Overview

Formerly known as RealCoin, US Dollar Tether (USDT) was established in 2014, making it one of the oldest stablecoins. USDT is a cryptocurrency that leverages distributed ledger technology to allow individuals and organizations to store, send, and receive digital tokens pegged primarily to US dollars (USDT), but also euros (EURT), the Chinese yuan (CNHT), and gold (XAUT). Tether tokens can be quickly sent and received in peer-to-peer fashion over multiple blockchains across the globe and for a fraction of the transaction costs of many legacy payment networks.

Tether Strengths

- Liquidity and market dominance: USDT is one of the longest-running stablecoin with the most liquidity and exchange listings. It’s network effects have given it a sizable lead in the stablecoin market with nearly 80% dominance.

- Price stability and track record: USDT has a significantly longer history of (almost) perfectly holding its dollar peg, thereby earning the trust of many traders.

- Exchange listings: Tether is supported by nearly all exchanges including many of the largest and most trusted.

Tether Weaknesses

- Centralized project with unscrupulous team : Counter to the cryptocurrency ethos, USDT is completely centralized around one company and asks that its user completely trust this single-point of failure. Additionally, the company has already been exposed as lying about its “one-to-one US dollar backing.”

- Lack of transparency and audits: Tether’s minting process and auditing practices operate in a “black box” with little transparency. Tether has never produced a full audit of its reserves.

- Unclear banking relations and regulatory status: Tether Limited, over the course of its existence, has jumped from one banking partner and regulatory jurisdiction to another, raising concerns over the project’s legitimacy and legal standing.

- Counter-party risk: Tether Limited is on record as stating that holding Tethers provides no legally enforceable rights to a US dollar for the holder. Users are also reliant on Tether’s relationships with banks outside of the high standards enforced in the US.

Use Case

Tether (USDT) is a currency that represents the price of US dollars on public blockchains. It’s commonly known as a “stablecoin,” a digital currency anchored to the price of an underlying asset (Ex: US dollars, euros, yuan, gold), redeemable 1-for-1 with the underlying currency. Each USDT is an IOU issued by Tether Limited, which entitles users to dollar deposits at Deltec bank in the Bahamas.

USDT, formerly known as “RealCoin,” was released in 2014 as one of the earliest stablecoins created, and today is the most widely used. All coins are issued by associated company Tether Limited which notably has the same founders as Hong Kong-based exchange Bitfinex. It’s become blockchain-agnostic having been deployed on nine public blockchains including Algorand, EOS, Ethereum, Bitcoin (Liquid & Omni), Bitcoin Cash, Tron, OMG Network, and most recently, layer-one Ethereum competitor Solana.

USDT benefits holders as a dollar-denominated bearer asset whereby possession is described by a private key that can permit a spend without depending on a third-party. Its transactions are auditable by anyone on publicly accessible blockchains, and the price stability garnered from the price of US dollars enables traders to mitigate volatility risk in the greater cryptoasset market. Further, a dollar-peg enables USDT as a functional form of collateral in crypto-finance along with opening arbitrage opportunities where asset prices differ across exchanges.

Overall, USDT mitigates volatility risk in the overall cryptocurrency market, diversifies protocol risk among varying cryptocurrency projects, and reduces exchange risk without relying on a single exchange. Additionally, it benefits from the cryptographic assurances of assets recorded on public blockchains and held in digital wallets.

![]()

Technology

As a stablecoin, USDT inherits the benefits of being built upon crypto-native infrastructure compared to presiding within the legacy financial system. It can be sent 24/7/365, with a speedy settlement across borders directly to an individuals’, exchanges’, or merchants’ digital wallet.

Traditionally, to create a USDT, an entity must first make a US dollar deposit to Tether Limited, the company that operates the stablecoin. Per Tether Limited’s FAQs, USDT digital tokens “are 100% backed by Tether’s reserves” as can be seen on their website via a Transparency page. However, there remains uncertainty around the veracity of these claims (discussed further in the Vulnerabilities section).

Since USDT isn’t built on a particular blockchain network and rather exists as a dollar-equivalent across many platforms, it is constrained by the technology of each chain on which it transacts. It’s become blockchain-agnostic having been deployed on nine public blockchains including Algorand, EOS, Ethereum, Bitcoin (Liquid & Omni), Bitcoin Cash, Tron, OMG Network, and most recently, layer-one Ethereum competitor Solana.

