If you have wandered or perhaps fallen down the crypto rabbit hole, you might find yourself trapped in the echo chamber of sentiments such as the imminent collapse of the fiat system, the downfall of the US dollar as a world reserve currency and the incessant money printing of the Fed that drives us ever closer to hyperinflationary armageddon. The typical fear and greed package.

But have you ever asked yourself:

- What is money?

- How is it printed?

Grab your reading glasses, and prepare to get loopy.

Formal definitions of money

Let's quickly skip through some formal definitions of what money is. We can add to this as we go deeper.

The common idea is that in a world sans money, if we wanted to exchange goods and services, we would have to barter with our goods. It would be difficult for us to agree upon fair value, or rather this idea would vary from trade to trade and person to person. Right now it may seem like a good idea to trade in eggs and other commodities whose values seem to be going to the moon, but this is obviously mostly impractical for a variety of reasons.

The idea of barter as the oldest method of settling transactions is, however, a misconception (the first of many). Michael Every explains that the anthropology of money (from Polyani or David Graeber's, Debt the First 500 Years), shows that debt came before barter. Barter is highly inefficient, more so at a global scale, where sole reliance on it would result in the freezing of supply chains.

To quote Investopedia:

Money is "any item or medium of exchange accepted by people for the payment of goods and services and the repayment of loans."

They add that:

- As with Gold and Silver, money has worth because (for most people) it represents something valuable.

- Government-issued Fiat money is backed by the stability of the issuing government, rather than by physical commodities.

- Money's main role is as a unit of account, a socially accepted standard against which things can be valued.

Many in crypto say that Fiat is not backed by anything; by the above definition they are dismissing the value of the stability offered by their governments, the stability many of us (including the doomsayers) enjoy is not something to be lightly dismissed.

The dollar is not money

Monetary Metals (as usual) get more granular on this, stating that money has four specific and textbook functions; medium, measure, standard and store. It must be noted that as Gold advocates, the context of their statements is usually to paint Gold as a functional form of money; not without reason.

Medium - as above, a medium of exchange used to pay for goods and services.

Measure - a way of measuring economic value, a unit of account. You are getting 1% cashback from your credit card purchases. You get paid $100 on your $10,000 worth of purchases per year. The additional money received only has meaning if money can accurately and consistently represent value.

Standard - in their interpretation, this is the standard of financing productive enterprise, and the monetary standard also has the ability to extinguish the debt created by the financing loans.

Store - a long-term store of value. Lock it away till the next halving and sound money should still have the same value.

Investanswers adds a fifth caveat to this; a reserve currency also needs to be a scalable means of payment. This is a consideration of the digital era, cryptocurrencies can easily deal with cross-border payments; borders are irrelevant as long as you have an internet connection, a wallet, and some money for gas fees. But scalability in the sense of transactions per second is a problem crypto is still grappling with, optimistic and zero-knowledge proof-based rollups may offer a solution. Fiat currency is a global digital payments network for double-entry bookkeeping, more on this below.

To this end, Keith Weiner of Monetary Metals has said that the dollar is not money. He thinks a more fitting description for money would be the most marketable commodity, that which is the most liquid, most widely available and with the tightest spread (in this case referring to the bid-ask spread). Many would consider Gold to be the best fit for this description. He goes into detail on this in two separate episodes linked here (part 1, part 2) and in the resources, if you prefer reading this is a link to the transcript.

Money or currency?

I keep drawing comparisons between Gold and Silver advocates and Bitcoin and Ether advocates, they both discuss the same topics (and come to similar conclusions). Anyway, here's another Gold fiend with a lot of conspiracies about the decline of the US dollar.

Mike Maloney, author of 'Gold and Silver,' states that the primary function of money is as a store of value. As he points out, even the Federal Reserve website agrees! Properties or functions such as medium of exchange, a unit of account, fungible and divisible are also listed.

Following on from this, due to inflation, Fiat currencies don't fit this definition, they are currency, not money. They do have all of the other qualities of money, but they do not retain purchasing power over time. They are not designed to.

In the featured Wealthion podcast episode, the host cites Confucius, "The beginning of wisdom is to call things by their proper name."

Throw away your textbook

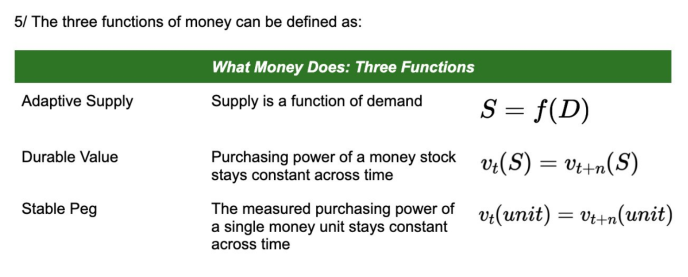

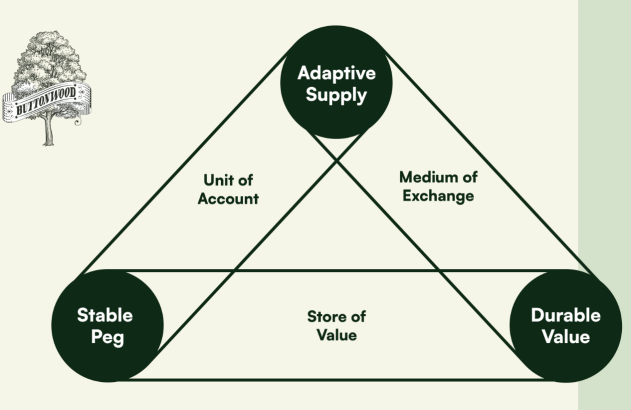

Buttonwood, a defi bond market protocol use a different approach (see Manny @mrinconcruz on Twitter), they reason that money does not have to satisfy all of these criteria at once.

They begin their argument by stating that the three primary functions of money are as a unit of account, store of value and medium of exchange. Similarly to the layer-1 trilemma, they offer a trilemma of these three vertices, stating that all versions of money target all three, eventually realize they cannot reliably deliver all of these functions, and settle for their 'most robust two-function configuration.'

