Consumer-centric Fintech startups have added 200M+ accounts while raising $7.6B in equity over the past decade

Arecent report from the CB Insights sheds further light on how the global landscape of Fintechs has evolved over the past few years. The analysis points towards massive consumer adoption driven by technological innovation, which continues to grow across the global financial ecosystem.

The notable trend is of these Fintechs beginning to expand to new products & markets, which spells trouble for the incumbents of the legacy financial system. The research deliberately excluded data from the Giant Fintechs Paytm (India, 350M users) and Ant Financial (China, 800M mobile wallets) owing to their population size. Imagine how skewed the growth projection would have been, were they to be included in the data.

Before moving on to look at the reasons behind the exponential growth of these Digital-first or “challenger banks,” lets review at some of the notable trends & stats which emerged from the report:

- Coinbase was the most valuable — $8B valuation.

- SoFi was the most well-funded — $2.54B in equity funding at a $4.8B valuation.

- Credit Karma is expected to be the top revenue-generating with $1B in 2019 (up from $700M in 2017).

- EToro was the first to report an equity raise of $1.7M Series A in 2007.

- Dave was launched in October 2016 & the youngest startup to reach 1M+ customers.

- Propel’s App Fresh EBT has seen massive under the radar growth of over 2M monthly active users — but according to Google Play data, the mobile App has actually more than 5M downloads.

- The following 12 Fintech startups have become Unicorns ($1B+ valuation) — Nubank, Robinhood, Coinbase, Toss, Credit Karma, Revolut, SoFi, N26, Monzo, Chime, Circle, and Transferwise.

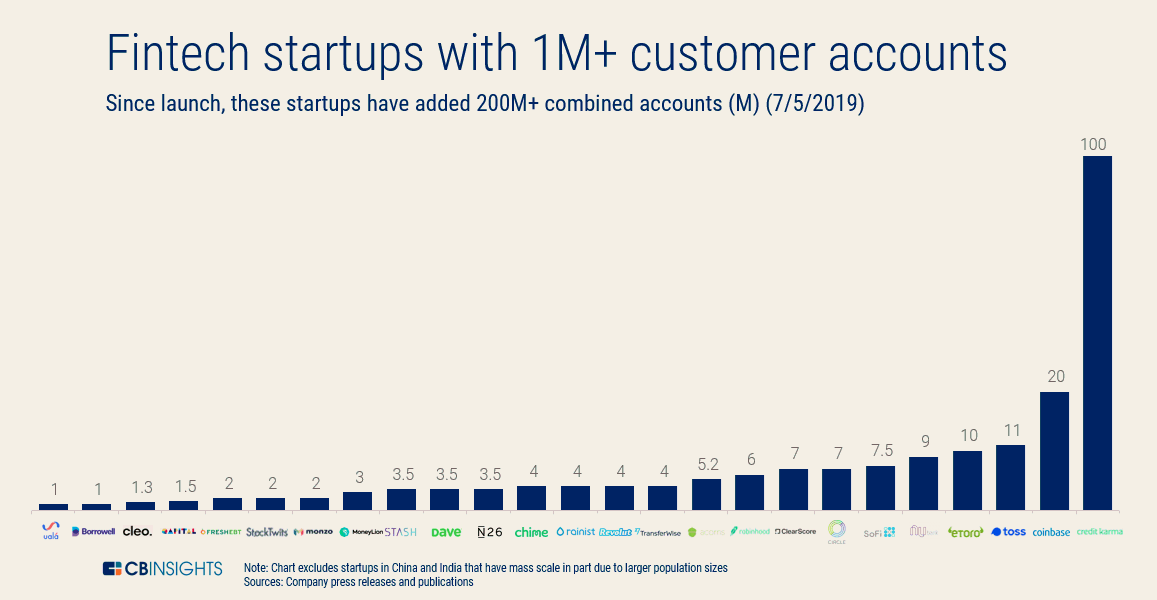

- And finally, 25 of these Fintechs have accumulated $1M+ customers (Figure 1) — Credit Karma was the largest & accounted for almost half of the total clientele with 100M users, followed by Coinbase with 20M customers.

Figure 1

These Fintech startups are changing consumer behavior by providing access to financial services in innovative ways. There are a number of factors which are driving these changes:

- Demographic shifts — Customer acquisition strategy is centered around first-time investors using digital channels. The Next-gen platforms are enticing to the Millennials & Generation Z, which are much more receptive to technology-enabled solutions than traditional banking channels of brick and mortar banks.

- New Products & Services — Startups are aggressively marketing & adding the emerging digital asset classes (cryptocurrencies) to their product line. They are way ahead of the incumbents in embracing this new model & enticing the new generation.

- Business Model shifts — Mobile-first delivery models are not only replacing the old delivery mechanism, which has little or no overheads, but also brings competitive pricing & transparency to the process. This is posing new challenges to the incumbents.

