You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Secondary Token and Utilities

In addition to the GMX token, the GLP token serves as the ecosystem’s LP token. Liquidity Providers (LPs) who stake the token are eligible to collect 70% of protocol fees, with the remaining 30% being converted to GLP to add to the GMX price floor contract. The GLP token is actually an index of assets used for swaps and trades on the exchange. Because of this, the GLP token lets investors earn “real yield” as the associated APR is determined by a percentage of real revenues generated by the protocol, not through deflationary tokenomics or other common strategies.

Competition and Value Proposition

There are a number of competitors, both centralized and decentralized, that compete with GMX. This includes previously mentioned CEXs, such as Binance, Kraken, and Coinbase. For decentralized derivatives platforms, GMX competes more directly with dYdX and Perpetual Protocol. In comparison, Perpetual Protocol lacks liquidity, which leads to high transaction slippage, while GMX boasts zero slippage. For traders concerned with price execution, GMX is the preferred choice.

dYdX leads GMX substantially in trading volume, but GMX has gone from being the fifth-largest perpetual DEX to dominating all DEXs—outside of dYdX—since GMX’s inception. Recently, dYdX left the Ethereum network for a Cosmos-based chain, which may not attract as many Ethereum users as GMX may by virtue of GMX being deployed on the layer 2 solution Arbitrum. This is because Arbitrum is a simple bridge away from layer 1 Ethereum, and the network even uses ETH for its transaction fees.

Both GMX and dYdX enjoy several critical elements underpinning their tokenomics. They offer liquidity mining incentives, token buybacks, and governance rights to token holders. Nevertheless, they diverge in specific aspects such as trading fee discounts, staking rewards, token burn strategies, and their approach toward the buyback-and-burn program.

A fundamental distinction between dYdX and GMX resides in their exchange models. dYdX employs an orderbook-based decentralized exchange, enabling users to establish and match buy and sell orders. On the other hand, GMX is an automated market maker (AMM)-based decentralized exchange, which capitalizes on a mathematical algorithm to ascertain prices and facilitate trades. In addition to this, dYdX extends margin trading, offering up to 10x leverage, whereas GMX provides yield farming and liquidity mining incentives for users contributing liquidity to the platform.

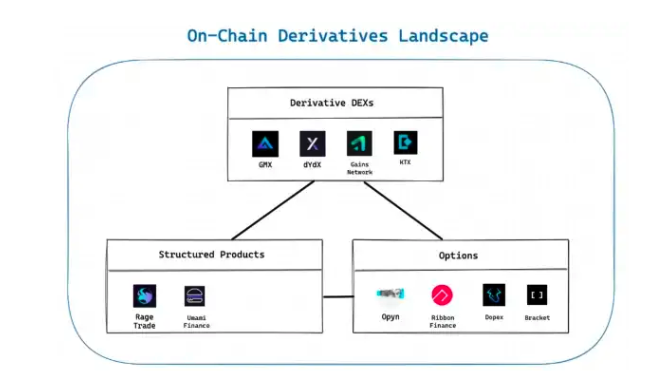

To a lesser extent, it's also worth briefly mentioning other products within the DeFi landscape that cover Structured and Options assets.

This includes Rage Trade, Ribbon Finance, and Dopex. More examples of on-chain derivatives are shown below:

GMX’s competitive advantage and value proposition stem from two interrelated factors. First off, the perpetual futures market is a magnitude larger than that of spot trading, approximately $2 trillion/month versus $200 billion/month in spot trades. There’s been a significant influx of this volume from centralized exchanges into decentralized derivatives, partially due to regulatory crackdowns and teetering user trust in centralized platforms. Following the collapse of the global FTX exchange, there was a noticeable migration of activities to on-chain exchanges.

GMX has directly benefited from this migration, which continues to boost its core value proposition of revenue sharing. Comparatively, GMX is one of the only existing exchanges (both centralized and decentralized) that pays back 100% of its revenues to GMX / GLP token stakers. As of Q2 2023, GMX is on pace to do over $1 billion in monthly volume, earning (on average) over $200k in daily collected fees (seven-day average) from protocol usage.

GMX is regularly in the top 5-10 in fees generated by a crypto protocol. Source

GMX is regularly in the top 5-10 in fees generated by a crypto protocol. Source

Combined, these factors work to create an economic flywheel that increases liquidity, margin trading volume, generated fees, and overall protocol revenues.