To preface this: credit score means absolutely nothing. Sure, it means something for the average person who is wanting to buy a home eventually, but for personal finance it really comes secondary or even tertiary to cash flow in my opinion. As some of you might or might not know, I am all about personal finance and I document my journey and broadcast it for the world to see as I progress upwards in life. I have a lot of categories that I openly update weekly, and credit is one of them. As some of you know, I apply for one new credit card per year. This is mainly to lower my debt slowly while increasing my assets, but also a way for me to get better at gamifying credit ethically and legally. As a kinesthetic learner, I learn better by doing; so this this not only increases my credit available, but to also lowers my debts each year at 0% promotional rates, while increasing my assets year over year (yoy).

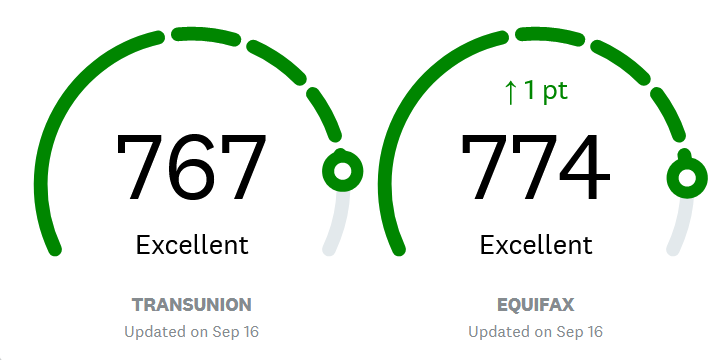

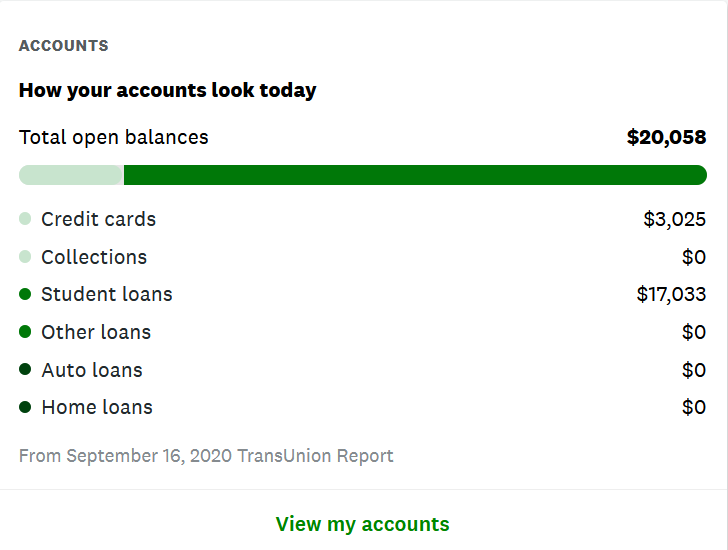

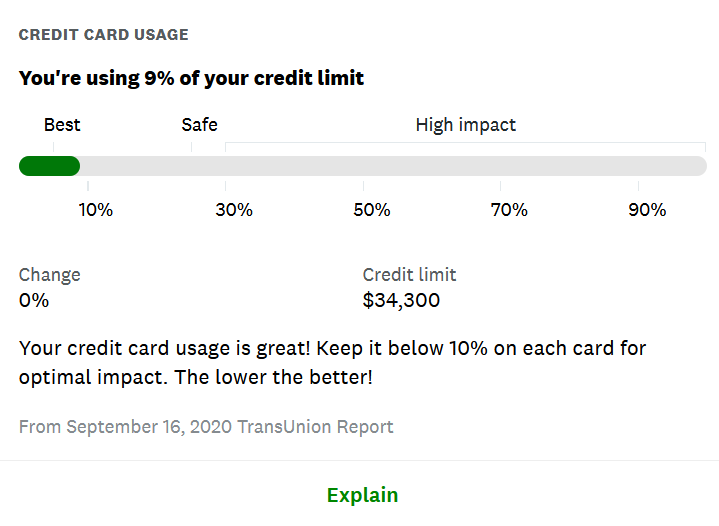

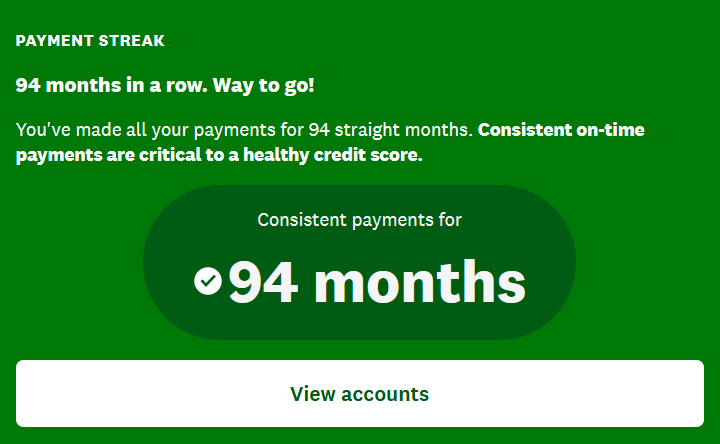

The updates in image form:

In conclusion, the credit card debt and student loans have consistently been lowering as a result of using a modified snowball version of lowering the lowest balance first and chipping away at the higher balances interest and principle before they start accumulating too high. As some of you might or might not know, because statement balances are reported based on the statement cycle of each credit type, the statement balance versus the current balance can be different. My balances on credit card debt and student loan debt have consistently been lowering. Almost like the inverse of compounding interest, my balance has been consistently being lowered over time while my assets have consistently been growing over time. You can track my journey on linktr.ee to read all of my blog and social mediums I own.