In their words, "rather than debating what money is (or should be i.e. gold bugs), the trilemma focuses on what money does," and what it historically has been. I tend to favor pragmatic perspectives.

They list the three functions of money as follows:

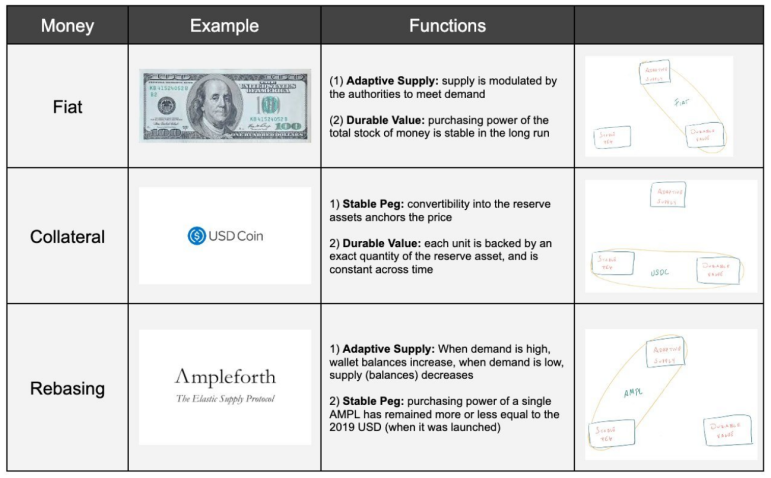

Some 46% of Fiat currencies attempt to retain a stable peg through a 'managed float,' (a.k.a. dirty float), where their central banks control the price within a certain range. While still common, these systems have seen dramatic breakdowns when central banks ran out of reserves (e.g. Mexico 1994, Asia 1997 crisis). Fiat currencies tend to have floating pegs as stable pegs are costly to manage.

The Gold-backed Bretton Woods dollar, where the price of the underlying Gold was fixed at a certain amount (US$35 per Troy ounce), was vulnerable to mass redemption for the underlying, hard-value asset.

Collateralized money has attempted to conjure elasticity, making supply more responsive to demand (ideally without excessive inflation or deflation), through fractional reserve banking. However as we are seeing today, these systems are vulnerable to bank runs (mass redemption) when trust in the system wanes. Also under this system (discussed below), the expansion and contraction of the money supply are difficult to control and can cascade in either direction. True collateralized money (such as USDC, wBTC) can only be minted or redeemed based on the assets in reserve.

Below the two-function combinations of fiat, collateral and rebasing money types are shown.

Buttonwood summarises the trilemma as a compromise between these three vertices and the consequent properties each combination enables.

Plans for their own stablecoin (which may or may not be SPOT), involve taking a rebasing asset or group of rebasing assets and using them as reserves for collateral-type money. This combination would make it a store of value. With reference to the previous section, I have used the terms money and currency interchangeably. With the store-of-value property, the Buttonwood concoction would be considered money.

To add to this idea, Australian economist and author Steve Keen notes that the store of value aspect of money contradicts the other two textbook properties, unit of account and means of exchange. If prices fall, the value of money rises, encouraging you to save. If money depreciates slightly over time, this (theoretically) encourages spending and hence under this model, the intended purpose of inflation is to stimulate demand. The takeaway is that it has historically been difficult for a form of money to satisfy all three major properties at once.

The property that cannot be ignored

In a short piece in Forbes, Keith Weiner (I have referenced him a lot) describes the decline of relative US wages (in terms of Gold) despite advancements in productivity. People work longer for less money, and neither skilled nor unskilled workers seem to be benefitting from the technology that should ultimately be making it possible to produce more for and with less. The store-of-value aspect of true money cannot be ignored.

Gold bugs want money to be a long-term store of value alongside all of the intended properties, and dismiss crypto. Most crypto bugs (there must be a better term) consider Gold to be an archaic, boomer fetish. Many would agree that Gold, while having a narrow bid-ask spread, would not be easy to use as money for the exchange of goods and services (not that I have tried), Silver, being much cheaper by weight, could be better for payments (again what do I know, I have never owned Silver). It is also inconvenient for the average person to verify the purity of Gold. Payment solutions such as Glint can offer an elegant solution for the use of Gold as both a store of value and for electronic transactions on any scale. Crypto could satisfy all edges of the abovementioned trilemma and overcome the custody issues of Gold, (which essentially becomes digital with respect to the owner when held in the custody of a third-party storage solution) while offering clear partitions between the seemingly inevitable equilibrium two-function combinations of money. However, it may not be accepted as a store of value in the near future without the backing of a physical commodity or in the long term without a good track record of consistent purchasing power.

Beyond barter, this author believes both Gold and crypto could be capable of issuing functional forms of debt. For more on this see this short piece on Gold bonds, I will elaborate on crypto-based debt in the conclusion.

Misconceptions of a trust-based system

Many have stated that Fiat systems are based on trust and backed by nothing (I stated this in an earlier article), however, Mike Maloney points out that they are really backed by your future taxation or future house, car, or other loan repayments. The collateral for the loan is your house etc., the bank providing the loan imagines however much money you need into existence, and while you may live in it, the house is theirs until you make the final payment.

Another way to look at fiat money is a devaluing promise to pay you back in full. (His videos can be quite morbid, playing heavily on the fear factor.)

Under the gold-based monetary system, the amount of work required to prospect and find a claim, build a mine, mine the ore, refine the ore, turn the refined ore into bars, melt those bars and mint coins was (roughly) equal to the work you would have to do to earn those coins, which would also equal the amount of work it would take to create the materials needed to build the house - and build the house. Some would consider this to be a fair trade-off, or at least (as Mike puts it) something, for something. If this sounds familiar to you, I was also reminded of one of our favourite consensus mechanisms.

Whereas fiat currency involves trading nothing, for something, which Mike points out is fraud. Digits are invented as reminders to pay IOUs. When they do this, it dilutes the IOU supply, the M2 money supply, thereby stealing purchasing power from all the existing units of currency.

