New tariffs could ignite inflation, shrink GDP, and slash jobs—who will suffer the most: the U.S., Canada, or Mexico?

So, this tariff rollercoaster that fired up as soon as Trump took the oath of office is still throwing the global economy for a loop, like a wild reality TV show. Earlier today, Trump slammed the brakes on the Canada and Mexico tariffs, tossing them another 30-day timeout until April 2, when his “reciprocal tariffs for all” scheme kicks in. Even with this break, about half of Mexico’s imports and only 37% of Canada’s imports will dodge the tariff bullet.

You can bet tariffs aren’t going anywhere, and neither is the back-and-forth. But Markets are already showing signs of tariff fatigue as Dow Jones tumbled 400 points today, and the tech-heavy Nasdaq closed in correction territory after a drop of 2.61% for the day. Investors can see the pain down the road that these tariffs are going to inflict on consumers and the broader economies.

With the clock now ticking toward April 2, 2025, when those broader reciprocal tariffs kick in, the economic fallout is already making waves. Thanks to some interesting data from the Brookings Institution and the Federal Reserve Bank of Boston (pictured below), we have a front-row seat to see how inflation, employment, and GDP might take a hit in all three countries. Let’s dive in and compare how each country might fare.

Inflation Pressure Points

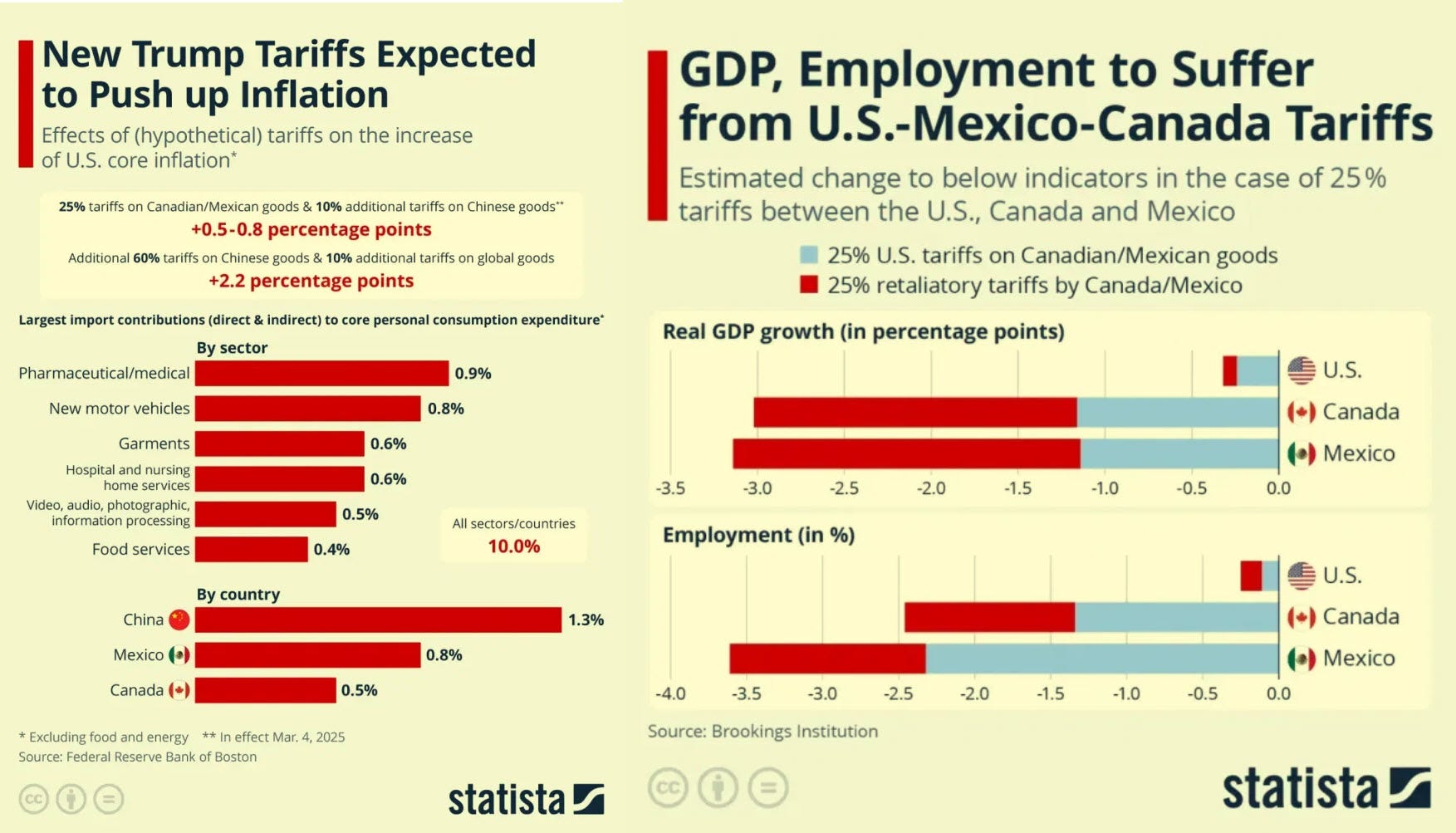

The left panel of the infographic reveals a troubling inflationary outlook for the United States. The initial 25% tariffs on Canadian and Mexican goods, combined with 10% additional tariffs on Chinese goods, are projected to increase U.S. core inflation by 0.5-0.8 percentage points. More concerning is the scenario with additional tariffs—60% on Chinese goods and 10% on global goods—which could push U.S. inflation up by a substantial 2.2 percentage points.

The sectoral breakdown shows pharmaceuticals and medical products contributing most significantly to inflation (0.9%), followed closely by new motor vehicles (0.8%). When viewed by country of origin, Chinese imports have the largest inflationary impact at 1.3%, with Mexican and Canadian imports contributing 0.8% and 0.5%, respectively.

GDP Contraction

The right panel paints a sobering picture of GDP impacts. While the United States would experience some contraction under 25% tariffs, Canada and Mexico face considerably steeper declines:

-

