Introduction

A few years ago my employer offered a free Dave Ramsey course in financial literacy. Not only would taking the three-day course cost me nothing, but, even better, I got to do it on company time, making it a no-brainer to sign up.

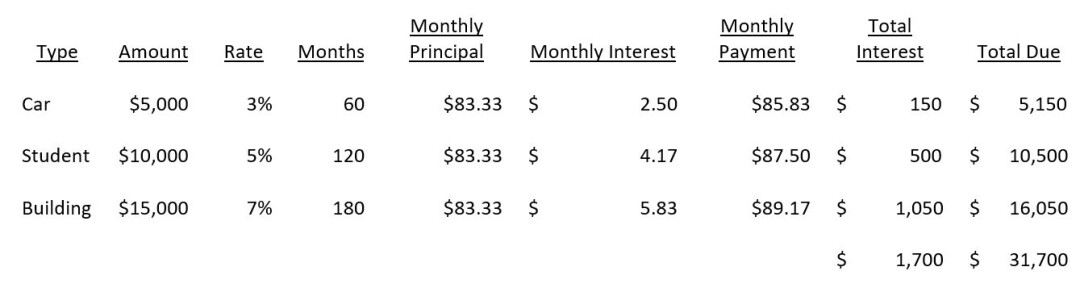

The course was interesting, and, although I went in as a skeptic, I found myself agreeing with most of his advice, even that which technically wasn’t the most logical, mathematically speaking. An example of this was his preference for the “snowball” method of debt erasure over the “avalanche” method. Imagine you have three sources of debt: a car loan of $5,000, a student loan of $10,000, and a building loan of $15,000. In the real world, how much you actually pay in interest on these loans varies by the interest rate, the length of the loan, whether it is simple or compound interest, and so on. But for ease of understanding, let’s just say they are all simple interest loans on the same terms, except for the rates and durations.

With a normal repayment strategy—that is, if you paid off each of the loans exactly according to the terms—you’d end up paying $1,700 in interest over 180 months:

Avalanche Repayment Strategy

Now, let’s say you are also able to save an extra $100 every month, meaning you can start chipping away at those loans to pay them off early (assuming none have a pre-payment penalty). From a pure numbers perspective, the wisest thing to do would be to take that $100 and make extra principal payments in the building loan, since it has the highest interest rate. And then, once that is done, move the extra money you were paying monthly on that loan to the next highest interest one. This is called the “avalanche” method of debt repayment, and it will definitely save you the most money over time.

Here we can see Phase 1 of such a strategy, with that extra $100 per month going towards the principal every month of the loan with the highest interest (building), while making the normal monthly payments on the other two loans (car and student). You’ll end up paying off the car loan in its entirety at the scheduled time of 60 months, but during that time you will bring the building loan balance all the way down from $15,000 to $4,000.

In Phase 2, with the car loan paid off, you should now have an additional $85.83 every month that you can stack onto the building loan, while you’ll continue paying the normal monthly payment on the student loan. This will enable you to increase your monthly principal payment on the building loan from $183.33 to $269.16, which will result in the building loan being paid off in only 15 more months (75 months total), instead of the remaining 120 months. It will also leave you with a surplus balance of $37 on that loan, which is extra money you immediately roll into the student loan that month as an extra principal payment.

Subtracting that extra $37 leaves a remaining balance of $3,713 on the one remaining loan (student), and also frees up the $275 you were paying on the building loan, which enables you to increase your monthly principal payment on the student loan to $358.33 in Phase 3. With all that money rolled forward, you’ll quickly pay off the remaining student loan in just 11 months (instead of the remaining 45 months), with $229 leftover. All in all, you ended up paying off all three loans in just 86 months at a cost of just $717 ($946 in interest minus the $229 surplus), instead of paying $1,700 in total interest over 180 months—all thanks to that extra $100 towards extra monthly principal payments using the avalanche method.

Snowball Repayment Strategy

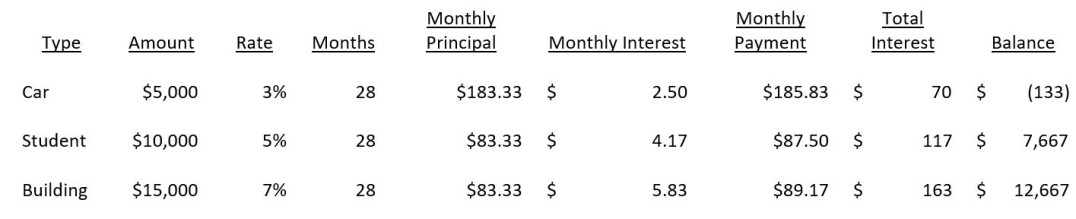

Nevertheless, Dave Ramsey recommends the “snowball” method, which, instead of paying off the highest interest loan first has you pay off the smallest loan first, simply for the psychological benefit of reducing the number of loans you have. In Phase 1, this would entail taking that $100 and putting it towards the car loan (instead of the building loan, as the avalanche method called for). Doing so will enable you to reduce the payoff time from 60 months down to just 28, and also have a surplus of $133 in the final month.

In Phase 2, with the car loan paid off, and rolling that $133 surplus into the next-smallest loan (student), you can increase your monthly principal payment to $273.33 (the $83.33 you were paying previously on the principal of the car loan, plus the $185.83 you used to pay every month toward the car loan). This will result in you paying off the student loan in 28 months (56 months total, instead of the original 120-month term), with a small surplus of $3 that can be rolled into the principal of the one remaining loan (building).

With a remaining principal balance of $10,330 and an increased monthly principal payment from $83.33 to $356.67, you’ll pay off the one remaining loan in just 29 months (85 total, which is 95 months faster than the originally scheduled 180-month loan term), and with a small surplus of $13. Collectively, the loans will have cost you $786 ($799 in interest, minus the $13 surplus), which, again, is significantly better than the normal pay-off schedule of $1,700 in total interest over 180 months. Compared to the avalanche method, the snowball method will cost you a bit more ($786 snowball vs. $717 avalanche), but you’ll actually have paid off all the loans one month faster (85 snowball vs. 86 avalanche).

Conclusion

I want to emphasize that the examples above are overly simplified, for ease of explanation, as they all are simple interest loans. In the example above, the avalanche method saved you money, but not much. In reality, most loans are compound interest, which means the savings gap between the avalanche and snowball strategies will be much greater. That said, to my own surprise, I’ve personally employed the snowball method as I did find myself agreeing with Dave Ramsey that the psychological benefits of paying off loans faster and thereby reducing the number of institutions you’re indebted to was, indeed, psychologically rewarding. But, from a pure numbers perspective, you’ll almost always be better off using the avalanche method.

(Photo by Marek Piwnicki from Pexels)