So maybe next time someone presents you with an irrational argument about how Bitcoin has no value, perhaps you could begin your rebuttal by reminding them of the extent to which money has been merely numbers on a balance sheet for quite some time (I will mention an estimate for exactly how long in a future article about Eurodollars).

In short, Gresham's Law states that bad money drives out good money, within the context of history, this process has happened numerous times, with repetitive results. The Mike Maloney Youtube rabbit hole is pretty long - episodes 1 and 4 of his series are enough to get a good idea. The whole series is a bit overwhelming but features some history lessons and insights from different perspectives. Note the age of his videos, he has been predicting a US Dollar collapse for nearly a decade.

Unfortunately, Mike has simplified much of the detail of how money works in our modern banking system. I will explain, but first, a detour.

U-turn - money from a social perspective

In a social sense, while we consider individual units of currencies such as dollars to be fungible, there are many social partitions that result in a sense of non-fungibility. As Viviana Zelizer says, 'as we transition to the digital era, at stake is not just the quantity of money but also the quality.'

To quote the article directly:

"If all money is the same, why do we call some dollars “dirty” — or even “blood money” — and others “honest”? Why is the money we earn as a salary often spent differently from a lottery winning? Why did we invent gift certificates rather than offer straight cash? Why do organizations construct elaborate compensation systems marking differences between salaries, bonuses, and perks?"

To ignore these social partitions is to ignore the way money is actually used, 'the fantasy of amoral, fungible money.'

Within the soup of these social partitions, it seems money and credit become interchangeable. The method of delivering the value seems to be of some importance.

These invisible partitions differ between cultures and can be subjective down to the individual. Using multiple currencies, not just different fiat, but different digital currencies allocated for different purposes may help to breach, clarify and/or specify some of these social partitions. If it is deemed necessary then this is a realistic possibility with digital/cryptocurrencies. (E.g. Islamic Coin.)

Using this idea, we could also think more about what we socially and culturally want and need money to be.

For example, imagine instead of the dystopian social credit systems being suggested, we had a social tipping currency. Instead of a single arbitrary number used to summarize your behaviour, you would have metrics related to how you use the currency. How much of it you have purchased for tipping, who you tip, how much you tip, and vice versa the way people have tipped you. Instead of a blanket social credit system intended to incentivize good behaviour from the perspective of a central planner, we would have social metrics that could be interpreted subjectively, but also objectively alert people to antisocial behaviour and malpractice as well as impart a level of trust between strangers by signifying elements of your social presence.

This could create further partitions, the high and mighty hefty tippers would want to spend more time with their own kind, likewise the thrifty may band together, and the cunning may find ways to game the system - as they always do.

But perhaps it would open up lines of communication and break down perceived social barriers, helping us all to realize we are much more similar than we think.

Let's get serious

Just as I began to think about posting a Twitter thread on money and money printing, Alf from Blockworks Macro beats me to it (here's a link to his Twitter thread). As Keith Weiner pointed out, the following perspective is not controversial, rather these are the textbook considerations of what money is, albeit a textbook that was slightly rewritten after the 2008 financial crisis.

Financial jargon incoming - you have been warned - I will try to explain this as clearly as possible. Luckily I'm a degen, not a financier so I am also foreign to most of the jargon. When learning a new topic it can be useful to hear the same thing explained from multiple perspectives, doing so creates more anchor points from which you can build your understanding.

Assets vs Liabilities - how the banking sector defines money

The next section will be easier to understand with some definitions.

What are assets and liabilities?

Assets - a claim on someone else.

Liabilities - a claim someone else has on you.

The gap between the two is equity, another definition for which would be, the amount of money that would be paid to a shareholder if all of a company's (in this case the bank's) assets were liquidated and all of their debt paid off, in the case of liquidation. In the case of acquisition, the value of company sales minus the value of any liabilities owed by the company that are not transferred with the sale of the company. Recently you might have seen banks such as Credit Suisse undergo acquisition as their shares plummeted.

The basic equation tying these together is:

Assets - liabilities - equity = 0

OR

Assets = liabilities + equity

This probably looks a lot like accounting, it is. The banking system operates using double-entry bookkeeping.

The key concept is that (queue another definition of money) money is the liabilities of the banking sector, a creature of accounting and not a commodity.

Money is a claim on someone else (or something else). I will develop this idea more in the section on money creation, but these are the basics.

Watch this Lex Fridman episode with Steve Keen to hear his explanation.

Money in the modern banking system

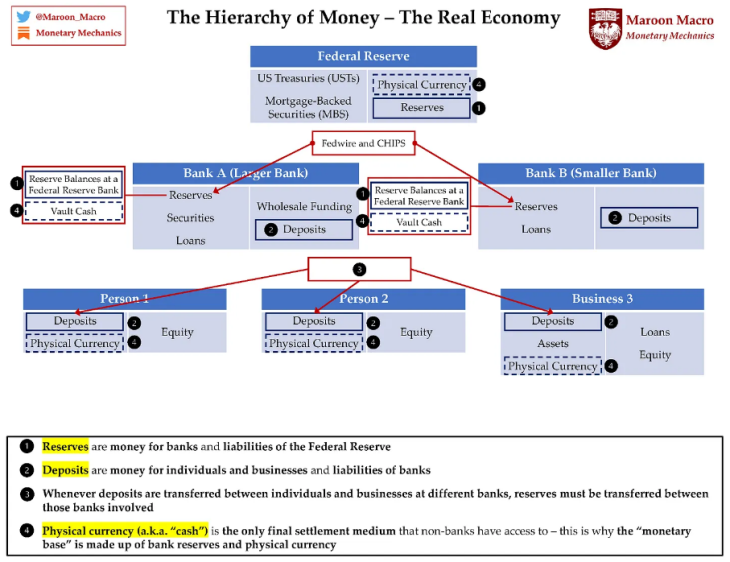

The two primary forms of money are:

Bank reserves - money for banks. These are a direct liability of the Federal Reserve (Fed), with no duration or credit risk. Banks use these tokens for settlements between themselves. In agreement with the central bank, these tokens are exchangeable at par for cash. When banks make payments to one another, the central bank moves reserves from one bank's reserve account to another.

