diagnosis is true is somewhat more involved.

How GameFi and FitFi Make Money

How much do you want to pay in order to win?

With GameFi, payment can take at least a few forms:

- time (e.g. hours spent playing can translate to earning perks)

- collecting in-game level ups by playing

- paying for in-game level ups with money

With conventional digital games, players pay with returns only arising with respect to leveling up or winning. With Web3 games like Axie, there is also the possibility of trading any items earned or bought for actual money (well, into crytpo and then into fiat).

In-game items are usually required to progress to more optimal earning rates, and tokens can often be exchanged on decentralized exchanges for other tokens. Users can even exchange game tokens for fiat currency, but usually only at centralized exchanges.

A significant benefit of GameFi is financial inclusion. In other words, it adds another pathway by which a larger swath of people can make money. All one needs in order to earn is the appropriate hardware and software. Items required to play games — such as, NFT characters — can be rented out to those who may not be able to afford their own character. The player then shares a percentage of his/her earnings with the NFT owner.

Similar to GameFi, FitFi pays its users to engage in fitness activities, such as walking, jogging, running, and cycling. FitFi is therefore a “move-to-earn” platform which monetizes its users’ geo-location data. Data monetization is, of course, nothing new. On the fitness front, Fitbit monetizes its users’ data as a way of making profit. Fitbit is a standard, “centralized” privately run venture in that sense.

Where FitFi differs significantly is with respect to Web3 distribution and decentralization. Apps like STEPN take the earnings from geo-location data and share them with its users in the form of its native tokens. While not significant, such Web3 platforms pay you for doing something you ought to be doing. It’s an extra incentive to live a healthier lifestyle.

The token reward system underwrites a larger tokenomic system where the tokens paid to users go back into the ecosystem.

- Generally, in-app purchases must be made to remain active and increase one’s token earning rate.

- So users have to use native tokens on in-app purchases to increase their token earnings.

This tokenomics structure appears “virtuous” in that it keeps value in the system — to stay active, users need to buy items; to buy items, you need to stay active. Furthermore, it is based on real utility — exercising or, in the case of GameFi, playing a game (entertainment). (Yes, I count entertainment as real utility since it can have significant philosophical ramifications.)

A Virtuous or Vicious Circle? How Things Breakdown

On the face of it, both GameFi and FitFi seem like excellent examples of a virtuous circle of value creation and value giving. Participants are rewarded for doing the things they love, which in turn helps to create a better community for each respective ecosystem.

However, theoretical ideas involving economic behavior often fall prey to blind spots in not noticing how the path of least resistance to profit often throws a wrench (or spanner) in the works.

A significant drawback of GameFi is whether or not the gaming ecosystem is financially sustainable. If tokens and items have a financial value, players can cash out. When this occurs frequently and in large enough numbers, the ecosystem can crash. Indeed, if the value of the native token drops enough, it can cause a bank run on the token.

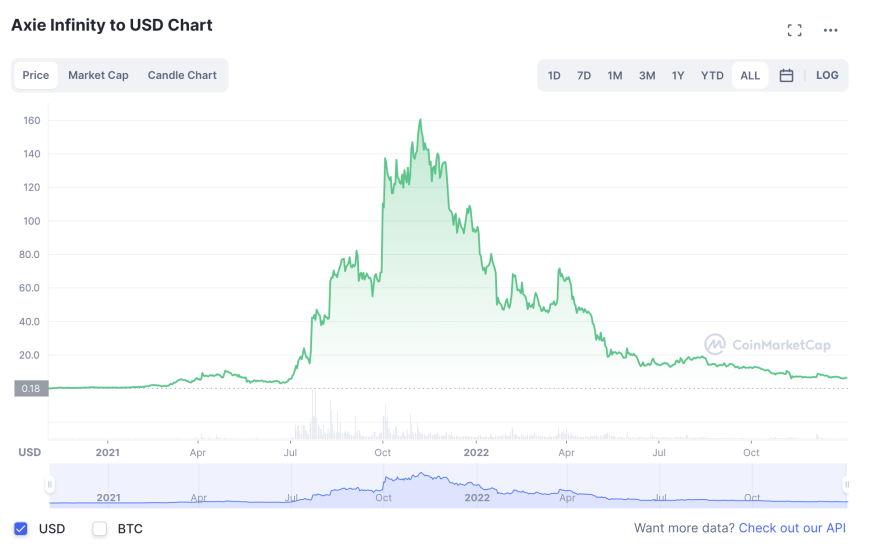

When this phenomenon significantly affects an ecosystem to the point where it looks like it cannot recover, it is referred to as a “death spiral”. Have a look at Axie's token value:

The peak and drop is often characteristic of dead or dying ecosystems. In one respect, if Axie is really about gaming with an added layer of paying back its members (now matter how little or how much), then the price of the token really shouldn't matter. Any payout is a perk. I'll come back to this in the final section under "dual value propositions".

The extreme and quick drop in value happened to STEPN, as well. (Axie in addition suffered from a hack of assets.). What we can learn from both cases are the conditions that herald a collapse:

- Users want to cash out the majority of their tokens, causing devaluation of the token as well as potentially creating a bank run when other users see the token value drop.

- The flow of new users slows or stops.

The latter is often cited as a criticism of FitFi and GameFi since it is alleged that the creation of value in the system relies on new users. This is true, but it’s important to note that both of these conditions are significant weaknesses in how most FitFi and GameFi ecosystems are constructed. So let’s break them down separately.