This section will focus on the most popular form of USDT released on Ethereum. Ethereum enables anyone to issue assets that abide by their ERC-20 token standard which allowed for seamless integration of USDT. Ethereum utilizes a modified version of Nakamoto consensus that yields roughly 10-15 transactions per second with a block time of roughly 12 seconds. For more on Ethereum, see our core report here or our abridged version here.

In 2019, stablecoin value overtook the transfer value of ETH on Ethereum with USDT leading the way.

Overall, USDT is dependent on the assurances of the blockchain network in which it's being transacted. However, it is fault-tolerant as it exists on many different chains while also benefiting from infrastructure superior to the legacy financial system. Although USDT is centralized in a monetary policy sense, it is resilient in a technological sense.

![]()

Economics

According to USDT’s whitepaper, Tether Limited is responsible for:

- Accepting fiat deposits and issuing corresponding Tethers

- Sending fiat withdrawals and revoking corresponding Tethers

- Custodying fiat reserves that back all Tethers in circulation

- Publicly reporting Proof of Reserves and audit results

- Initiating and managing integrations with existing blockchain wallets, exchanges, and merchants

- Operating a web wallet that allows users to send, receive, store, and convert Tether conveniently

Hong Kong-based Tether Ltd. is the only entity capable of altering the supply of USDT. Given USDT is a currency intended to reflect the price of USD on public blockchains, the stablecoin is meant to be backed 1:1 by Tether Limited in reserves. In turn, Tether purports they accept fiat currency into a bank account and credit a corresponding user with new supply of USDT. Conversely, Tether Limited burns supply when users deposit USDT and redeem fiat currency to a bank account.

The value of USDT rarely trades at exactly $1 but rather fluctuates around its one-to-one reserve ratio between the token (Tether) and its associated traditional fiat assets (e.g. US dollar bank deposits). However, arbitrageurs have a financial incentive to mitigate any fluctuations by redeeming/purchasing USDT whenever economically profitable. Ultimately, the incentives for crypto entities (exchanges, funds, institutional traders) to mint or buy USDT are similar to the incentives for fiat entities to buy dollars — they’re both highly liquid.

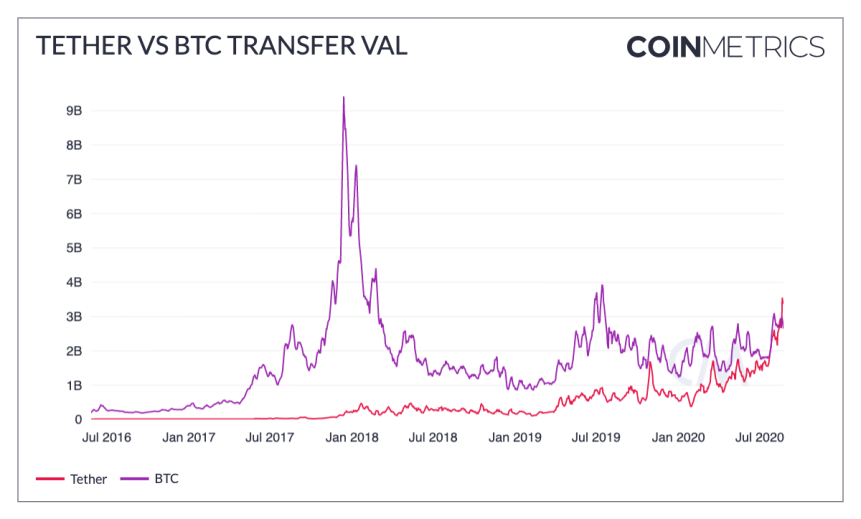

In August 2020, Tether passed a major milestone in its existence as its 7-day average adjusted transfer value finally flipped Bitcoin’s, reaching over $3.55 billion compared to Bitcoin’s $2.94 billion. This flip signaled a monumental change in the crypto-industry as Bitcoin had been the default reserve asset and base trading pair since its creation in 2009. Tether now holds that distinction and continues to take more and more of the market share of on-chain transfers.

