CredEarn is another service in the world of crypto finance. It operates in the same market as Nexo, which I have reviewed over here.

I ended up using CredEarn for a couple of reasons:

- Diversify the portfolio across multiple vendors should the worst case scenario happens. A bankruptcy most likely would wipe my deposits, so it all goes back to the old don't keep all the eggs in the same basked. They are also not protected via a protection scheme like the savings in my bank accounts. While they claim that they are also backed by insurance, I don't take everything at face value. The risk management is key.

- Convenience. CredEarn provide their services through a series of partners. That list of partners include Uphold who happen to be the custodians for the BAT earnings from the Brave Rewards programme which is available by merely using Brave Browser and enable the rewards. Essentially, the Uphold cards are available on CredEarn as source for the deposits, and they are used as destination for the earnings. So, I may as well earn on the side while HODL-ing my BAT.

How does it work?

The deposits made on their platform are your assets lent to CredEarn. Then, they use your assets to lend to their customers on their crypto-backed loans. It is a fairly low risk business as their borrowers must post a collateral which is greater than the value of the loan and they must maintain a certain maximum LTV (load to value) percentage to maintain the loan, therefore shielding themselves from the volatility of the crypto markets.

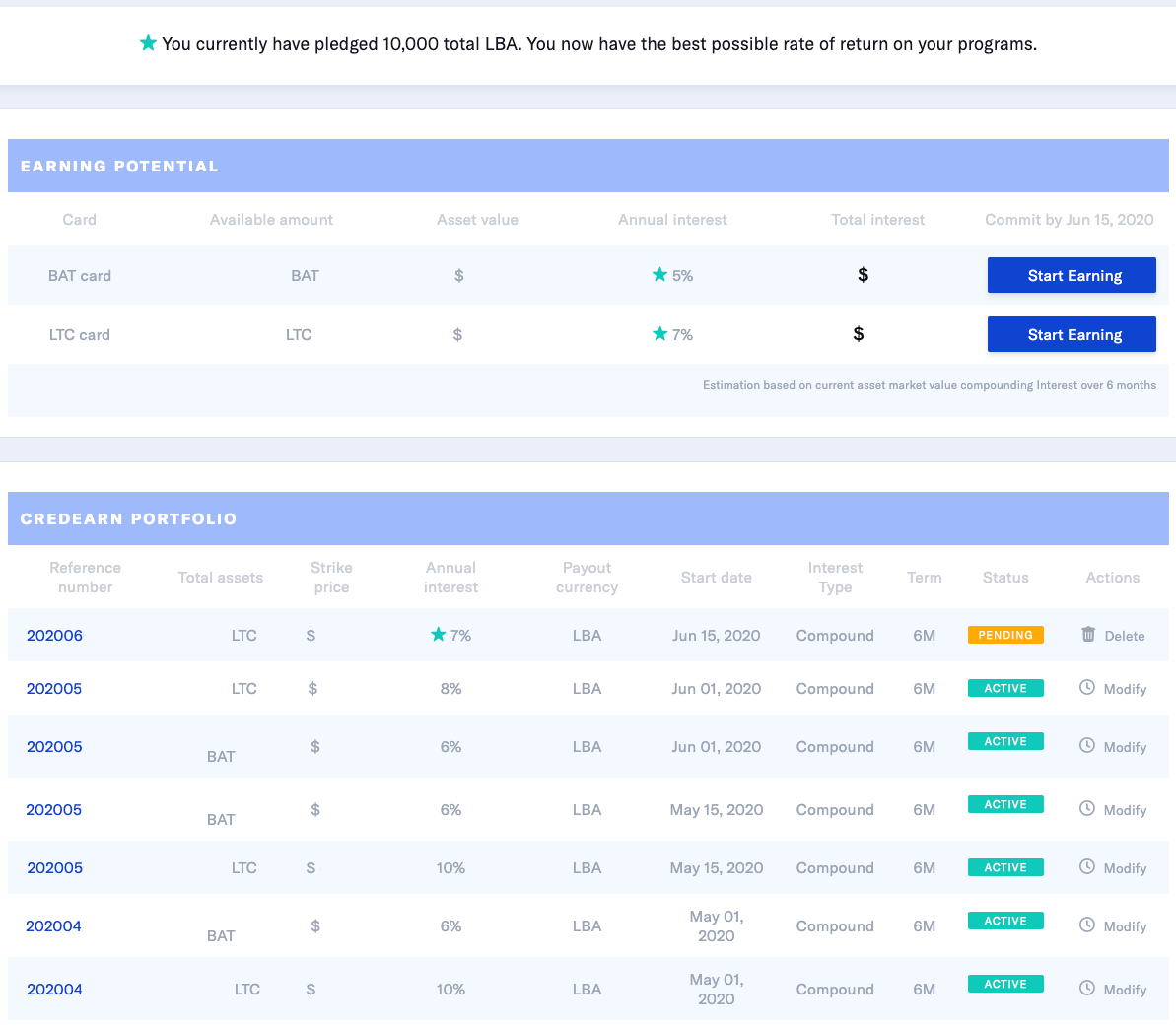

They are also offering two sets of interest rates. To access the higher interest rates, you would need to pledge 10000 LBA. This is their own crypto token. LBA is a token operating on the Ethereum network. It can be traded on its own, or used for specific services on CredEarn. 10000 may sound like a lot, but at the current value against fiat, is around $120 / £97. Unfortunately, the pledged LBA can't be used for earning interest, only for accessing their higher interest rates.

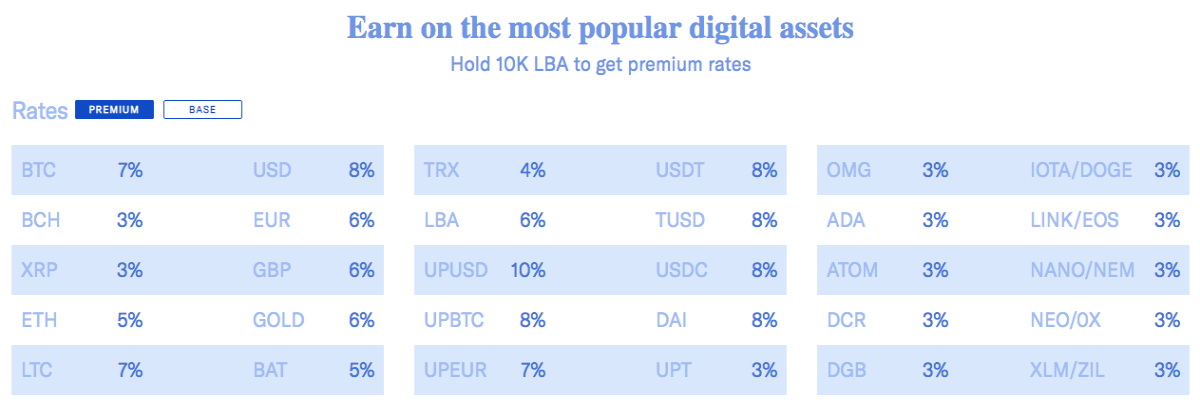

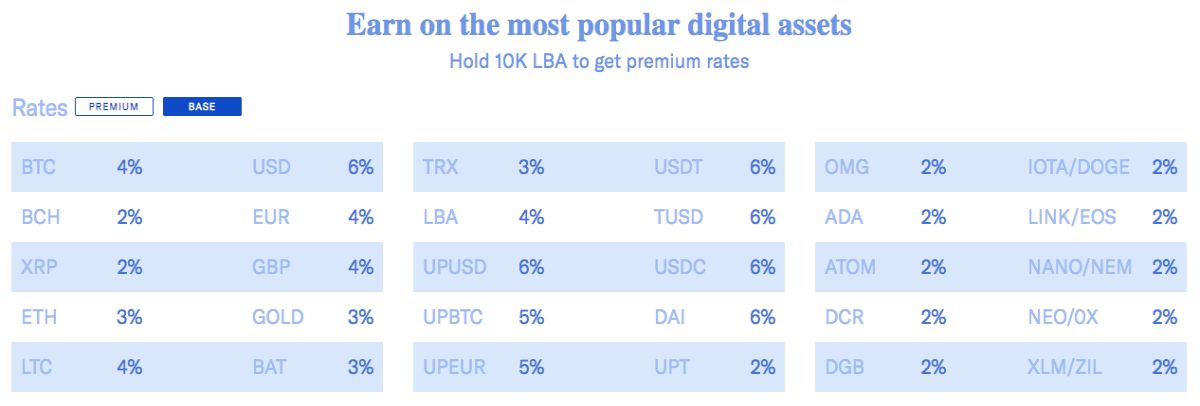

So, the interest rates are as follows.

