One of the more complex systems we have in finance is issuing, buying, selling, settling, and running corporate stock offerings on a public exchange. Because of how this process was created to facilitate the exchange of money for securities, the transfer of securities, and interactions with shareholders, there is a substantial amount of excess effort involved in the process that I want first to explore and then to examine what an optimized solution based on the blockchain might look like.

Let’s take a look at the process, as described in the diagram below:

- The process starts with an Issuer that makes an IPO for shares in a corporation for public sale on an exchange. The Issuer creates, registers and sells the securities to finance their operations, research & development, acquisitions or any other growth-driven activity.

One area of friction in the current system is that the Issuer does not have access to a complete list of the actual shareowners. - The stock is then placed with a Transfer Agent. The Transfer Agent acts as the registrar for all physical shares, maintains a record of share ownership, and tracks stock transfers, dividends, corporate actions and other reporting activities.

One area of friction for Transfer Agents is that they only see the registered shareholders and not necessarily the actual shareholders, usually maintained by brokerages. - Once it is listed on an exchange, the stock is available in the market to Buyers and Sellers of stocks. These could be individuals making self-directed trades or licensed institutional traders making trades on behalf of individuals, corporations or other groups.

Since the Transfer Agent doesn’t have a record of the actual shareholders, corporate actions and other shareholder communications have to be issued through various parties that either review or forward that content on behalf of the actual shareholder. - Corporate or institutional sellers making trades are usually directed by an Investment Manager who may be managing funds or other groups of assets that include stock instruments. These parties are usually disconnected from the details of portfolio but are looking to drive some aggregated growth on many investors’ behalf.

- An Investment Manager can also be a buyer in the marketplace with the same goals as the seller’s Investment Manager. We split these out to better understand that the parties in a transaction to buy or sell securities in the marketplace may be the same or different organizations.

Investment managers need to reconcile submitted orders against the notices of executed trades with brokers to confirm trade activity. - The Buyer Broker is the party that enables a group of firms or individuals to place buy orders to various exchanges.

- Buy and sell orders are placed on an exchange in order to match buyers and sellers at agreed prices.

- The Seller Broker is the party that enables a group of firms or individuals to place sell orders to various exchanges.

Buyer and Seller brokers can only reconcile internal trading positions, accounting balances and street-side versus client-side transactions across multiple trading systems and exchanges. All of these trades are usually validated via custodians. These reconciliations are usually completed on a trade +1 day at a minimum but usually may take longer depending on the level of integration and data sharing between the brokers and custodians. - Seller Custodians are financial institutions that will hold and protect a seller’s securities to limit the risk of loss or theft of stock holdings

- Central Securities Depositories are specialist organizations tasked with storing the physical stock certificates on behalf of custodians. A book of ownership is usually maintained based on confirmed trades via the custodians. Still, the depository usually only knows the broker that holds the title to the security but not the individual shareholder.

- A Buyer Custodian works in the same way as a Seller Custodian to reduce the risk of loss or theft by holding and protecting shares that are available to be transacted on an exchange.

- Custodians work the final trades through a set of representative clearing houses that facilitate the update and exchange of securities that have been executed through an exchange. The Buyer’s Clearer works with a central counterparty clearing house to complete sales with other Clearing firms.

- The central counterparty clearing house ensures that executed transactions on the markets are resolved between clearing parties on a timely basis.

- The Seller’s clearing firm is the clearinghouse on behalf of the Seller of securities to finalize the swap of ownership via the central counterparty

These clearinghouses and central counterparties are usually only aware of ownership at the brokerage level, not at the actual shareholder level. - At the end of the process, the trade is complete.

A specific problem that was heavily paper and ledger bound gets solved organically over time to deal with scale issues. There is still a legal requirement for stocks to be issued on physical paper certificates. Depositories were created to be the vaults for all of this paper and to assist with the broad tracking of ownership. You can still request the physical shares to be issued to you if you are a shareholder, but few bother to do this anymore.

This process also ignores off-exchange trading capabilities such as dark pools and grey pools. But overall the process highlights that the actual beneficial shareholder is only known to the brokers within the whole trade ecosystem. For example, If John agrees by phone to sell ten shares of stock to Steve, the actual buy and sell can hit the market and get settled, but there is no guarantee that the specific shares that had John as the beneficial shareholder are transferred explicitly to Steve. Steve will get ten shares at the agreed trade price, but nothing related to the transaction connects John and Steve.

