A legal tax-optimization strategy lets the rich rebalance portfolios without realizing capital gains — here’s how it works.

In the vast ecosystem of American finance, few things are as predictable as the relentless pursuit of tax efficiency by the ultra-wealthy. For decades, Wall Street has engineered strategies that allow investors to minimize or entirely avoid paying capital gains taxes on their vast portfolios. One of these sophisticated maneuvers is the “351 conversion,” a relatively obscure yet increasingly popular method of converting private portfolios into exchange-traded funds (ETFs) while keeping the IRS at bay.

It sounds almost too clever to be true. But as Bloomberg recently illustrated, this process is not only real, it’s completely legal.

A Quiet Revolution in Wealth Management

To understand how 351 conversions work, imagine a wealthy investor who holds a Separately Managed Account (SMA) — essentially a personalized basket of stocks curated by a financial advisor. Over time, certain stocks in that account may balloon in value. For instance, let’s say Nvidia, the AI chipmaker whose stock has skyrocketed over the past few years, becomes disproportionately large in the portfolio.

Normally, if that investor wanted to rebalance, perhaps by selling some Nvidia shares and reallocating into other assets like an S&P 500 index fund, they’d face a hefty capital gains tax bill. For high-net-worth individuals, that can mean handing over 20% or more of their profits to the federal government, plus potential state taxes.

But there’s a way around that. Rather than selling those shares, the investor can convert their SMA into an ETF — a process governed under Section 351 of the U.S. tax code. This provision allows investors to transfer assets into a corporation in exchange for shares of that corporation — tax-free, so long as certain ownership and control requirements are met.

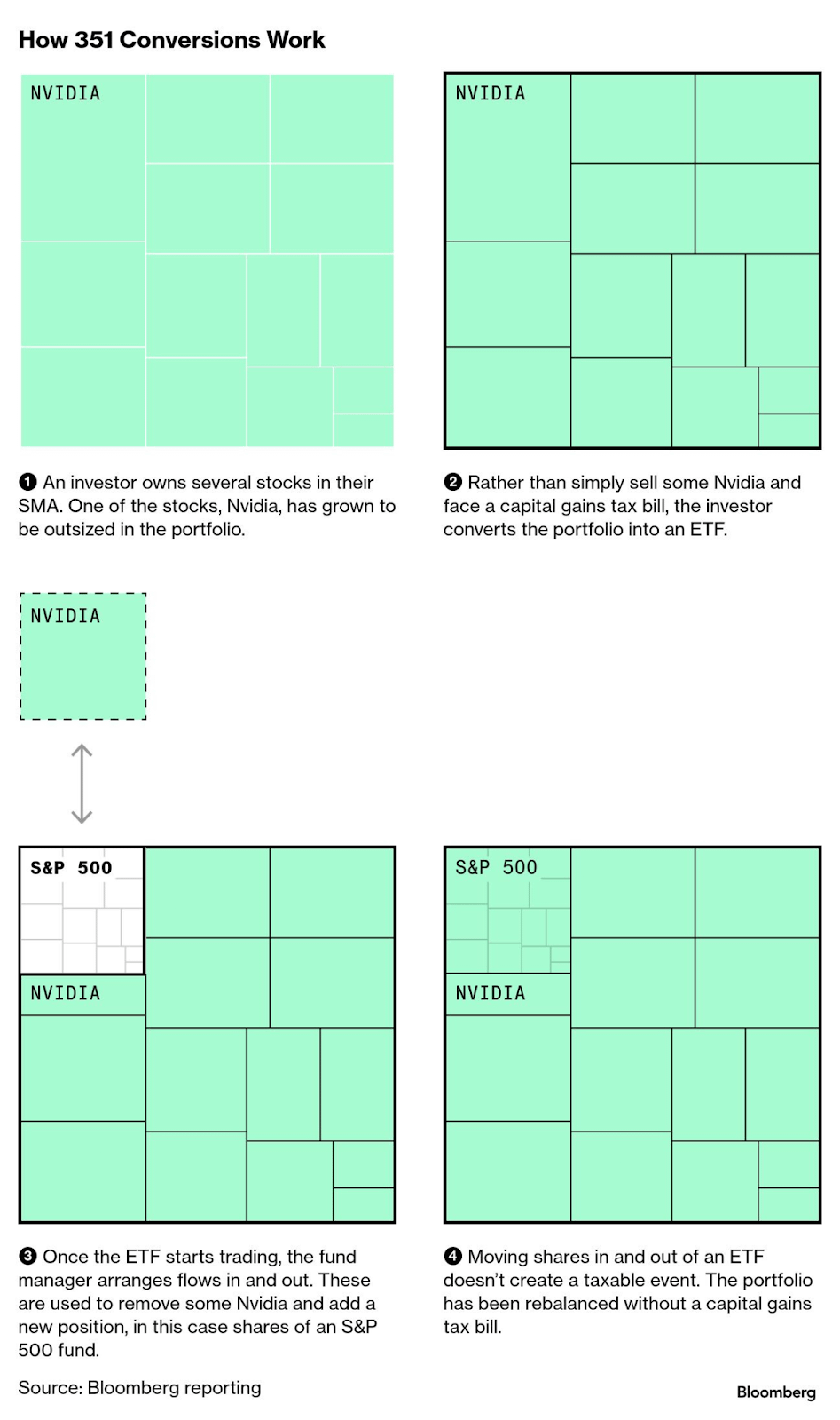

Visualizing the Trick: The ‘351 Conversion’ in Action

As shown in Bloomberg’s explainer diagram (below), the process unfolds in four stages:

-

An investor’s portfolio becomes unbalanced.