The United States could see GDP growth reduced by approximately 0.1-0.2 percentage points.

-

Canada appears significantly more vulnerable, with projections showing a GDP contraction of approximately 3.0 percentage points.

-

Mexico faces the most severe impact, with GDP potentially dropping by over 3.0 percentage points.

These disparities highlight the asymmetrical power dynamics in North American trade relationships, with the smaller economies bearing disproportionate consequences of trade friction.

Employment Outlook

The employment picture mirrors the GDP projections in both pattern and severity:

-

U.S. employment would decline marginally, perhaps by 0.1-0.2 percentage points.

-

Canadian employment could drop by roughly 1.8-2.4 percentage points.

-

Mexican employment faces the steepest decline of approximately 2.3-3.6 percentage points.

What's particularly noteworthy is that retaliatory tariffs (shown in red) would cause significantly more damage than the initial U.S. tariffs (shown in blue) across all metrics and countries. This suggests a potential lose-lose scenario in any escalating trade confrontation.

Comparative Analysis: Who Stands to Lose Most?

When comparing the three economic indicators across the three countries, a clear pattern emerges:

United States: While facing increased inflation domestically (potentially hampering the Federal Reserve's inflation control efforts), the U.S. economy shows relatively modest GDP and employment impacts compared to its neighbors.

Canada: With substantial exposure to U.S. markets and significant integration in manufacturing supply chains, Canada occupies a middle position in vulnerability—less exposed than Mexico but considerably more vulnerable than the United States.

Mexico: Emerging as the most vulnerable of the three economies, Mexico faces the steepest projected declines in both GDP and employment, suggesting its high dependence on U.S. trade and limited short-term alternatives for economic adjustment.

These projections highlight the deep interconnectedness of North American economies after decades of integration under NAFTA and subsequently USMCA. As these tariff policies move from projection to implementation, policymakers in all three countries are scrambling to consider mitigation strategies for these anticipated economic shocks, particularly for the most vulnerable industries and workers in their respective economies.

Originally published on Substack.