The Flow of New Users & Pyramid Schemes

Let’s take the second condition first since it’s easier to identify and unpack.

Critics often allege FitFi platforms like STEPN are “Ponzi schemes”. I often complain that this term is overused. (Here’s why.) In most cases, such as this one, the correct descriptor is “pyramid scheme”. Let’s take STEPN as a case study.

A Ponzi scheme is one in which the underlying asset has no value or utility. As noted above, STEPN provides real utility in terms of incentivizing exercise. So users are definitely getting something in return for playing.

More accurately, the problem with STEPN is that it is a certain type of pyramid scheme (a Ponzi can be a pyramid scheme; but a pyramid scheme is not necessarily a Ponzi scheme.) In other words, if the creation of value relies on the addition of new users, and if entering later into the scheme means paying a higher price than those who arrived earlier, then the ecosystem has a pyramid structure. In the case of STEPN, later adopters pay a higher cost in terms of a reduced token earning rate (as its value rises) and the cost of in-app items.

Nonetheless, pyramid schemes are not necessarily vicious if there is another route of value creation in the system. With FitFi, the monetization of data should theoretically provide a value support to the system. Instead of relying mostly on user growth, the ecosystem relies on the frequency of the activity of current users. Of course, new users help with the monetization effort, but it also means that the reliance on new users is less burdensome. Active users are what counts.

So why is it that the FitFi and GameFi ecosystems undergo what is often called “a death spiral” when their token value crashes and users flee?

The Death Spiral & Value Proposition

Pyramid schemes can function so long as the value of the asset driving the scheme retains utility value. Utility value is the value that users get from the a system or network for ends other than financial profit.

In the case of STEPN, this would mean that whatever the value one gets for exercising, the exercise and social connections would be the utility values that matter most. In turn, the native tokens that users earn would not really be subject to dumping since the main puposes would be exercise and connecting with others. A side perk is that some of the tokens can be exchanged for other currencies.

But alas, this was not entirely the case with STEPN.

And so we come back to the opening thesis about Axie and STEPN:

Their offering of real utility was supplanted to a large extent by financial utility, or the motive to gain profit.

The problem to highlight here is one of value proposition. In conventional games, that proposition is one of enjoying the use of the game or application. In cases of Play- or Move-to-earn, the value proposition can instead be dominated by the desire for profit.

When this occurs, it foregrounds financial incentives over the non-financial which sustain ecosystems like conventional games. STEPN is still active. While its token (i.e. GMT) value did crash from a high of almost $4 in April of 2022 to almost $0.40 at the time of writing, STEPN is still alive and kicking (sorry for the pun!). Not quite a death spiral (unless you were counting on STEPN being a moonshot). Rather, it would appear that in practice, the STEPN ecosystem was “over-financialized” to the point the motive for profit muted any gaming utility.

In fact, what one can say is that where an ecosystem offers real utility, the native token will probably level out to a more realistic price once all the hype settles and user adoption remains wedded more to use rather than price speculation.

In sum: The STEPN ecosystem is a pyramid scheme that relies on the influx of new users to sustain the value of its native token AND persistent user engagement. This design becomes problematic when the value proposition of the ecosystem provides little to no incentive to keep using the ecosystem, as opposed to cashing out by dumping the native token.

What, then, is the solution?

It’s all about a healthy, Dual Value Proposition.

A genuinely virtuous ecosystem does not solely rely on a single economic value proposition — most common of which is the incentive to profit. Economic behavior nudges related to profit need to be enframed by non-economic nudges or incentives. There are two types of non-economic nudges that come to mind:

Utility

While the term “utility” is used frequently to describe motivations for economic behavior, it is often reduced or confused with financial “utility” — that is, what is useful in making a profit. Non-financial utility, or “use-value” if we follow Adam Smith and Karl Marx, is that which enables us to perform our daily tasks or live aspects of our lives well.

A virtuous ecosystem is one in which use-value remains constant and dominant — that is, where financial utility may exist but does not outrun what is useful. In the case of STEPN, those who move-to-earn purely to make money may be engaging in the utility of exercise, but because their main motivation is profit, they will leave when the token value reaches a peak.

Moral Incentives

People driven by moral incentives will often engage in the action or behavior driven by such incentives regardless of profiting. Why? Because they see that it is the right thing to do without any external motivation. (Ok, how moral action and behavior is intrinsically motivated is a huge philosophical question. But let’s assume this relation.)

Given the prominence of moral incentive, any activity that has other perks will usually fail to supplant it. As Aristotle observed, a virtuous person does not engage in ethical action solely because it makes him or her feel good (i.e. feel pleasure); rather s/he does so for its own sake. When pleasure arises, it is a side-effect . . . no doubt, a welcome one.

Looking ahead (i.e. past the crypto winter of 2022), it seems that if a crypto platform wants to be viable, it will have to consider making at least one of these non-economic incentives central to its ecosystem.

Make it so!

About the Author

Todd Mei is the lead researcher and writer for 1.2 Labs, which is the consultancy group for the crypto hedge fund 1.2 Capital. He is a former Associate Professor of Philosophy at the University of Kent (UK), with specialisms in philosophy of economics, meaningful work, ethics, hermeneutics, and existentialism. His aim is to help innovative projects get on-chain in order to provide real utility to the world.

Portions of this article were originally published in Medium.