Bank deposits - money for the real economy, these can be insured by entities such as the FDIC (explained below) and are still a liability of a commercial bank as opposed to a liability of the Fed.

Duration risk is the risk that an asset held until maturity will have lost value (e.g. the expiry date of a Treasury security), whereas credit risk is the risk that a lender will lose money when extending credit to a borrower.

Technically US bank deposits involve some credit risk, especially those in excess of the FDIC limit (~$250,000 per depositor). Here's a hilarious explanation of FDIC insurance (and Eurodollars). In short, the FDIC (Federal Deposit Insurance Corporation) is a government entity, and the insurance is for depositors so if there should be some issue with the bank, the depositors can get some of their money back.

The third type of money is:

Physical currency, cash - also a direct liability of central banks such as the Fed, and the only way everyday businesses and citizens can have access to some sort of direct liability of their central bank to use in their own economic transactions. Physical currency is fundamentally different to bank deposits in that when you transfer money e.g. with a debit card you are paying in bank deposits, not in something that is a direct liability of the federal reserve, but something that your bank owes you. As you may be aware of, the utilization of cash is fading rapidly.

If you pay in physical cash, that is a credit risk-free transaction. This brings up the topic of final settlements:

- If JP Morgan sends Citybank reserves over Fedwire, that transaction would be considered final.

- If I were to send money to you, the transaction is not final until the money has been sent from one bank to another. Even when the deposits have arrived in your account, the stage of the transaction we are involved in is by no means final, taking up to a few days to be fully confirmed.

Relative amounts of bank reserves, bank deposits, physical currency

Of the total amount of US M2 (cash and cash equivalents) bank deposits in circulation, around 10% (roughly $1 - 2 trillion) exist in the form of physical cash and the remaining 90% ($20 - 22 trillion) in bank deposits. Roughly 2% of all transactions are done with physical cash.

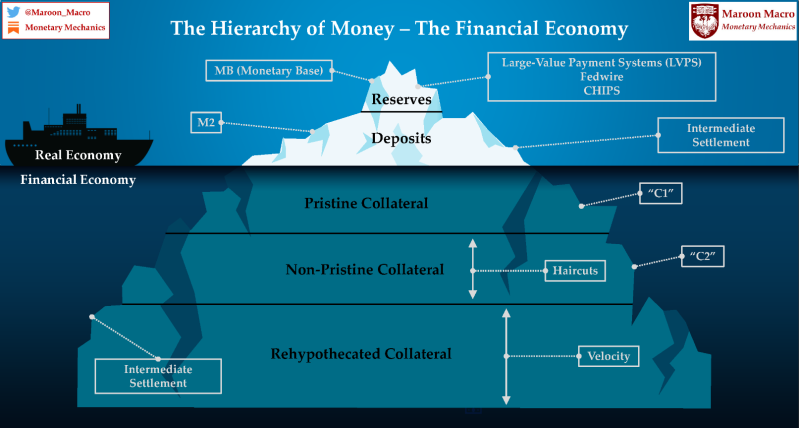

The following diagram shows how the different tiers of money interact with one another. I don't think it would be beneficial to explain it, see Maroon Macro's blog, Monetary Mechanics, if you are interested (links to some free articles at the end).

The broad strokes of money creation

The Hypocrite Twins on Youtube summarize the process briefly. The Fed (and other central banks) create money through Fed funds (different to Fed funds rate). Commercial and private banks, who have accounts at the Fed lend the money between one another in the process of fractional reserve banking, amplifying the money supply by about 10x.

FDIC insurance is the amount of bank deposits that are insured in case of a liquidity crisis. In the US this is $250,000, whereas in the Eurozone, bank deposits are only insured up to €100,000 and in the UK the FSCS covers £85,000 of bank deposits per account. So if you have more than this in your account, be sure to diversify to other forms of savings, Gold, bonds, etc., and the obligatory NFA.

Some say the system of offshore US dollars - Eurodollars - was created to avoid FDIC insurance, others say it was a way for Communist nations to hold US dollars away from regulatory bodies. Through fractional lending, these offshore US banks amplify the money supply to a level that is very hard to estimate, but the supply is likely amplified by greater than another 10x. Jim Rickards estimates that for all the money in offshore derivatives, only 1% of it is collateralized. Yikes. The TVL of the Eurodollar system is estimated to be around $57 trillion, (2018) nearly three times the size of the US economy. Double yikes. There is no consensus on the true quantity of what is referred to as Shadow Money or Black Hole Money as it exists as excesses on bank balance sheets, the only thing that's agreed upon is that it's a lot.

I will go into more detail about this in my next article.

Money creation from the perspective of banks and governments

- Monetary vs Fiscal

Monetary policy is the manipulation of interest rates and the circulating supply of money by central banks.

Fiscal policy refers to the taxation and spending of governments.

From these definitions, you can probably see where this is going.

Following Steve Keen's explanation above, if money is a liability of the banking sector, how do banks create new liabilities?

When I send money from my bank account to yours, the bank adds to yours and subtracts from mine, there is a net zero change on the liabilities side of the banking sector.

But when you borrow money from the bank, your account balance increases, the bank's assets increase and additional liabilities are created. This operation occurs on both the liabilities and assets sides of the accounting equation.

On the scale of banks and governments, the explanation is different. Take the US, they run a deficit, spending more money than they take from taxes. This increases the government's bank balance and creates money for the private sector. This operation can put more money in people's accounts via spending and welfare than is taken from them in taxation.

The money turns up in reserve accounts, private bank accounts in the central bank, in this example Master Accounts at the Federal Reserve.

Loans are the assets of both private and government money creation.

Money is the liabilities side of assets.