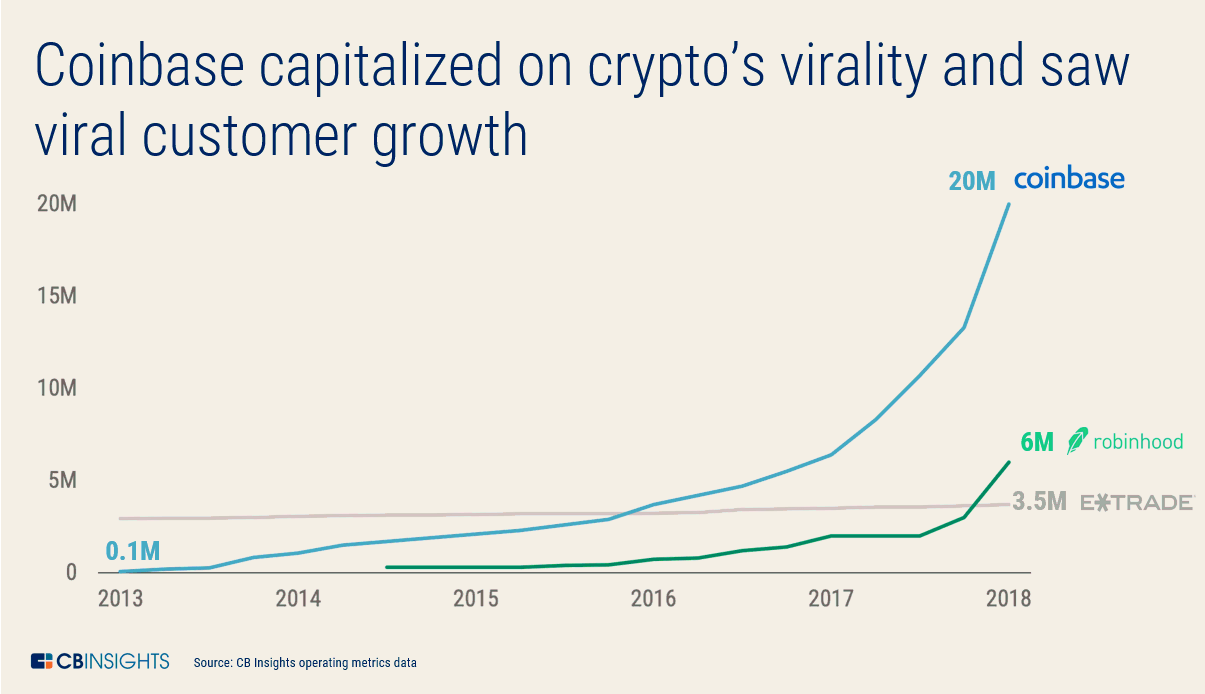

Figure 2

Less Stringent Regulations

Of the seven challenger banks — Uala, N26, Monzo, Qapital, Chime, Nubank, and Revolut — Nubank is by far the largest with 9M customers. The fastest growth in this segment is seen by digital-only banks located outside the U.S, with the exception of Chime and Qapital. The growth is mainly attributed to the less stringent regulatory requirements as we see in Europe where Open banking regulations have lowered the entry barriers for these Fintechs.

EU based Monzo & N26 have launched digital-first banks via their Apps as they wait for full bank charters. Brazil’s Nubank has received regulatory approval last year to launch a bank. With the loosening regulations, the cropping up of these challenger banks & their vertical growth is all set to continue.

