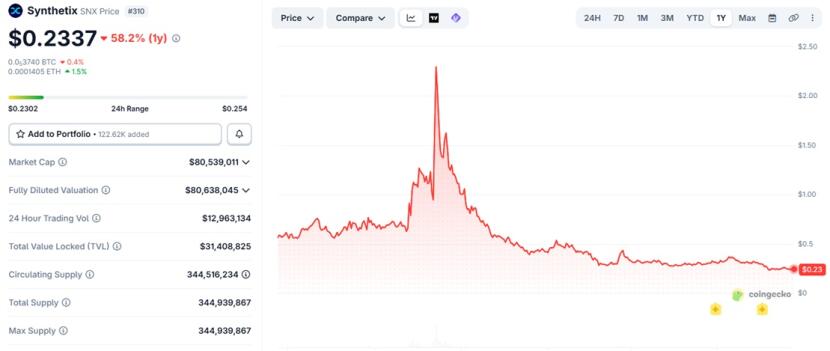

For about a year, another stablecoin has been de-pegged from the dollar, posing systemic risk to the entire ecosystem that issued it. I'm talking about SUSD and Synthetix Network. Synthetic was born as a synthetic assets system built around a simple yet powerful idea: using the SNX token as collateral to issue a synthetic stablecoin, sUSD.

The initial operation was as follows:

- Users staked SNX.

- In exchange, they could mine sUSD.

- Each staker assumed a share of the system's global debt.

- The system maintained the peg through direct economic incentives.

The key point was that if sUSD fell below $1, it became rational for stakers to buy it on the market, burn it, and reduce their debt at a discount. This arbitrage mechanism was the heart of the peg's stability. For years, this model worked relatively effectively.

EXPANSION AND DEATH SPIRAL RISK

Over time, Synthetix expanded, leading to a growth in total debt, increased system complexity, and a progressive reduction in natural demand for sUSD (which was widely used for a time in Curve Finance trading to reduce slippage).

Meanwhile, three problems emerged:

- Volatility of SNX collateral (the system depended heavily on the value of SNX).

- Increasingly difficult to manage debt.

- Insufficient actual use of sUSD.

REMOVAL OF THE OLD DEBT MECHANISM

SIP-420 removes the old debt mechanism. This reform introduces:

- Elimination of individual staker debt.

- Transition to a collective debt pool.

- Introduction of the 420 Pool as a new staking and incentive mechanism.

- Radical simplification of the system.

SIP-420 has a fundamental effect: it eliminates the main natural incentive that supported the sUSD peg. Previously, the individual staker had a direct interest in bringing sUSD back to $1. Afterward, the debt is collective, and arbitrage becomes much weaker. The 420 Pool attempts to bring stability to the protocol (on collateral), but at the expense of the stablecoin.

The 420 Pool was created as a mechanism to:

- Stabilize the SNX system.

- Incentivize staking and capital locks.

- Avoid a possible collateral collapse.

According to the founder himself, the 420 Pool likely saved the protocol from a death spiral, but at the cost of losing the sUSD peg. The implicit trade-off is that SNX survives as a protocol asset, the system avoids a collateral crisis, and sUSD loses its stability mechanism.

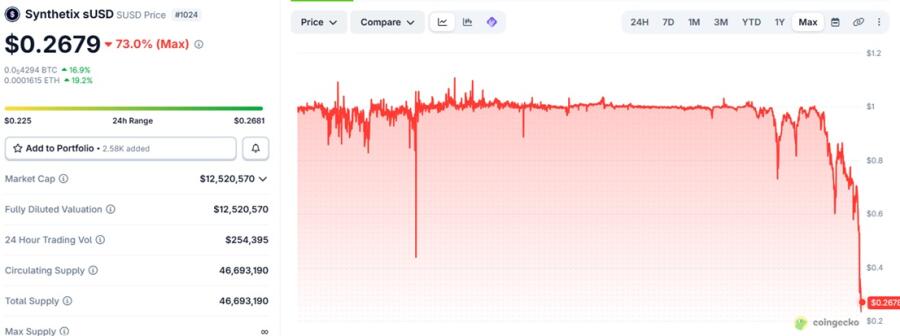

LOSS OF THE SUSD PEG

After SIP-420, sUSD begins to progressively lose its peg because arbitrage is no longer sufficient and confidence in a return to $1 weakens. The result is a persistent depeg lasting over a year.

To try to restore the peg, Synthetix tries several strategies:

1) Yield on sUSD (the idea was to make sUSD attractive to hold;

but yield generation does not materialize sustainably).

2) Treasury buyback (the protocol accumulates approximately 30% of the sUSD supply; it uses SNX to absorb selling pressure).

3) Integration with new trading, vault, and delta-neutral strategies.

The problem remains, as the protocol does not generate enough stable revenue to sustain the peg. There is no longer a natural mechanism that guarantees the conversion of sUSD to $1; the system depends on artificial incentives or treasury intervention; the cost of sustaining the peg becomes excessive.

This leads to a key diagnosis: the residual debt represented by sUSD becomes economically unsustainable.

SIP-423 AND SUSD DEPRECATED

With the SIP-423 proposal, Synthetix is making a radical decision:

- The old sUSD is being discontinued.

- Holders are being reimbursed in SNX.

- The conversion ratio is approximately 4:1 with lockup.

- The system is transitioning to a new stablecoin based on basis vaults.

According to the founder, maintaining the peg would require unsustainable buybacks, selling SNX to support sUSD would destroy the protocol's value, and the residual debt is now "functionally insolvent". After the divestment, Synthetix is evolving toward a different model:

- Focus on perpetual exchanges.

- Revenue based on trading fees.

- Future stablecoin based on basis vaults and market strategies.

- Separation between platform stability and SNX collateral.

They are incentivizing volume on their exchange by awarding weekly prizes to traders through a raffle system, based on the number of tickets collected from trading. Obviously, you don't have to buy SNX or sUSD, but simply deposit USDT on Synthetix (from Ethereum mainnet) and trade.

In this new setup: SNX is no longer the direct backstop of the stablecoin, sUSD (as we knew it) is eliminated and the system becomes more like an exchange with a “functional” internal stablecoin.

Article always updated with all the possibilities of on-chain farming (airdrop): Some Sites To Earn Crypto Bonus (Old & New)