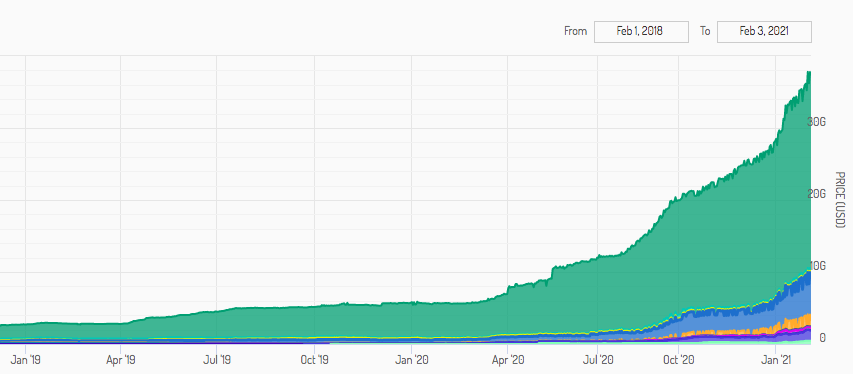

The supply figures of USDT are dynamic depending on the demand from users. For example, the free float supply of USDT (TRC20 & ERC-20) grew from around 10 million in January 2017 to over 2.8 billion in September 2018. Further, in 2020, the free float supply of USDT grew from around 3.9 billion in January to 20 billion in December 2020 . Prior to March 2020 it had taken over three years for total supply to grow to about 6 billion.

![]()

Governance

Governance is a controversial aspect of Tether as leaked documents and investigative journalists have debunked some of the company’s claims. With that said, Tether Limited is the minting agency that controls the supply and development of USDT. They claim to be fully reserved (maintain a 1:1 backing) and mint/burn USDT as real fiat dollars are deposited/withdrawn from their reserves.

In 2015, popular exchange Bitfinex enabled trading of USDT on their platform without indicating any further relationship with Tether Limited. However, the Paradise Papers leak in 2017 revealed Bitfinex operators Phillip Potter and Giancarlo Devasini were responsible for setting up Tether Holdings Limited, the parent company of Tether Limited, in the British Virgin Islands in 2014. Additionally, a later investigation proved the two firms to have a common CEO, JL (Jean-Louis) van der Velde.

Outside of the centralized issuing entity, USDT is available on many public blockchains, and as a result, protocol risk is idiosyncratic to each transport network.

Ultimately, Tether is a centralized bank-like entity where businesses and individuals undergo a KYC verification process to ostensibly deposit and redeem USDT. While users are subject to the centralization risk of this issuing entity, USDT transacted peer-to-peer or with an exchange is outside the scope of Tether’s KYC process and is subject to risks associated with the transacting counterparty and transport protocol. Given the inconsistent claims of Tether Limited and centralized control over its issuance, USDT owners must weigh these risks when deciding whether it is worth holding and transacting in USDT.

Additionally, in November 2018, the New York Attorney General issued subpoenas to Bitfinex and Tether which, as discussed above, are owned and operated by the same small group of individuals. According to the filings, Bitfinex has siphoned at least $700 million from Tether’s reserves; the Attorney general describes these transactions as “treat[ing] Tether’s cash reserves as Bitfinex’s corporate slush fund.” Given this example and the connection between these two companies, USDT’s centralization risk is clear and subject to a small group of leaders.

![]()

Vulnerabilities

The largest outstanding risks associated with Tether aren’t technological — they are rather financial, legal, security, and censorship risks.

It’s been reported Tether Limited hasn’t had consistent banking relationships throughout its lifetime. Tether is limited or restricted for use in the following areas: Cuba, North Korea, Iran, Pakistan, Syria, Venezuela, Crimea, and the US. The financial viability of Tether Limited connecting to US banking institutions is a serious and legitimate threat to USDT.

Additionally, the very idea of stablecoins or “crypto dollars” have come under attack from US regulators as the STABLE Act was proposed in December 2020. The STABLE Act was written with “the intent to prevent abuse, opacity, and the potential rise of a stablecoin-based shadow-banking system.” However, the obligations that stablecoin issuers would have to abide by in order to avoid breaking the law are incredibly cumbersome and/or restrictive.

Any stablecoin issuer would be required to obtain a federal banking charter and required to obtain the approval of both the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) six months before issuance. Additionally, the stablecoin issuers would either need to obtain FDIC insurance or deposit dollar reserves directly at the Federal Reserve.

In November 2017, roughly $31 million were stolen from Tether. Notably, as Tether Limited isn’t a US-regulated bank, users are outside the promise of FDIC-insured bank accounts that guarantee withdrawals up to a threshold of dollars. Ultimately, as a centralized entity, users must trust Tether Limited to responsibly custody deposits.

USDT hasn’t always reflected fully-backed dollar reserves or a dollar-pegged value. Despite a solvency report released to the public in 2017 which indicated a fully-backed USDT supply, a roughly 74% backing was revealed by Tether’s General Counsel in a 2019 Supreme Court hearing in New York. Also, Tether's stability mechanism to maintain a dollar peg is imperfect, as USDT was trading at a ten percent discount in 2018 across notable exchanges Kraken and Bittrex.

