A deep dive into how runaway spending, rising interest payments, and political paralysis are reshaping the world’s largest economy.

In October 2025, the United States crossed a milestone that few economists, investors, or ordinary citizens could ignore: the gross federal debt has now exceeded $38 trillion, only two months after surpassing $37 trillion. This marks the fastest trillion-dollar climb in history outside of the pandemic year, an alarming acceleration that underscores the unsustainable trajectory of America’s public finances.

According to data from the U.S. Debt Clock, the pace of federal borrowing has effectively doubled compared to the early 2000s, even as the economy grows at a far more subdued rate. The national debt, once a distant abstraction, has now become a defining challenge of America’s economic identity—one that cuts across party lines, touches every generation, and quietly shapes the future of growth, equity, and global leadership.

The Price Tag of a Superpower

To grasp the sheer magnitude of $38 trillion, consider this: it’s roughly equal to the combined annual economic output of China, Germany, Japan, India, and the United Kingdom. Each American household effectively shoulders $287,000 in debt, or about $111,000 per citizen, according to the Peter G. Peterson Foundation.

The debt is growing at a staggering clip—$4.8 million per minute, $288 million per hour, and nearly $7 billion per day. Meanwhile, the U.S government now spends close to $3 billion daily just servicing the interest on that debt. In fact, interest payments have quietly become the third-largest federal expense, behind only Social Security and defense.

And with interest rates still hovering near multi-decade highs, the cost of borrowing is compounding faster than any political will to address it. On a more symbolic level, $38 trillion could pay for a four-year college education for every graduating U.S. high school student for the next 113 years. Instead, it reflects the cumulative weight of fiscal promises that neither of the two major political parties has seriously attempted to reform.

Downgrades and Decline

The debt spiral has not gone unnoticed by credit agencies. The United States has now suffered three successive credit rating downgrades since 2011, most recently falling below the once-unquestioned AAA tier shared by countries like Germany, Denmark, and Australia. Today, America’s credit quality sits closer to that of France, Austria, and New Zealand, but even in that company, it remains a fiscal outlier.

Why? Because no other major developed economy carries such a combination of scale and imbalance—a debt-to-GDP ratio now hovering near 119% and a fiscal deficit exceeding 7% of annual output. Japan’s debt ratio may be higher, but it is funded largely by domestic savings and accompanied by a far smaller structural deficit.

The United States, by contrast, finances its excess through global borrowing, underwritten by the dollar’s role as the world’s reserve currency—a privilege that is not guaranteed forever. These rating cuts are not mere symbolism. They raise the cost of borrowing for the government, which in turn flows through to mortgage rates, business loans, and credit cards. In other words, the national debt is no longer a distant accounting problem; it’s an everyday tax on economic opportunity.

A Political Deadlock with Fiscal Consequences

Ironically, this debt crisis unfolds amid a government shutdown, now the second-longest in U.S. history. The stalemate centers on familiar ideological divisions: whether to extend enhanced tax credits under the Affordable Care Act, how to balance defense spending, and whether to reform entitlement programs like Social Security, Medicare, and Medicaid.

Yet the deeper truth is bipartisan: both parties have consistently expanded federal spending while cutting taxes or avoiding hard fiscal reforms. Recent legislation, like the so-called “One Big Beautiful Bill”—a sprawling omnibus that ballooned discretionary spending—has further widened deficits. The result is a kind of fiscal drift, where the U.S. economy continues to grow on paper but erodes its long-term resilience.

The unwillingness to “touch” politically sensitive programs reflects a collective denial about trade-offs. Entitlements and defense now account for nearly two-thirds of federal spending, leaving little room for flexibility. As the population ages and healthcare costs continue to rise, these automatic outlays will only grow faster, leaving interest payments as the next uncontrollable line item.

The Global Ripples: Gold, the Dollar, and Bond Yields

Markets are already responding. Gold prices have surged sharply this year, despite occasional pullbacks, as investors seek refuge from fiscal instability and a weakening dollar. The U.S. currency has lost ground against other major currencies, eroding some of the benefits of its reserve status. Meanwhile, government bond yields have climbed, reflecting investor anxiety over long-term solvency.

High yields, however, are a double-edged sword. On one hand, they attract capital and signal confidence in U.S. growth. On the other hand, they increase borrowing costs for everyone, from homeowners to small businesses to state governments. If these yields remain elevated for an extended period, they could stifle investment, slow hiring, and ultimately choke economic growth—creating a feedback loop that worsens the very debt problem that caused them.