Over time, one stock — say Nvidia — dominates the holdings, creating concentration risk. -

The portfolio is converted into an ETF.

Instead of selling, the investor wraps the entire portfolio into an ETF structure. This maneuver avoids triggering any taxable events. -

ETF managers adjust the holdings.

Once the ETF begins trading, the fund manager can swap out portions of Nvidia and add new assets, such as S&P 500 index fund shares, through a process called “in-kind creation and redemption.” -

Rebalancing happens — tax-free.

Because moving shares in and out of an ETF doesn’t count as a taxable sale, the investor’s portfolio is effectively rebalanced without a single dollar of capital gains tax owed.

In essence, the investor has side-stepped a massive tax bill and, in the process, transformed a concentrated portfolio into a diversified, professionally managed ETF.

Wall Street’s Tax-Optimization Machine

The 351 conversion is just one cog in Wall Street’s ever-growing tax-optimization complex. Over the past decade, financial engineers have honed dozens of strategies that let the wealthy defer, minimize, or erase taxes on capital appreciation. These include “heartbeat trades,” where ETF managers rapidly swap securities in and out to purge built-up gains before they become taxable, and “in-kind redemptions,” where appreciated shares are exchanged rather than sold.

Each of these relies on the same tax treatment that gives ETFs an advantage over mutual funds: the ability to trade securities without triggering capital gains. For wealthy investors, 351 conversions are particularly attractive because they combine customization with tax efficiency.

Unlike traditional ETFs, which are standardized and publicly traded, these conversions create bespoke ETFs that hold the investor’s own assets — effectively turning a private portfolio into a tradeable financial product. And thanks to Section 351, the transition itself can occur entirely tax-free.

Why the IRS Can’t Stop It (Yet)?

The legality of this maneuver lies squarely in the Internal Revenue Code. Section 351 was originally designed to help entrepreneurs and corporations exchange property for stock without incurring immediate taxes, a provision meant to encourage business formation and capital investment.

However, as financial innovation accelerated, tax lawyers realized that the same principle could apply to investment portfolios. If an investor contributes stocks to a newly formed ETF, and that ETF meets the statutory requirements, the transaction qualifies as a non-recognition event, meaning the IRS doesn’t view it as a sale.

In other words, the investor hasn’t “realized” a gain. They’ve merely swapped one ownership form for another. Regulators are aware of the loophole, but closing it is tricky. ETFs have become a $12.7 trillion cornerstone of the U.S. financial system, and their tax advantages are part of what makes them so attractive to investors. Any attempt to clamp down on 351 conversions could ripple through the industry, potentially upsetting institutional investors and asset managers alike.

Who’s Using It — and Why?

According to Bloomberg, a growing number of wealth management firms and private banks are now offering 351 conversions to high-net-worth clients, often with portfolios of $50 million or more. These investors are typically sitting on large unrealized gains and looking to diversify without paying a tax penalty. Firms such as Aperture Investors, Halo Investing, and specialized ETF creators have begun to market these conversions as part of broader tax-planning services.

For clients, the appeal is obvious: rebalance, diversify, and modernize — all while keeping Uncle Sam’s hands off their profits. In some cases, even family offices have formed their own ETFs, using 351 conversions as the bridge. Once created, these private ETFs can be traded, added to, or even passed on to heirs, further enhancing long-term wealth preservation.

A Growing Debate Over Fairness

Unsurprisingly, the strategy has reignited debates about tax fairness and inequality. For everyday investors, selling appreciated stock means paying the piper. For the wealthy, creative structuring and high-priced legal advice provide a legal escape hatch. Proponents, on the other hand, argue that these strategies utilize existing legal frameworks, ones that are available to anyone with sufficient assets to make them worthwhile. They see 351 conversions as an evolution of the ETF industry’s tax efficiency, not an abuse of it.

The Bigger Picture: A Two-Tier Tax System

At its core, the rise of 351 conversions underscores a broader truth: the U.S. tax system operates on two tiers. One for wage earners, who have taxes withheld at the source, and another for asset owners, who can defer, minimize, or eliminate taxes through sophisticated planning. As long as laws like Section 351 remain in place, Wall Street will continue to “innovate” around them.

And unless lawmakers move to tighten definitions of “ownership” and “realization,” these strategies will remain perfectly legitimate. That raises an uncomfortable but important question, one that policymakers and investors alike must confront: Should access to tax efficiency depend on wealth and sophistication, or should the same opportunities apply to everyone?

Originally Published on Substack.