Lastly, Tether’s history of blacklisting addresses, freezing funds, and complying with regulatory pressures pose remarkable censorship risks. In 2020 alone, 84 addresses have been blacklisted, meaning the funds held by these wallets are completely unusable.

Overall, USDT is vulnerable to financial, legal, and security risk. Tether Limited has proven its inability to maintain a relationship with a US depository institution while also revealing its lack of regulatory compliance, protection of reserves, solvency, and ability to be honest in its transparency reports.

![]()

Network Effect

USDT has been established in the cryptocurrency industry as the undisputed leader in the realm of stablecoins. It comparatively leads in terms of market cap, volume, and exchange listings; beyond its categorical dominance, it’s the third-ranked overall cryptocurrency in terms of market cap behind only Bitcoin and Ethereum. Impressively, USDT briefly surpassed Bitcoin’s reported volume in September 2019 on a day in which USDT broke its previous all-time high. Lastly, USDT currently leads all crypto-assets in terms of “Real Volume (24H)” as calculated by Messari.

According to CoinGecko, USDT is listed on 311 exchanges and holds ~80% of the total market cap of tracked stablecoins. The most notable exchanges include Bitfinex, Binance, FTX, Uniswap (v2), and OKEx. Further, USDT’s market cap is over double the combined market caps of competing stablecoins USDC, Dai, BUSD, PAX, and sUSD. The availability and depth of USDT in both centralized and decentralized exchanges signals the stablecoin as perhaps the most liquid crypto asset. Further adding to its ubiquitous appeal, USDT has launched on nine prominent public blockchains — including Bitcoin (Omni, Liquid), Ethereum, Solana, and EOS.

Delving into the social media landscape, Tether’s official Twitter account and Subreddit have 49.5K followers and 5K members, respectively. Comparatively, these figures are dwarfed relative to both layer-one platforms of a similar market cap and popular decentralized apps. However, when analyzing its crypto asset category, USDT ranks ahead of other centralized stablecoins BUSD and TUSD while settling behind decentralized stablecoin Dai. Notably, USDT doesn’t have an available Github as it’s organized by a proprietary authority.

Ultimately, USDT has built significant liquidity in the cryptocurrency community and sits well ahead of competing stablecoins in each of the major quantifiable categories.

![]()

Team

Tether was originally founded as “RealCoin” in 2014 by Mastercoin founders Brock Pierce and Craig Sellars, along with Reeve Collins. Today, Tether’s team consists of three executives who hold the same titles at prominent exchange Bitfinex: CEO JL (Jean-Louis) van der Velde, CFO Giancarlo Devasini, and General Counsel Stuart Hoegner. Notably, the fourth executive member of Tether and former Bitfinex CSO Phillip Potter departed in 2018 during an investigation led by New York Attorney General Letitia James.

According to the Bitfinex blog, van der Velde founded many companies ranging from hardware design, software development, and investment — namely, PAG Asia, Tuxia GmbH, and Amos Ltd. Moreover, he began serving as Bitfinex CEO in 2013.

Devasini, a graduate of Milan University and originally a physician, founded Point-G-Srl, a distributor of computer parts across China, Hong Kong, and Taiwan. Upon discovering Bitcoin in 2012, he pivoted his career to join Bitfinex.

Hoegner, a former employee of Ernst & Young’s M&A group, is called to the bar in Canada and the US. He attended Carleton University and the University of Toronto and joined Bitfinex in 2014. Significantly, Hoegner admitted in a 2019 affidavit to the Supreme Court of New York that Tether Limited was 74% fractional reserve.

Specific to a project like Tether, banking relationships and compliance are extraordinarily important for the success of USDT. As mentioned previously, it’s been reported Tether Limited hasn’t had consistent banking relationships since inception. The reported timeline includes the company being founded in the British Virgin Islands through off-shore law firm Appleby in 2014, an apparent tie with four Taiwanese banks that wired transactions with Wells Fargo until 2017, and relationships with the Bahaman Deltec Bank, the Puerto Rican Noble Bank, and an associated Panamanian payment processor Crypto Capital Corp. in 2018. The financial viability of Tether Limited connecting to US banking institutions is paramount in the coming years for the project.

![]()

User Experience

Having issued tokens abiding by differing standards on differing protocols, USDT is storable across a wide variety of wallets. USDT is compatible with wallets capable of storing ERC-20, TRC20, SLP, Bitcoin (Omni-compatible), and so on. Some popular mobile, hardware, and web wallets include Exodus, MyEtherWallet, TrustWallet, Omni, and Ledger. It’s important to note when sending and receiving USDT between wallets to verify which token standard and network to which the USDT corresponds. Additionally, different block explorers (Omni Explorer, Etherscan, EOS Park, Tronscan) are tailored to viewing USDT transactions on different chains.