Lessons from History: When Debt Meets Denial

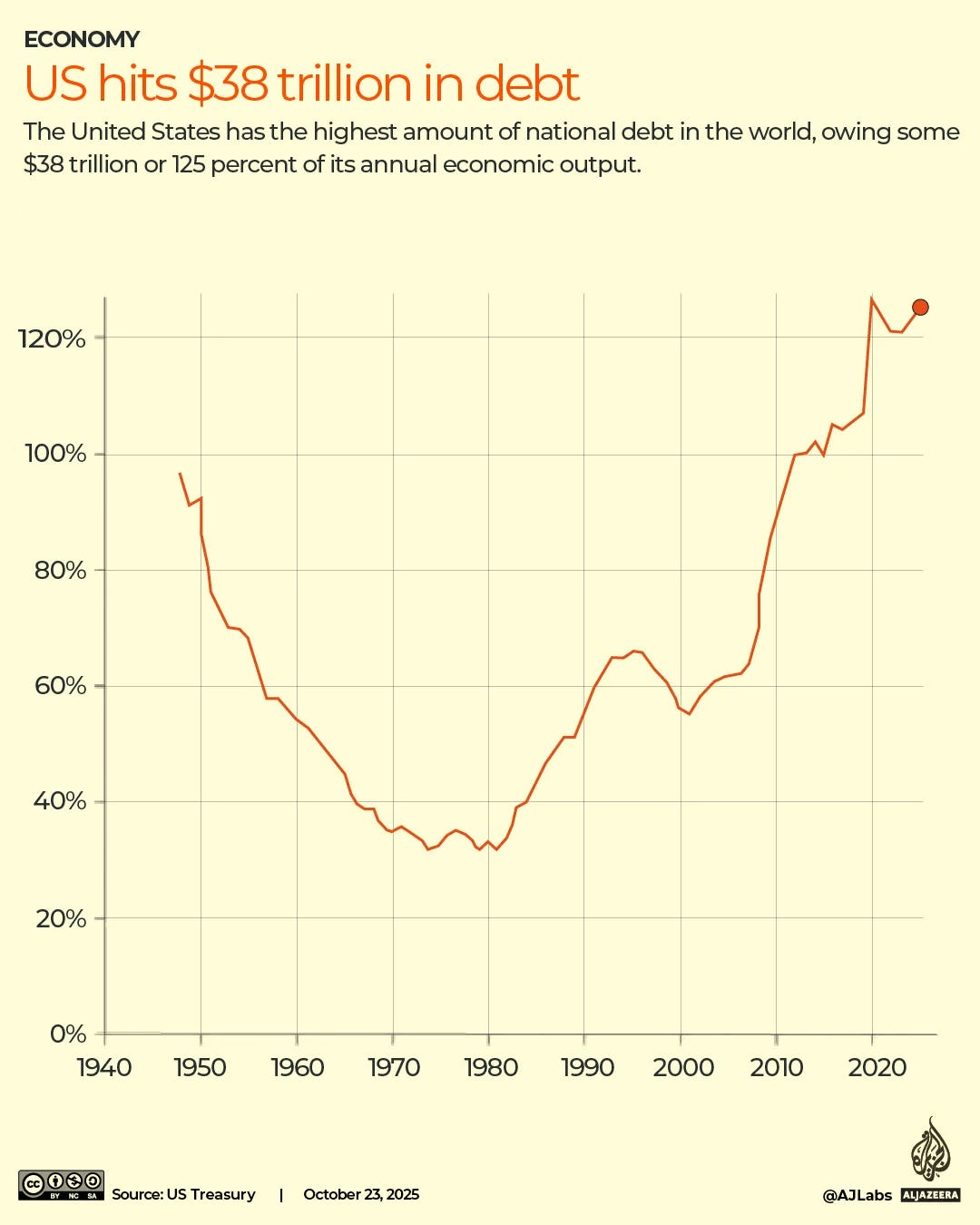

The chart above tells a story that stretches back to the 1940s. After World War II, U.S. debt-to-GDP soared past 100%, only to fall dramatically in the decades that followed, thanks to strong postwar growth, restrained spending, and inflation that gradually eroded nominal debt. By the 1970s and 1980s, that ratio had stabilized below 40%.

Today, the curve has reversed. Beginning in the early 2000s—with the wars in Iraq and Afghanistan, followed by the financial crisis, pandemic relief, and expansive fiscal policy—the trajectory has been steadily upward. The debt-to-GDP ratio now stands at levels unseen since the war years, with no credible plan for reduction.

Economists warn that this time is different. The U.S. can no longer rely on rapid growth or inflation to offset debt in real terms, and political polarization has made structural reform nearly impossible. The danger, then, is not an immediate collapse but a slow erosion of credibility—a future in which debt service crowds out public investment, productivity stalls, and the next crisis meets a government with no fiscal ammunition left.

A Call for Fiscal Realism

It’s not too late to act, but the window is narrowing. To put it simply: The earlier the U.S gets started, the easier it will be to fix. That means rethinking the sacred cows of both parties—questioning tax loopholes, reevaluating entitlement formulas, and aligning defense budgets with strategic realities.

Fiscal sustainability isn’t just an accounting issue; it’s a moral one. It asks whether today’s leaders are willing to make modest sacrifices now to spare future generations from impossible choices later. The debt may be a number, but it’s also a mirror—reflecting the nation’s values, priorities, and capacity for discipline. As America stares down its $38 trillion reflection, the question is not whether it can afford to change course, but whether it can afford NOT to.

Originally Published on Substack.