As the starting date for cryptocurrencies, the birth of Bitcoin in 2008 is considered.

In fact, about 20 years before Bitcoin was born, Digicash was founded by David Chuam in 1989 to produce digital money.

What is the Idea Foundation of the Digicash Project?

In 1981 David Chaum published the article "Untraceable Electronic Mail, Return Addresses, and Digital Pseudonyms" in which he laid the foundations for research in the field of anonymous communications. Based on asymmetric cryptography, the method described in this paper is intended to be applied to email or elections.

During 1982, David Chaum also published a paper entitled "Blind signatures for untraceable payments" in which he formalized a concept of anonymous electronic money, a concept which would later become the theoretical basis of eCash

David Chaum focused on creating solutions to prevent governments and large technology companies from easily accessing people's private information. In a period when the global economy did not mature, cyber technology did not develop, and mobile phones were not available, it was a forward-thinking way of thinking about individual privacy.

David Chaum “The difference between a bad electronic money system and a well-developed digital currency will determine whether we will have dictatorship or a real democracy”

What is eCash?

David Chaum founded the DigiCash company in 1989 to realize the idea of the eCash payment system, which he started developing in 1981.

eCash was a peer-to-peer micro-payment system. While using the banks as a tool, eCash also aimed to be confidential and anonymous. The basic concept behind ECash was blind signatures. Blind signature is a type of digital signature in which the content of the message does not appear before signing. This way, no user can create a link between withdrawal and spending. The money used in the system was called "CyberBucks"

How eCash Works Inside

Like banknotes, eCash can be withdrawn from and deposited to transaction demand deposit accounts. And like banknotes, one person can transfer possession of a given amount of ecash to another person. But unlike cash, when a customer pays another customer an electronic bank will play an unobtrusive but essential role.

To show how it all works we'll explain how a withdrawal works, then follow the eCash in a payment to a merchant. Combining these two transactions, we can then understand why the customer perceives that ecash is paid from person to person without involving any bank. Finally the withdrawal is explained in greater detail to illustrate the 'blind signature' concept, which is the foundation of the privacy feature, and explain why the bank cannot trace it's own money!

Simple Withdrawal of eCash

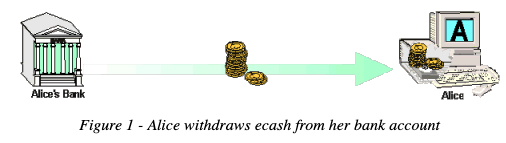

Figure 1 shows the two participants in the withdrawal transaction: the bank and customer, Alice. The digital coins that have been withdrawn from Alice's account at the bank are on their way to her PC. When they arrive, they will be stored along with some coins she already has on her hard disk.

No physical coins are involved in the actual system of course, but the messages include strings of digits, and each string corresponds to a different digital coin. Each coin has a denomination, or value, so that a purse of digital coins is managed automatically by Alice's ecash software. It decides which denominations to withdraw and which to spend in particular payments. (The ecash software keeps plenty of 'small change', but will prompt the user to contact the bank in the rare event that more change is needed before the next payment, to restructure its purse of coin denominations.)

An eCash Purchase

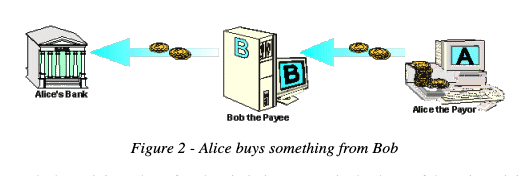

Now that Alice has some eCash on her hard drive, she can buy things from Bob's shop (as shown below).

Having received a payment request from Bob, she agrees by ticking the 'Yes' box. Her eCash software chooses coins with the desired total value from the purse on her hard disk. Then it removes these coins and sends them over the network to Bob's shop. When it receives the coins, Bob's software automatically sends them on to the bank and waits for acceptance before sending the goods to Alice along with a receipt.

To ensure that each coin is used only once, the bank records the serial number of each coin in its spent coin database. If the coin serial number is already recorded, the bank has detected someone trying to spend the coin more than once and informs Bob that it is a worthless copy. If, as will be the usual case, no such serial number has been recorded, the bank stores it at that position and informs Bob that the coin is valid and the deposit is accepted.

Person-to-Person Cash

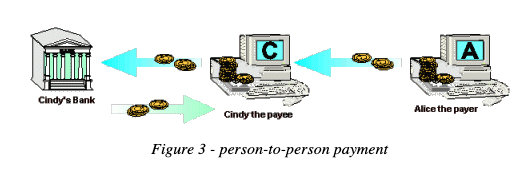

When a consumer receives a payment, the process could be the same. But some people may prefer that when they receive money, it be made available on their hard disk immediately, ready for spending; just like when someone hands them a five dollar bill. This user preference can be realized as depicted in Figure 3.