Bank accounts (holding bank deposits) are liabilities of the banking sector, whereas cash is a liability of the federal reserve. Money is the promise of a third party to close our transaction. As Steve says, the use of money for the purchase of goods is triangular, it involves a commodity, two parties and the promises of a bank to fulfill the transaction.

In this sense, he believes money creation is justified, as it is necessary to drive commerce. The non-commodity money crowd tends to agree.

Central banks put liquidity into markets through open market operations or QE. With the former, for example, the Bank of England pumping the bond market at the end of 2022, the central bank intervened directly in the market to put cash, but really electronic money, into the markets. However, in many cases they are merely exchanging one form of money for another. In the case of the BoE, they were exchanging reserves for Gilts (British equivalent of Treasuries). QE is often called money printing, but this really depends on your definition of money. QE usually involves central banks going into the market and buying assets, including a significant amount of liquid assets such as Treasuries and paying for them with newly created reserves. These reserves are intermediated through banks, and banks create new deposits. This results in more M1-type money being in circulation in the economy, but fewer liquid assets being in circulation. Again simply exchanging one type of asset for another, improving the liquidity of the economy, but without having really changed the size of the economy.

Government deficits, caused by fiscal spending not matched by taxes, are in the mind of Frances Copolla, much more like money printing than QE. Two scenarios, in the first, the government spends but funds the spending by issuing debts, in the second, they run an overdraft at the central bank. These two scenarios are functionally equivalent, the only difference is who is holding the debt.

Most governments operate under the first scenario, issuing debt to the private sector and spending into the economy. New debt and new money. Leveraging up the government, and increasing the amount of money or purchasing power in circulation.

To be able to lend, banks need capital and credibility. They do this by having equity, some kind of bank capital, such as shareholders' funds, retained earnings, or forms of debt that can be converted into equity.

Those defi tokens look a little less foolish now, don't they. Defi is the future of France after all.

Banks also need reserves, which enable the bank to settle lending payments. With the modern electronic banking system, banks can obtain payment for settlement very quickly (intraday). They may not have the reserves they need to settle a loan on hand, but they can borrow them, or as a last resort, they can get them from the central bank. Banks needed more reserves when the world was more cash-heavy.

Modern banks are capable of operating on zero reserves, even the Fed, which had a 10% reserve requirement. This was abolished in March 2020 (dun dun dunnnn). It did this for a few reasons, the first of which is QE. One of the effects of QE is to vastly increase the amount of bank reserves in the system.

Money printing?

Who is responsible for all the filthy money printing? The quick answer is - not central banks. Central banks manage monetary policy, whereas commercial or private banks manage fiscal policy, and it is these banks that create additional money through fractional reserve lending.

Mike Maloney dives deeper into this, with excellent visuals. When banks create money and lend it out, the borrowing entity needs to pay interest on the debt. So for every dollar lent out, there is a dollar worth of IOUs created, plus an additional dollar of interest. As Mike says, where do you get the second dollar to pay the interest? Ultimately this system is always destined to snowball until it becomes impossible to extinguish the debt.

To what extent are the different forms of money interchangeable? Can the bank reserves created by the Fed bleed into the real economy?

Banks have reserve balances at the Fed, they can make a request to the Fed to be credited in physical cash for their reserve balances. In exchange, the Fed will send them physical cash in an armored car to be stored in the bank's vault. Reserve balances and physical cash in that sense are interchangeable.

However, bank deposits and bank reserves are not interchangeable. Bank deposits are created by commercial banks when they create loans. They are a claim against the assets of a commercial bank.

Over 97% of transactions occur in the form of bank deposits, created by the money printing of commercial banks. Hence, they are also responsible for the increasing mismatch between spendable money and the basket of goods in the CPI (i.e. inflation).

If the Fed gives banks an increasing amount of reserves by doing QE, they can turn some of these additional reserves into cash or lend them out. However, banks can only lend reserves to one another, and not to businesses or individuals. To pay in reserves you need a Master Account at the Fed. (I just want to add here that Frax Finance, a stablecoin protocol, has ambitions to obtain a Fed Master Account). These accounts are only accessible to regulated depository institutions such as banks and government institutions. Sorry, but no Master Account for us average Joe's.

Reserves are stuck in the banking system unless all of us non-banking institutions go to banks and ATMs and demand to withdraw physical cash at the same time. However, due to the small amount of cash in circulation, this is an unlikely source of inflation.

The conversion of bank deposits to cash is not inflationary as the total amount of money circulating is not changed by this operation. Furthermore, as soon as the cash was spent it would likely soon be turned back into bank deposits at another bank.

Finally, all bank reserves converted to cash must be physically stored, it is highly impractical for banks to store this much cash. There is also no demand for this much cash from the private sector, no offense to any modern bank heist fantasists. Cash is also impractical for us serfs, holding large amounts of cash or Gold makes you a target for thieves. Your bullion may survive a house fire, but the cash is much more vulnerable.

Is QE inflationary or deflationary (or neutral)?

This seems to be a high-level question, as even among experts, there are different interpretations. Here is what Maroon Macro and Alf had to say (with a few other opinions sprinkled in).

The general consensus of QE is that the Fed balance sheet increases and the banking system gets flooded with reserves. It is important to ask the question, what does the Fed do with the printed money?

As Joseph Wang, a former trader at the Fed explains, the Fed uses the money created by QE to purchase Treasury Securities (usually long-dated ones).

From this point, there are a few potential outcomes:

If the Fed does QE with the banking system or if the banking system is the end seller of whatever security the Fed is purchasing, this is a direct swap of treasuries for reserves. The banking system ends up with fewer treasuries and more reserves, resulting in zero net change in the balance sheets.

However, if an institutional investor is the ultimate seller of Treasury Securities to the Fed during QE, as institutional investors do not have Fed Master accounts, the Fed will credit the institutional investors' bank with reserves, and that bank will then create deposit liabilities to issue on behalf of the institutional investor. The institutional investor will have deposits, the banking system will have more reserves and more deposits and fewer Treasuries and the Fed will have more reserves and more Treasuries.