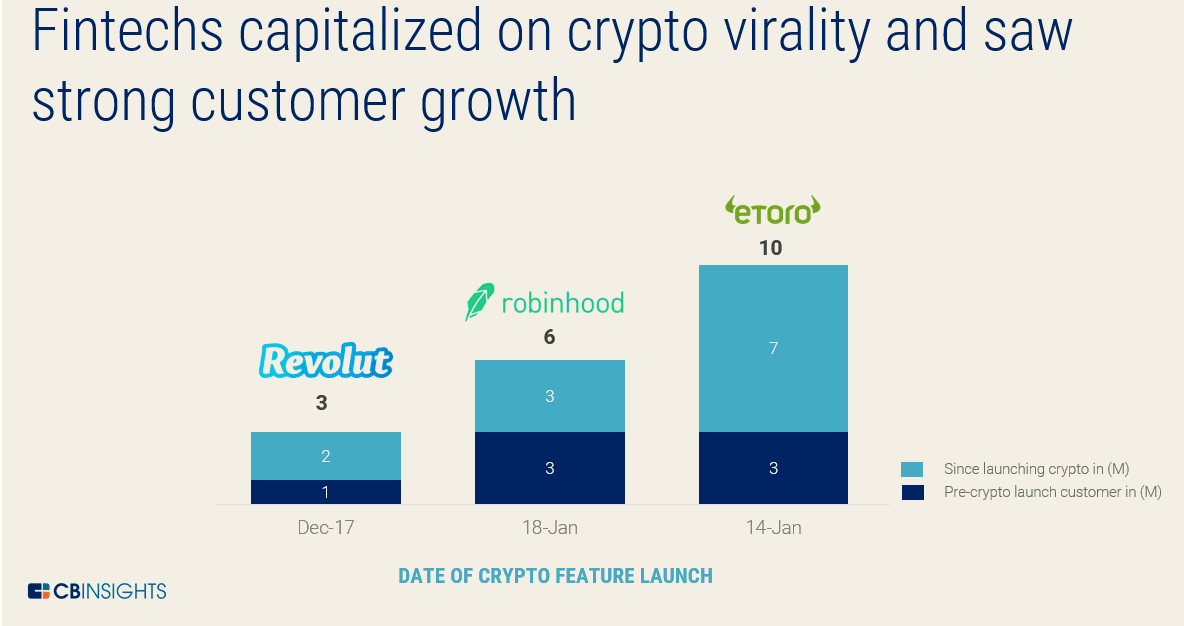

Figure 3

Crypto Virality

Cryptocurrencies have gained immense traction as a new-age investment. And these companies have really leveraged the viral nature of the digital assets to make an entry into the Fintech space. Coinbase & Circle were two of the earliest players to capitalize on this trend. Coinbase — one of the first & the biggest Crypto exchanges in the U.S amassed 20 million users in just two years. Now compare this to the incumbent E-trade, which has been in business for the past four decades still has less than 5 million customers (Figure 2).

Other startups also responded to the demands of the customers for access to cryptocurrencies — these included stock trading Apps EToro, Robinhood & challenger bank Revolut, all three of whom added 2 million customers after the addition of the Crypto offerings to their product lines. Despite a Crypto bear market in 2018, they showed impressive growth to their user bases — EToro topped all of them with 10 million accounts after their crypto launch in January 2019 (Figure 3).

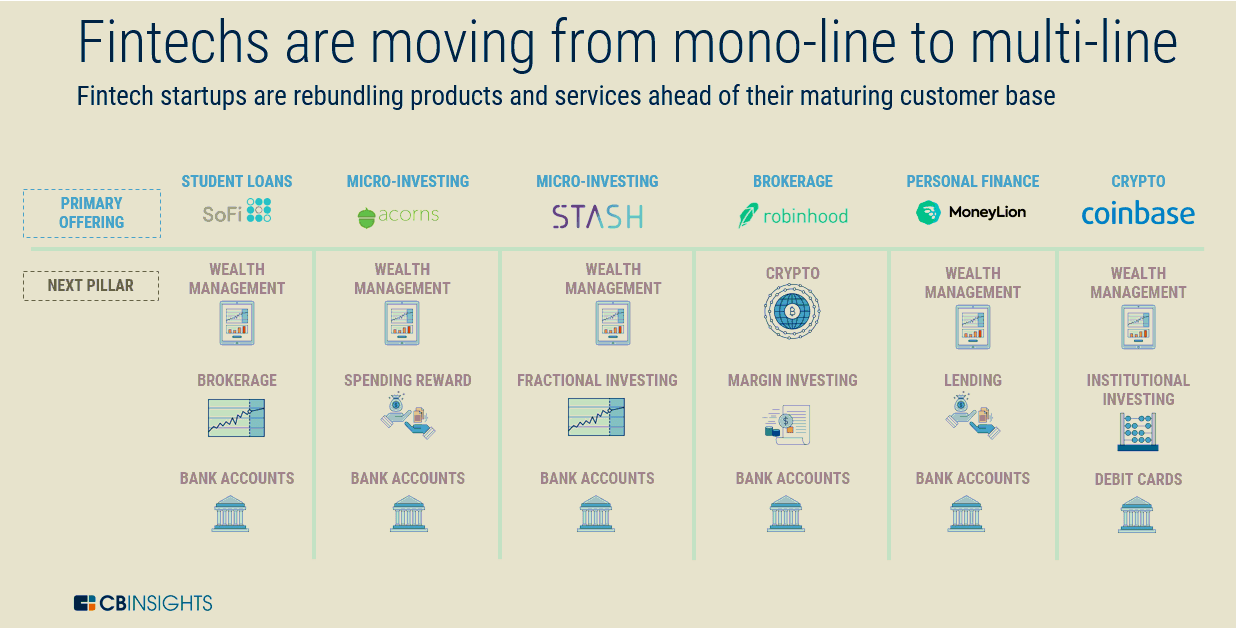

Figure 4

Multi-Line Rebundling

Most of these Fintechs started off as mono-line business with their market niches — Acorns & Stash were micro-investing Apps, SoFi offered alternative student loans, Coinbase as a crypto exchange & MoneyLion as a personal finance App. However, growing customer bases coupled with increased funding encouraged them to switch to a multi-line business model (Figure 4). This enabled them to generate more revenue while providing a basket of additional services under one roof.

The rebundling of Product offerings is seeing concentration around bank accounts — like the Open banking regulations introduced by the EU, which has made it easier for these Fintechs to launch bank accounts. On the other side of the pond, in the U.S, Fintechs are partnering with the existing banks to leverage their bank charters to launch their own bank accounts & debit accounts — members of the 1M+ account club Transferwise, SoFi, Stash, Acorns, MoneyLion, Coinbase, Dave, and Robinhood have all done so.

The disruption to the legacy financial system will become even more pronounced as regulatory clarity takes shape & these Fintechs reach to scale in their initial market.

Medium | Twitter | LinkedIn | StockTwits | Telegram