USDT may also be stored in a Tether account with centralized minting organization Tether Limited which requires customers to participate in a KYC verification process.

Since USDT is widely accepted and available, it can be secured and acquired in many different formats. Each form of storage from exchanges to mobile, web, and hardware wallets incur varying degrees of security risk. Exchanges are centralized custodians that store and have full control of your keys; this carries the risk of a hack, rehypothecation, or company shutdown.

The list of top-volume addresses for USDT reveals a mix of CeFi (Centralized Finance) and DeFi users. On the CeFi side, we see Binance, FTX, Paxos, Circle, Huobi, and Alameda. DeFi projects with high stablecoin volume include Aave, Compound, Curve, Harvest, Tokenlon, and Uniswap.

Overall, USDT has a wide variety of options, yet it can be confusing for new adopters given the varying types of USDT that exist on differing blockchain networks.

![]()

Regulation

There have been many regulatory orders related to Tether ranging from late 2017 through 2019 involving fraud, audits, and unlicensed money transmitting. In December 2017, the US Commodity Futures Trade Commission sent Tether, Bitfinex, and former auditor Friedman LLP a subpoena of which the requested information was undisclosed. A report was published in January of 2018 that revealed Tether’s relationship with Friedman had dissolved.

Most notably, a lawsuit filed by Attorney General Letita James in the New York Supreme Court cited fraud violations to iFinex inc., the operator of Bitfinex and Tether, in April 2019. More specifically, James' investigation determined they (Bitfinex and Tether) hid losses of $850 million of commingled client and corporate funds. Reportedly, subpoenas issued to Bitfinex and Tether in November 2018 uncovered these funds had been sent to Panamanian payment processor Crypto Capital Corp. without any written contract or assurance. According to the filings, Bitfinex had been taking millions from Tether’s reserves to hide undisclosed losses and their inability to service customer withdrawals.

As mentioned in the Vulnerabilities section, the very idea of stablecoins or “crypto dollars” have come under attack from US regulators as the STABLE Act was proposed in December 2020. The obligations that stablecoin issuers would have to abide by in order to avoid breaking the law are incredibly cumbersome and/or restrictive.

Outside of court investigations, Tether has extensive terms of service and clearly states its restrictions in Cuba, North Korea, Iran, Pakistan, Syria, Venezuela, Crimea, and the US. In addition, despite USDT representing the value of a dollar on public blockchains, it is treated by the IRS as property. Essentially, this means exchanges of stablecoins, such as USDT, should be reported as it represents a taxable event.

Ultimately, based on historically stringent regulatory activity, Tether is closely monitored by law officials. That being said, Tether has been resilient and remains the leader of stablecoins while under scrutiny in an increasingly competitive environment.

![]()

Road Map

Since launching in 2014 on Bitcoin’s Omni protocol, Tether has issued USDT on alternative blockchain networks as well as launch new stablecoins.

USDT has been represented on 9 differing blockchains: Algorand, Ethereum, EOS, Bitcoin (Omni + Liquid), Bitcoin Cash, OMG Network, Solana, and Tron. Further, Tether has released stablecoins to track many underlying currencies beyond the US dollar, including euros, the Chinese yuan, and gold.

While Tether hasn’t disclosed an official roadmap, it’s apparent leadership will continue to bridge stablecoins onto more public blockchains as well as release new stablecoins.

![]()

Disclaimer

This content is for informational purposes only and is not intended to provide tax, legal, accounting, financial, investment, or professional advice. CryptoEQ is not an investment advisor nor any sort of financial advisor. You should not construe the information provided on this website as investment advice, financial advice, or any other advice. The information contained on this website is general information, and CryptoEQ does not provide personalized information to any Users.

Investing involves substantial risk, and CryptoEQ makes no guarantee or promise as to any results that may be obtained using information from the website, either directly or indirectly. Different types of investments involve carrying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for any User’s portfolio.

CryptoEQ provides all information on its website “as is” and without warranties of any kind. CryptoEQ will strive to provide accurate information, but CryptoEQ is not responsible for any inaccurate or missing information. By accessing the information and CryptoEQ website or platform, you expressly acknowledge and accept all risks and liability associated with the use of the information provided. To the maximum extent permitted by law, CryptoEQ disclaims any and all liability in the event any information provided on the website proves to be inaccurate, incomplete or unreliable, or result in any investment or other losses.