So is QE inflationary?

The aggregate quantity or transfer of the QE funds is important, but how the deposits are used is more important.

If the Fed does QE with a non-bank, e.g. a Pension Fund or Asset Manager, the non-bank entity is likely to use these excess deposits to buy other financial assets, such as more US Treasuries, corporate credit, equities, etc.

Such deposits can leak into the real economy via direct lending and direct investment portfolios of institutional investors. Investors that have been pushed further out on the risk curve (perhaps due to the zero interest rate environment) over the past decade have been more active in private equity or direct lending. Technically there is some leakage of bank deposits that can trickle out from direct lending portfolios of institutional investors into the real economy. This is estimated to be worth a few $100 billion, which is nothing compared to the aggregate scale of QE and the total bank deposits available in the real economy.

The majority of potentially inflationary bank deposits are created by the lending of commercial banks. Their lending increases the total bank deposits available for spending.

While QE that involves buying Treasuries from Pension funds increases their bank deposits, a very small proportion of this goes towards assets in the basket of goods that make up the CPI. Alf and Maroon Macro joke that Pension funds are not buying televisions with bank deposits - the bank deposits do not really enter the real economy.

It is important to track bank deposits in the non-financial sector. If corporate consumers are earning bank deposits, there is a chance these will get into the real economy, while bank deposits owned by financial institutions are less likely to do so.

What do banks do with the extra bank reserves from QE?

Before the great financial crisis (GFC), banks used to lend to one another through the federal funds market. This market has since become deprecated. Post-GFC, banks need to maintain reserve levels that satisfy Basel III's Liquidity Coverage Ratios (LCRs) and the Dodd-Frank Acts resolutions planning and intraday liquidity requirements.

Banks need reserves to lend to the repo and fx swap markets, and to settle transactions with one another. Bank reserves are also used to settle payments within banks.

If after QE, JP Morgan has exchanged some Treasuries for bank reserves and consequently, they want to replenish their treasury portfolio, they go to buy them from e.g. Citigroup using their new bank reserves. From the perspective of banks, QE can result in a portfolio rebalancing effect, where banks use their reserves to buy risk assets from one another.

As mentioned before, exchanging reserves for reserve notes does not increase the amount of spendable money in the real economy, it is merely exchanging one form of money for another. The question is, can the additional bank reserves from QE enter the real economy and create an inflationary environment?

In a risk-off environment, banks may be satisfied with earning the reserve rate on bank reserves they receive from QE. But if they want extra yield, banks will, according to their risk mandates, buy different types of assets that satisfy their risk-return thresholds. From low to high risk vs return:

Treasuries < Corporate Credit < Equities

US Treasuries offer moderate yield and low risk, corporate credit is slightly riskier, and equities offer the highest returns in exchange for the greatest level of risk. Maybe they start with US Treasuries, bringing down the so-called risk-free rate and making them less attractive, and then creeping into riskier assets. This is the channel through which QE is thought to lead to a general increase in asset prices. By buying up risk-free assets, making them less attractive relative to other assets, investors are forced into riskier assets.

This is thought to bleed into the real economy through the wealth effect, the idea that when the retirement plans or housing prices of consumers increase, they feel more comfortable and spend more money. Consumers have a higher propensity to spend when their retirement portfolios or asset prices are doing well.

The caveat is that this is a very indirect method of targeting the level of spending in the real economy. The evidence to support the wealth effect is ambiguous at best; central banks often publish findings supporting the relationship between QE and wealth effects. Much like the Gold bugs their motivations must be considered. Others find the results are more ambiguous.

The permanent income hypothesis says that consumers will overlook temporary deviations in their net worth due to fluctuations in asset price levels. If the change in their level of wealth is seen as non-permanent, they might not necessarily adjust their spending in proportion to it.

By flooding the system with excess reserves, banks are somehow encouraged to go down the risk curve. This leads to credit and volatility compression and there is significant evidence for this. Secondary effects such as the wealth effect and the direct economic effects of QE can be closely measured.

Repo and Collateral

This is the final hurdle, if you can get through this, you will have an idea of the extent of what you do not know; this is the only way to truly ascend the Dunning-Kruger curve and become an expert.

Bank reserves and deposits are above the iceberg. Beneath the iceberg lie the different forms of collateral, which are not very widely known about or understood.

FDIC insurance imposes limits on commercial bank deposits. To institutional investors who may have millions or billions of dollars in bank deposits, the risk that a commercial bank might fail and the FDIC will not be able to reimburse them may be unacceptable. So instead they hold Treasuries, often Treasury bills so they can take less duration risk, but some may be comfortable holding coupons, depending on their risk mandate. For many institutional investors and other large participants in the financial system, US treasury securities are a form of cash.

The two major categories of collateral are pristine and non-pristine. Pristine collateral has no credit risk, US Treasuries are at the forefront of this category, but it could be argued that mortgage-backed securities are backed by the US government and hence also pristine.

Non-pristine collateral refers to assets such as private-label securities. At different times and different points in the market cycle, different types of non-pristine collateral have different levels of acceptability, which is determined by haircuts.

A lower percentage haircut means that a given security has less credit or liquidity risk. US Treasury securities repo with a 1 or 2% haircut, whereas something like a private label asset-backed security may repo at 20%, if you can even get someone to do a repo with you.

What is repo? It's short for repurchase agreement, a deal to sell a security and buy it back later at a higher price (if this sounds like lending with interest, you're getting the hang of this), the securities are usually borrowed for up to 48 hours. The additional cost or interest on securities lent out via this process is known as the repo rate, which is the risk-free overnight rate.

Finally, we have rehypothecated collateral. Due to the phenomenon that when you repo a given security you might be pledging it with the rights to reuse. For example, a hedge fund with JP Morgan as its prime broker wants to leverage their position on treasury securities. The hedge fund pledges its Treasury securities to JP Morgan, to allow JP Morgan to give the hedge fund more leverage and purchase more securities. The hedge fund pledges the securities to JP Morgan with the rights to reuse, meaning that JP Morgan can repledge those securities in repo, or transfer them and use them to settle outstanding balances on e.g. OTC derivatives, contracts, or however they see fit. Rehypothecated collateral is controlled by a measure known as velocity, an abstract concept, analogous to the velocity of money.

