Today we are going to talk about how to define performance through concrete mathematical equations.

An investor with a decision-making process based on the principle of rationality will try to create a portfolio that allows him to maximize the return, having fixed the maximum risk he is willing to bear (depending on his degree of risk adversity), or to minimize the risk, having fixed a desired minimum return.

The return is made up of two components: interest (dividends/chedules) and the change in the value of the asset (capital gain).

For a generic security, the return at time t, will be given by:

where

are the price of the security at time t, the price of the security at time t-1 and the dividend of period t.

However, since the investor must make his choices before knowing the actual performance of the financial assets, the return is a random variable. The expected return is given by:

where

is the probability associated with the j-th yield.

Such an approach, however, requires knowledge of the probability distribution of the yield of a particular security.

Thanks to the Strong Law of Large Numbers, the calculation of the estimate of the expected return is particularly simple, as its evaluation is based only on the analysis of historical data.

Therefore, the estimate of the yield of a particular security is given simply by the arithmetic average of past returns, which will be all the more accurate the more historical data is available (i.e. the more samples we consider).

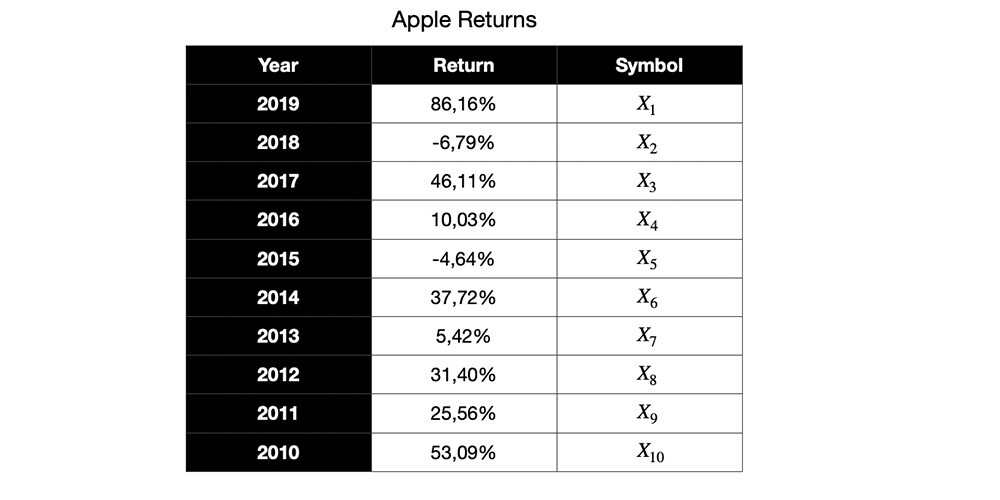

Let's take an example: let's consider Apple Inc. and its performance over the last 10 years.

Assuming that the generic annual return is statistically independent and identically distributed (i.e. they have the same probability distribution) compared to the others, by the law of large numbers, the following quantity:

is sufficiently close to the real value of the expected return.

Do you invest long term or are you for a more speculative approach?

Let me know what you think in the comments!

If you appreciate my content leave me a thumbs up ;)