The Blockchain Future for Securities & Commodities Trading

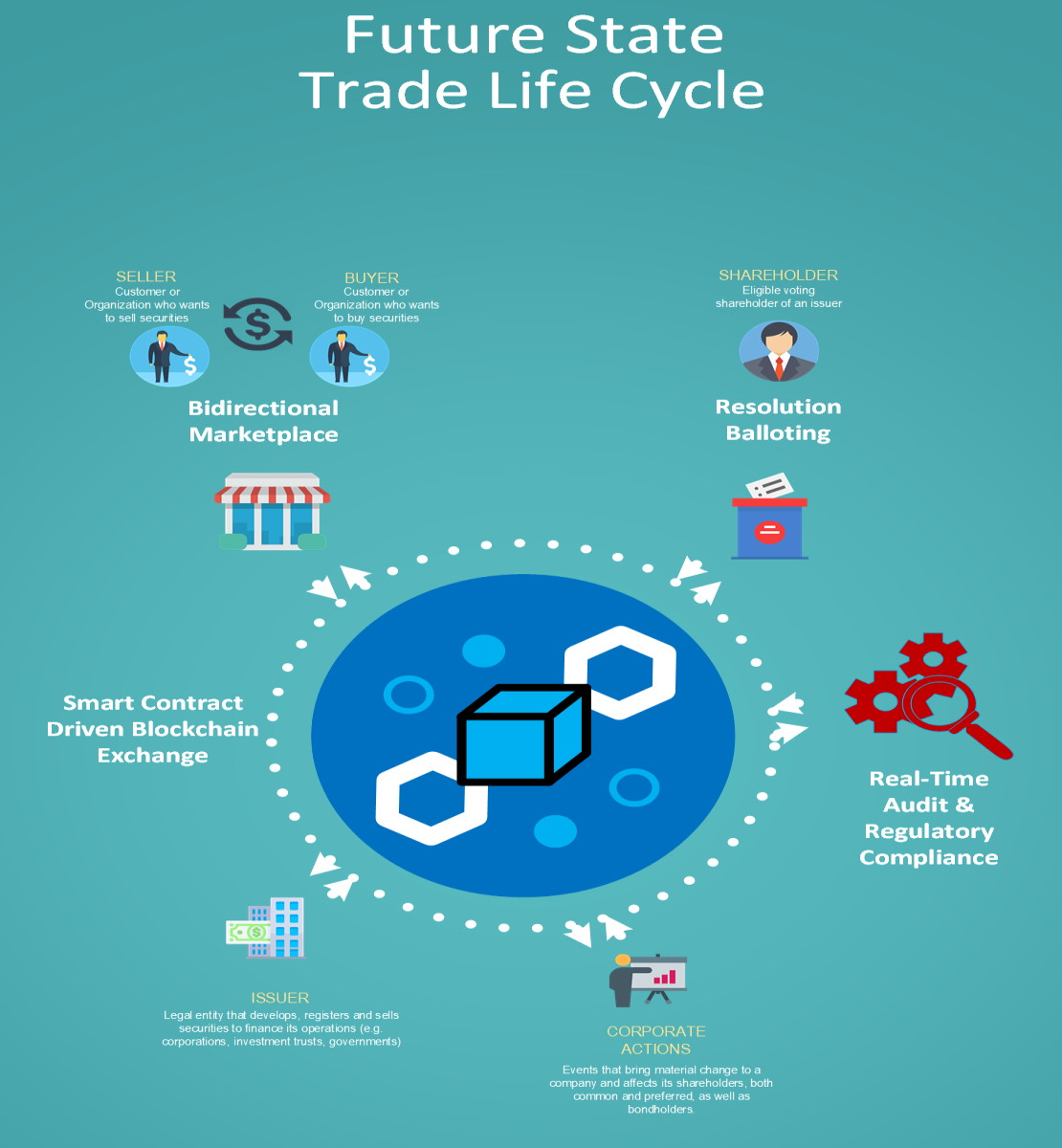

If we took a greenfield design for securities trading in a blockchain-enabled environment, the picture would be very different. In a blockchain-based solution, the beneficial shareholders are known and tracked as part of the blockchain’s securities ownership pattern. So many of the different parties that have added complexity to the current process are no longer needed. The core trading exchange holds all of the content required to facilitate buyers and sellers to make trades. Brokers could continue to be part of the marketplace community to aggregate buyers and sellers, but there is no reason that a trader couldn’t interact with the exchange directly.

Much of the friction of getting communications and ballots out to the beneficial shareholders is simplified. All of these items are generated, handled and resolved electronically through the use of smart contracts. The Issuer is directly in control of their stocks’ management and knows all of their actual shareholders.

The overall audit and regulatory visibility into the exchange activities can be centralized and reported openly in real-time. There would still need to be some regulatory hurdles, such as eliminating the requirement to publish physical share certificates, but this shows some of the significant benefits and transparency that can be brought to a specific industry through the use of blockchain.

In this model, buyers and sellers can interact directly or utilize a 3rd party broker that may offer some value-added services to transactions on the exchange. The market place can provide various shareholder and trading services to individuals who want to either run their trades on the exchange or use a managed investment approach.

An exchange would permission an approved issuer of stock to list their offering and issue shares for purchase. Issuing stock on the blockchain could operate in a similar model to how alternate cryptocurrencies are issued on a core cryptocurrency like Ethereum. After the stock is issued, the corporation could then initiate various corporate actions against their stock using smart contracts and consensus-based ballots to shareholders.

The shareholder’s portfolio would be contained in a wallet that could integrate with digital currencies to facilitate transactions between cash and stock.

The real-time audit functions will provide a series of checks and balances via smart contracts for pre-trade and post-trade compliance. The blockchain solution allows for the exchange to maintain perpetual KYC and compliance operations and alerts within the exchange to act on any irregularities that may arise. With all of the exchange's activity and operations being centralized, these automated and scaled KYC and compliance methods can monitor all activity in real-time and analyze activity over time across the exchange for irregularities.