The velocity of money is measured as a ratio of GDP: money supply, M1 or M2 of a country. As the name implies, it is a measure of the rate at which money moves through an economy. Specifically, it is the speed at which money changes hands, in an attempt to measure the collective spending habits of constituent consumers and businesses.

If an asset manager or pension fund holds a lot of bank deposits overnight and is over the insurance limit of their respective banking system (e.g. FDIC), they are exposed to huge overnight credit risk. They would essentially be depositing millions or billions into commercial banks and not getting rewarded for it, while taking on significant risk. So most pension funds or asset managers will try to engage in transactions known as reverse repo, where they lend the bank deposits and get back proper collateral, which for them is a form of money, or the closest proxy to money that they can get. In addition to the credit risk, bank deposits are also low-yield.

That's probably enough of a segway.

Inflation bad? Fiscal and Monetarist Views on Inflation

As mentioned previously, Steve Keen and many others believe that a little inflation is beneficial. He explains that historically, hyperinflation has occurred when there is massive destruction of physical resources and the monetary authority tries to print through the crisis.

Moderate inflation undermines the store of value property of sound money, but encourages spending.

The biggest danger in capitalism is debt deflation caused by too much lending and private money creation.

Solutions?

He believes that the level of private debt needs to be taken as seriously as inflation and that private debt should be limited to 30 - 70% of GDP, for context in the US this percentage is currently 170%.

Put simply, private debt causes booms and financing credit causes slumps. To this point, he believes the solution is to decrease the level debt can reach and instead of lending speculatively, lending should be focused on innovation, (real) investing, and essential consumption.

Finally, he notes that the boom and bust cycles cannot be stopped, as they are just a function of the market, but that their size can be limited. The focus should be on controlling instability to prevent massive breakdowns.

I don't want to stray too much further (or write about inflation, it's been all over the media), but here is a simple calculation of the ideal level of inflation as explained by Steve Hanke, a proponent of monetary theory.

He uses something called the equation of exchange:

MV = PY

Where M is the money supply, V is the velocity of money, P is the price level and Y is real GDP.

The identity is:

%ΔM + %ΔV = %ΔP + %ΔY, rearranging for M we get:

%ΔM = %ΔP + %ΔY - %ΔV

If the target is 2% %ΔP and %ΔY is 2%, which as Steve says is the real GDP potential of the US, and the velocity %ΔV is falling by just under 2% (approximated to -2%), this gives a %ΔM of 6%, the golden growth rate in the money supply that achieves the target of 2% inflation.

However, the money supply is currently contracting at -2.35% (as seen on a chart of USM2), due to QT. He believes the monetary traces of inflation have almost been quashed, as this contraction has sucked it out of the system. As a monetarist, he follows the teachings of Milton Friedman, and the idea that inflation is always a monetary phenomenon, occurring due to changes in the money supply.

This is not an agreed-upon fact. There is significant data to show that inflation is not a monetary phenomenon. Here are a few examples 1 and 2.

Eugene Fama notes that such monetary principles were valid before reserves paid interest, the concept of a monetary base has since lost its meaning. He states that he does not know how to control inflation in this new environment.

John Cochrane, a Senior Fellow at Stanford and proponent of Fiscal theory, believes inflation in wages and prices originates from excessive government debt in the form of money (currency) and government bonds, more debt than people believe the government will be able or willing to repay (over a long period of time, hence today's debts and deficits are not good predictors of current inflation). Believing that money is overvalued, people do not prioritize saving and collectively spend it, causing the general price level of assets to increase.

Governments should borrow as much money as is necessary to overcome whatever challenges they face, but absent a plan for paying the money back with steady, primary surplusses over years and decades, a loss of faith in the system is likely to occur. Crucially, he notes, there is no easy formula or absolute quantity for determining what constitutes too much debt or deficit.

John compares 2008 and 2020, in the former case the Fed printed money to bail out banks, but in the process of printing announced a plan for paying it back saying 'stimulus today, debt reduction tomorrow.' This was not the case during the covid printing episode, where no such repayment plan was mentioned upon issuance of the digital money. In fact, the US government suspended budget rules, so spending does not have to come from offsets from taxes or cuts in future spending, accompanied by talk of modern monetary theory and low-interest rates, which dictate that debt never has to be paid back. People spent the airdropped Fed money, either believing that it was not a great investment vehicle or store of value, or perhaps (my opinion) believing that more money could and would be airdropped in the future.

The 2% inflation target seems to have come from New Zealand, which plucked 2% out of thin air 30 years ago while trying to tame two decades of double-digit inflation. The rest of the world's central banks followed suit. The general justification is that when the economy is flourishing the 2% target puts it under some pressure, and if there were to be a recession, rates could be lowered to 0% and this would stimulate economic growth - it's supposed to provide headroom to lower rates in a recession.

With every inflationary stint comes witch hunts for some root cause, random increases in prices of commodities, or 'random outbreaks of greed' that can easily explain away much more complex supply chain issues with respect to wages and the overall price level. You may have also heard media and JP Morgan blaming short sellers for the recent banking collapses following the collapse of their equity prices.

John concludes by saying that our central banks could easily target lower inflation or deflation, but fear of deflation that stems from the faint memory of the events leading up to the Great Depression, which began in 1933, inhibits such practices. We could have negative interest rates and a steady price level over decades and when some inflation emerges, immediately work it off, as opposed to the situation we are in now where inflation has been allowed to get wildly out of control, requiring dramatic measures to deal with. Steady deflation is what Milton Friedman referred to as the 'optimum quantity of money.' With -1% deflation, the nominal interest rate is 0 and money and bonds become perfect substitutes, people wouldn't have to spend any time thinking about cash management, we could all just sit in cash.

