You should know that there are different types of stablecoins: overcollateralized (Dai), algorithmic (Frax, Usdd and the failed Ust) and 1:1 collateralized by real dollars (Usdt, Usdc, Busd).

If you want to mint an over-collateralized one you need a lot of capital, for an algorithmic one you don't need capital but it is too dangerous a model in bearish phases due to the arbitrage that incorporates a token of its own ecosystem (Luna/Ust or Trx/Usdd).

This one from Curve could be something in between.

The Curve stablecoin (crvUSD) in fact uses a completely different model, being collateralized by LP tokens and functioning through the LLAMMA (Lending-Liquidating Automated Market Maker Algorithm) algorithm. Basically this model, to avoid liquidations and "bad debit", sells the collateral in stablecoins, in a linear way.

OVERCOLLATERALIZED DAI MODEL

In general, speaking of over-collateralized stables, Dai is mined by blocking a collateral (e.g. Eth). I block $100 and I can borrow for example 60% of the collateral in Dai ($60). What happens if Eth drops too much in price? The margin call starts or, in any case, other collateral needs to be blocked, to avoid liquidation (if there were no liquidation, the borrower would no longer be inclined to repay it, since they would find themselves borrowing a dollar equivalent greater than the collateral). For a protocol that has to avoid this situation, what could be the problem? If the protocol has to liquidate collateral greater than the liquidity present on-chain, this would remain so with "bad debit".

CRVUSD MODEL

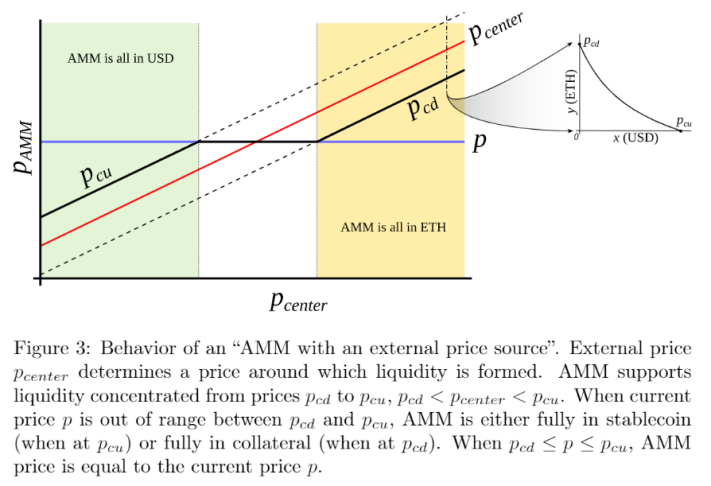

Instead, to mint crvUSD, let's assume that we are blocking Eth: if Eth drops too much in price, slowly reducing its value, it is sold in stablecoins (Usdc or Usdt). This does nothing but push the settlement price away, until it reaches infinity (it becomes difficult to be liquidated because the guarantee will always remain higher than the loan, since the extreme case, by hypothesis, is the 100% conversion of the Eth collateral into stablecoins). In reality, the collateral will be formed by an LP token (initially Eth/Usdc or Eth/Usdt). Thus, in an Eth/Usdc pool, as the price of Eth falls, the LP gradually sells Eth into Usdc. When the price goes up, the opposite happens and Usdc is sold for Eth. If ETH never dates back, the LP has enough USDC on hand to guarantee the debt.

PERMANENT LOSS?

What questions does such a model pose? Swaps between LP tokens in stablecoins would lead to a "permanent loss" (if 1 ETH=1000$ and when it is going down it is swapped in stablecoin, I get a loss therefore a progressive liquidation). In fact, the AMM is intended to operate through concentrated liquidity. This means that the liquidity itself is concentrated within a range. When the proportion of LP shifts too much to one side, the collateral will be fully converted to Eth or Usdc. This is the opposite of how AMMs normally work, where the LP holder suffers impermanent loss, getting less and less assets in appreciation and more assets in depreciation (due to the divergence of the price of the two tokens initially entered into the pool 50 and 50%). In this case the loss is temporary because if the two tokens self-balance progressively returning to the initial situation, it gradually decreases. The loss becomes permanent, only if I withdraw.

Instead, to date, through the Curve model, the loss would be permanent. This is the main problem with such a model, however if it were fixed, it would be a big upgrade. Ideally when this collateral is declining, the algorithm automatically liquidates a portion of your portfolio. If the price goes up, your guarantee is bought back. Therefore, instead of an instant liquidation, the process happens on a continuous interval (Uniswap V3?).

This strategy severely limits your potential losses and allows for passive loan management. It is somewhat as if the price of the collateral is divided into "bands". Instead of depositing at a specific settlement price, you deposit collateral over a range of settlement prices. As the price falls, the contract keeps track of which band is "active" (band in liquidation).

Liquidity is, as mentioned, divided into bands. A wider band means that your position starts to liquidate sooner, but more gradually. A smaller interval means the process can be faster. Imagine you take out a loan using 1 Eth, with a settlement range of $2000 to $2100. Your settlement bands might look like this:

X-Band ($2000 - $2020): 0.2 ETH

Y-Band ($2020 - $2040): 0.2 ETH

K-Band ($2040 - $2060): 0.2 ETH

H-Band ($2060 - $2080): 0.2 ETH

Z-Band ($2080 - $2100): 0.2 ETH

Once the price falls into the $2080 - $2100 range, your position starts to be liquidated. Your $crvUSD position is now backed by 0.8 ETH and an amount in Usdc. As the price goes down, there is an easing. In this case it is an "adiabatic process": some systems behave differently when changes occur too quickly to react. The same principle applies here: if asset prices are less volatile, liquidations are easier to avoid than sudden moves.

HOW IS THE PEG MAINTAINED?

Curve uses a PegKeeper, which is an algorithmic controller of market operations (AMO) that keeps the value of crvUSD tied to $1 through two actions:

1) If 1$crvUSD<1$USD, PegKeeper will redeem a quantity of stablecoin, burning it. This decreases supply, thereby increasing scarcity and driving the price back to the peg

2) If 1$crvUSD>1$USD, the PegKeeper standalone contract will mint uncollateralized stablecoins and deposit them into the stableswap pool. This increases supply, thereby driving the price down and regaining the peg

In a sense, crvUSD is a mix between overcollateralisation, algorithmic stable and the concept of treasuries (LPs and bonds). Do you remember which platforms used a treasury? Olympus DAO, Wonderland or mixed mechanisms such as Tomb Finance (operating through arbitrage incentives). Effectively crvUSD will be a somewhat algorithmic stablecoin with an internal AMM that creates an over-collateralized trasury that allows the peg to be maintained in volatile market conditions. The model is also relatively similar to Frax, however with some notable differences: where crvUSD mints more stablecoins to reduce their scarcity, Frax does so by eliminating Usdc. Frax also uses its treasury as its primary tool to maintain its peg, while crvUSD controls its own supply.

What are the advantages for liquidty providers (LP)? When crvUSD is minted, users are charged a variable interest rate. While the mint is not collateralized, the stablecoin itself appears to be implicitly backed by liquidity in the stablecoin pool. In general, when crvUSD is > $1, the interest rate decreases to incentivize users to borrow. This increases supply, so the price drops back to the peg. If crvUSD < $1: interest rate goes up, forcing lenders to roll back, decreasing supply and bringing it back to the peg. Will this model work? We cannot know it, yet it is very interesting. Whitepaper: crvUSD Stablecoin

Are you interested in ways to earn crypto bonus? Check it out here: Some Sites To Earn Crypto Bonus (Old & New)