For premium rates with pledged 10000 LBA:

The basic rates with no LBA pledge:

As you can see, at the moment, that up to 10% is for just a single asset. There used to be more, but as the current bull run of the crypto markets continues, the interest rates have been dropping lately. However, the selection is quite broad and it even includes USD, EUR, and GBP as fiat rather than being converted into a stablecoin pegged to their value. Depending on jurisdiction, this distinction is important as the earnings may have different tax classification which may be used for maximising the different income allowances you may have.

About deposits

The deposits are fairly inflexible. This is quite the opposite of Nexo. However, they do support quite a few asset classes. The minimum duration is 6 months with an automatic extension to 9 months, unless you opt-out from the auto extension. Essentially, they operate as savings bonds with a twist.

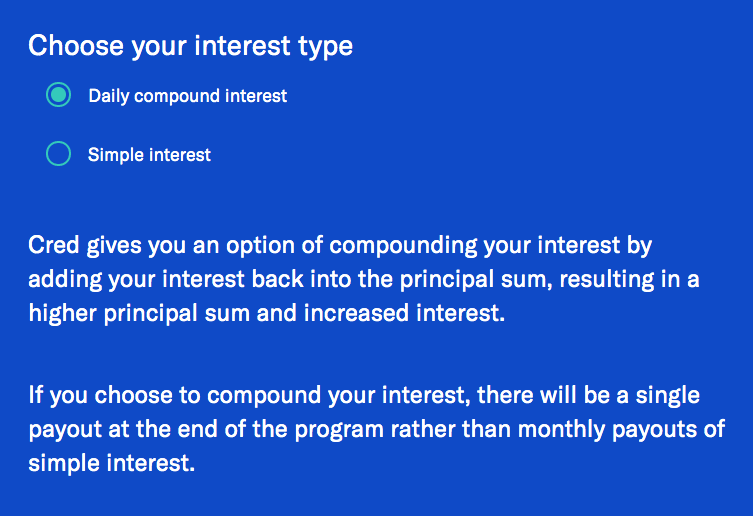

The twist is that they offer simple interest and the simple interest is paid monthly, unlike the compound interest. In their own words:

You can open a deposit at any time, but they are only executed twice per month - on the 1st and on the 15th of the month. While they are in pending state, the assets remain in Uphold's custody, so you must have enough liquidity to fund the deposit when it is executed.

I have discovered one particular advantage of opening early a pending deposit: if they decide to reduce the interest rate, you will keep the original interest rate you originally subscribed to. If they decide to increase the rate, you can always cancel the deposit before the execution date and resubscribe. I have not seen the interest rates going up in practice, therefore I have not tried this technique.

CredEarn also have the concept of strike price i.e they calculate the US dollar value of your deposit at the date of execution and the interest payout is based on that value. The good news is that the payout is predictable in terms of fiat. That may not be beneficial: if the value of the underlying asset is increasing in the mean time, you would be earning less in interest. The opposite is also true: if the value of the asset is decreasing, the interest is earned based on the original strike price.

The payout is either done in USD or LBA. For the time being, I am using it to build a position in LBA. Afterwards, even LBA itself may be used at a future date for a deposit, to further compound the earnings.

The consequence of the strike price concept and USD or LBA payout is that even the deposits in EUR or GBP may only be used to build a position in USD or LBA.

Any words about the strategy?

Some form of strategy is required due to the inflexibility of the deposits which are locked for 6 months. I am using the cost averaging, so I drip feed the deposits every 2 weeks as I am expecting the value of the underlying assets to increase, so locking the assets at a strike price close to the current value would yield less in 6 months time. That's dividing the initial value of the stash by 12 and add a deposit every 2 weeks, each slice at a time. I have not discovered any limit for the number of active deposits. Also, the BAT stash is increasing every month, therefore, the BAT deposits are slowly increasing in size as well.

I am also using compound interest as it gives a greater yield for the same period of time. Sure, a monthly USD payout would be useful to build up a position in crypto, but that usually comes at a steep 1.95% fee on Uphold which is their typical conversion fee. Therefore, I try to limit the conversions as much as possible as 1.95% per transaction adds up quickly.

I can't tell just yet how successful this strategy may be. For my LTC deposits, they have reduced the interest, twice, and for the BAT deposits, once. The potential for greater returns has been eroded by the lower interest rates. The other thing I can't tell is whether the LBA payout goes through a conversion or it is paid straight as LBA to the destination LBA card on Uphold. This distinction is important. If they send USD to Uphold and leverage Uphold to the conversion, that attracts the 1.95% fee. Time will tell.

This article is not investment advice. Should you need it, please hire the services of an independent financial advisor.

This article contains referral links should you wish to support the author.