Creator and destroyer

As we established above, commercial banks do the majority of money creation when they lend, resulting in new loan assets on their balance sheets, also putting an amount of money equal to the loan in the customer's bank account. Assets and liabilities.

As the amount of lending in the system increases, the banking system leverages up, increasing the money supply. When the leverage rises to unsustainable levels there can be a large correction. As people repay or default on their loans, the money created at the time the loan was made gets destroyed.

Banks can also destroy money.

The destruction of money at scale can cause damaging economic recessions and even depressions.

It's all about perspective

To close, I want to briefly describe what happens when transactions are made - from a macro perspective. Jumble your brain a bit more while it is already jumbled.

Banks do not technically lend out deposits. From a macro perspective, the relevant identifier is:

Savings = Investments

OR

Investments = Savings

This identity can be read in either direction. But which comes first?

Banks create money via loans and customers can spend this money. When the money goes into someone else's bank account (of the person they bought whatever commodity from), that money becomes the savings of those people.

From a high-level (as in top-down not black belt) view, debt and savings are equal.

You can view the system as - banks lend deposits (i.e. loans = deposits), but it isn't actually how it works.

Banks create deposits, customers use them to make payments, and other customers deposit those into another or the same bank.

It's a circular flow and your perspective is shaped by the point at which you are involved.

Another way to view it is that the bank lends out money and the entire system gets more deposits, effectively becoming levered in terms of assets and liabilities. The opposite happens when a loan is destroyed.

These last two sections were from, Blockworks Macro, and their episode with Frances Copolla. Another great episode.

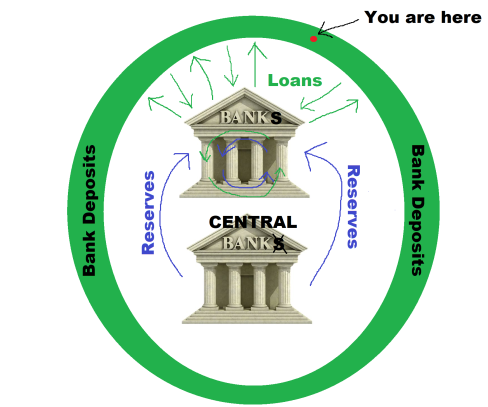

Here's a shitty diagram I drew to help visualize the system with respect to reserves, deposits and you.

Conclusion

Several perspectives emerge when the concept of money is brought into question. Money from a social and moral perspective, money from the perspective of idealists such as gold and crypto bugs and money as credit from the perspective of banks and governments. Both banks and governments are capable of creating and destroying bank ledger-based, double-accounting style money, one of the issues Bitcoin was created to overcome.

The trilemma of money properties could be satisfied by a trinity of digital currencies, programmability enables the creation of a store of value, medium of exchange, unit of account. It must be acknowledged that a centralized entity could pull all of these sound money principles under one roof. It must be acknowledged that many will never accept anything but Gold as a true store of value.

Going back to the point that debt came before barter, it seems that this may be a system that is missing from the cultural lexicon of crypto. Defi may not need a common debt system. Its Lego block-style architecture, credit to the property of composability, would enable this to be built from the ground up. Or perhaps a debt protocol could be designed to account for and tie all crypto debt together.

Keith Weiner rightly points out that Bitcoin alone cannot be used to issue debt, due to its volatility. But crypto debt could easily be issued with stablecoins. There are many protocols that issue bonds (Bond Protocol, Buttonwood, Olympus Dao etc.) as well as protocols that are now offering access to Treasuries on-chain. Another question would be - should defi try to recreate under collateralized lending, and should it mingle with real-world debt by bringing government debt such as US Treasuries on-chain? Bad debt can accrue in defi protocols where the value of collateral falls below that of the borrowed assets.

I have not discussed cash in detail, Bitcoin was supposed to be digital cash! Darrell Hubbard, the creator of Unicoin and UMU, the Universal Monetary Unit, has created a pseudo-centralized version of digital cash, enabling point-to-point transactions via NFC or Bluetooth, which he believes could be a store of value. It is likely decentralized version of such technology could be created outright, or as additional layers of Bitcoin or Ethereum. However, crypto transactions do not currently offer the privacy of cash, without the stigma of crime or laundering. What are you hiding?

In Jeff Snider's words: "money is supposed to be simple." If you care about crypto and defi you understand that being able to premeditate a system gives developers a new set of powers. These can be misused but optimistically, defi offers us the ability to create a form of money that better represents what people want and need it to be.

Many recent financial instruments were created to mend cracks in a flawed system. The Fed for example always say that they have the tools to deal with any issues, but they always end up inventing new terms and mechanisms such as BTFP. Crypto and defi do not need to recreate all of these modern instruments. It would be better to think about the function of all the parts in abstraction and create the necessary pieces on-chain.

As tradfi proponents like to say, cryptocurrency (or digital assets) is not a revolution, but an evolution of money (to justify their continued existence). The next natural, lower energy state to which money could be reduced if the necessary transitions are allowed to take place (feel free to regurgitate the second law of thermodynamics as a counter). To paraphrase Jeff Snider, when one system becomes too tame, the ingenuity of man will find a way to create a competing system that may ultimately be better. If there is anything worth speculating on it is our potential as a species to shatter all expectations.

I used the terms money and currency interchangeably, as most people do. Please do not take Mike Maloney's pedantry as an excuse to be a grammar Nazi.

I will elaborate further on many of these topics in the future with respect to crypto, cash, debt, as well as going deeper into individual protocols already primed to act as money, comparing the different contenders.

Fear and greed aside, we must accept the irresponsibility of the crypto community, a banking collapse wouldn't benefit anyone (maybe except entities that never waste a good crisis). We should want banks to survive and thrive and clean themselves up, alongside the development of crypto technology that opens banking access to anyone with a smartphone and an internet connection. In a sense, crypto and defi are everything the banking system should be, highly competitive, and only those able to retain users and remain profitable survive. Loss of trust is the ultimate failure. Whatever comes out of this tinderbox of experimentation will be truly hardened and battle-tested.