The only difference between this payment from Alice to another consumer, Cindy, and the one Alice paid to Bob's shop in Figure 2, is what happens after the bank accepts the cash. In Figure 3, Cindy has configured her software to request the bank to withdraw the eCash she has just deposited and send it back to her PC as soon as the coins are accepted. (Actually Cindy's bank will check with Alice's bank to make sure that the coins deposited are good.) Now when Alice sends Cindy five dollars, new coins are immediately available to spend from Cindy's PC.

How Privacy Is Protected

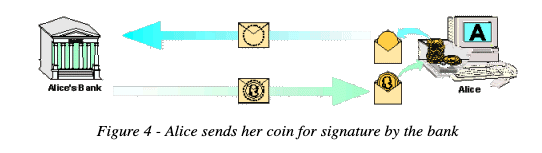

In the simple withdrawal of Figure 1, the bank created unique blank digital coins, validated them with its special digital stamp, and supplied them to Alice. This would normally allow the bank (at least in principle) to recognize the particular coins when they are later accepted in a payment. And this would tell the bank exactly which payments were made by Alice.

By using 'blind signatures, a feature unique to ecash, the bank can be prevented from recognizing the coins as having come from a particular account. The idea is shown in Figure 4. Instead of the bank creating a blank coin, Alice's computer creates the coin itself at random. Then it hides the coin in a special digital envelope and sends it off to the bank. The bank withdraws one dollar from Alice's account and makes its special 'worth-one-dollar' digital validation like an embossed stamp on the envelope before returning it to Alice's computer.

Like an emboss, the blind signature mechanism lets the validating signature be applied through the envelope. When Alice's computer removes the envelope, it has obtained a coin of its own choice, validated by the bank's stamp. When she spends the coin, the bank must honor it and accept it as a valid payment because of the stamp. But because the bank is unable to recognize the coin, since it was hidden in the envelope when it was stamped, the bank cannot tell who made the payment. The bank which signed can verify that it made the signature, but it cannot link it back to a particular object or owner.

Digicash Partnerships

DigiCash was founded in the 1990s when internet companies began to find new life. The company has signed agreements with several banks that aim to use the platform in a few years. These banks included Deutsche Bank (DB), Credit Suisse (CS) and other banks around the world. Microsoft was also interested in eCash for Windows 95, but the two companies failed to accept an agreement.

One of the most promising (and yet ultimately disappointing) potential partnerships was with Citibank. The bank engaged in long-term negotiations with DigiCash about the possibility of integrating, only to ultimately shift toward other projects.

Digicash's Bankruptcy

The banks that decided to implement eCash started testing the platform but never sold it as a viable product to its customers. The only bank that actually used the platform was Mark Twain Bank in St. Louis, Missouri.

After the ongoing partnership talks between Microsoft and eCash remained endless, disagreements arose between the project team and David Chaum. In 1994, David Chaum left the company.

In 1997, Nicholas Negroponte became president. After a three-year trial signing only 5,000 customers, the system failed to make progress. The banks that decided to implement eCash started testing the platform but never sold it as a viable product to its customers.

DigiCash eventually filed for bankruptcy in 1998. İts assets to eCash Technologies, another digital currency company, which was acquired by InfoSpace on Feb. 19, 2002.

Why did eCash fail?

- When ECash was launched, the internet was still in its infancy and there were no blockchain apps.

- To use ECash, you had to have an account at Digicash's contract bank. Also, the number of cooperating banks and financial institutions was not enough to keep eCash alive.

- In the 1990s, individual privacy was not as important as it is today.

- People were not sufficiently knowledgeable about the possibilities offered by new technologies and did not have the courage to use eCash.

- Disagreements within the team of the project

David Chaum “What prevented the success of the Digicash project? It was difficult to find a trader to accept privacy, so it was difficult to find users ... or vice versa. "

Why was eCash important?

- eCash provided a major innovation in financial transactions with privacy-oriented blind signatures technology

- The eCash project was the first serious project aimed at creating a privacy-focused anonymous electronic network.

- eCash has proved that cryptocurrencies can be used in the electronic trading network

- eCash has led to the idea that it will be possible to adapt the importance of protecting individual privacy against governments and large financial institutions to commercial transactions.

Purpose of the Article

ECash may seem like a failed project. In this article, I wanted to explain the importance of the eCash project, the first pioneer of cryptocurrency usage. Thank you for reading.

My Other Articles :

https://www.publish0x.com/crypto-world3/is-bitcoin-the-21st-century-tulip-mania-xwxqke

My Publish0x Reference link: https://www.publish0x.com?a=myerlrbbob