Government bond yields across the US, UK, and Japan are climbing sharply as markets fear a renewed era of monetary tightening.

Global government bond markets are sending an unmistakable warning signal. From Washington to London to Tokyo, investors are dumping long-dated sovereign debt, driving yields sharply higher and reigniting fears that the world economy may be entering a dangerous new phase defined by inflation persistence, geopolitical instability, and mounting fiscal stress.

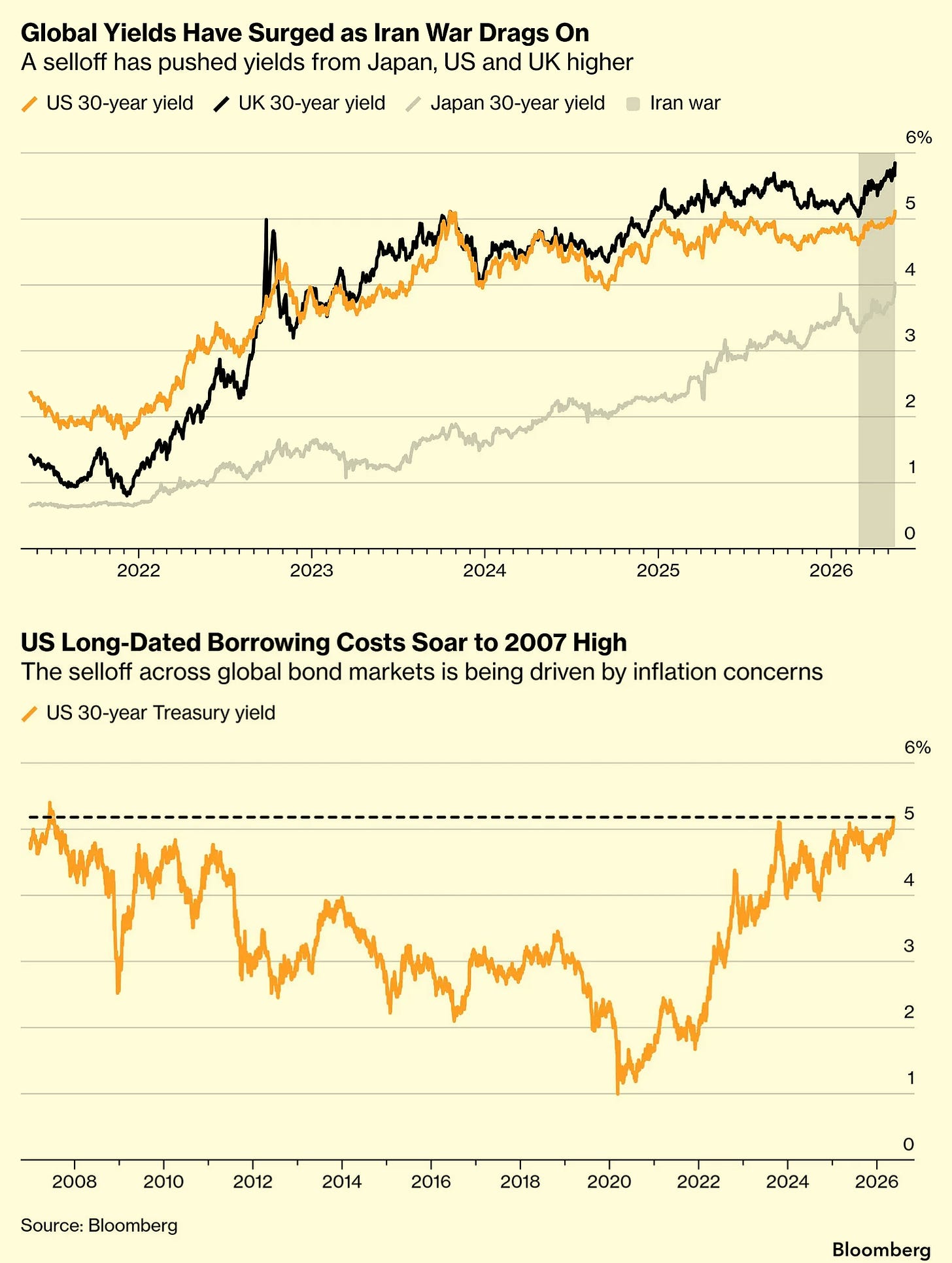

The latest selloff in government bonds reflects more than ordinary market volatility. It represents a growing belief among investors that the Iran war and its resulting energy shock could force central banks back into aggressive monetary tightening just as economies were hoping for relief from years of elevated interest rates.

According to Bloomberg data (below) shown in the attached charts, yields on 30-year government bonds in the U.S, the U.K, and Japan have climbed dramatically since the outbreak of the Iran conflict. US 30-year Treasury yields surged to roughly 5.20%, a level not seen since just before the 2008 global financial crisis. UK 30-year yields climbed above 5%, while Japan’s 30-year yields rose toward 3.5%, marking an extraordinary shift for a country that spent decades battling deflation and ultra-low interest rates.

Oil Shock Revives Inflation Fears

At the center of the bond market panic is energy. Crude oil prices have climbed sharply as the Iran conflict threatens global supply routes and raises fears of prolonged instability across the Middle East. Markets had hoped the recent US-China summit might produce diplomatic momentum capable of easing geopolitical tensions or stabilizing global trade expectations.

Instead, the summit ended without meaningful breakthroughs, deepening investor concerns about fragmentation in the global economy. Higher oil prices matter because energy costs ripple through virtually every sector. Transportation, manufacturing, food production, aviation, logistics, and consumer goods all become more expensive.

This creates a second-wave inflation effect that central banks fear most: inflation expectations becoming embedded across the economy. Those fears intensified after back-to-back US government reports showed stronger-than-expected increases in both consumer prices and wholesale inflation. The data reinforced the view that inflation may not return to central bank targets as quickly as policymakers previously anticipated.

For bond investors, that changes everything. When inflation rises, the fixed payments offered by long-term government bonds become less attractive in real terms. Investors, therefore, demand higher yields as compensation for inflation risk. That dynamic pushes bond prices lower and borrowing costs higher.

The Return of “Higher for Longer”

Only months ago, markets were pricing in interest rate cuts from the Federal Reserve and other major central banks. That narrative has now shifted dramatically. Investors increasingly believe central banks may need to maintain restrictive monetary policy for far longer than expected—or even resume rate hikes if inflation accelerates further.

The implications are profound. Higher long-term yields increase borrowing costs across the entire economy. Mortgage rates rise. Corporate financing becomes more expensive. Governments face larger debt-servicing burdens. Equity valuations come under pressure as future earnings are discounted more heavily.

The Bloomberg chart highlighting US long-dated borrowing costs is particularly striking. The 30-year Treasury yield has returned to levels last seen before the global financial crisis, erasing nearly two decades of ultra-low-rate assumptions that shaped financial markets after 2008. This is not simply a temporary repricing. It may represent a structural transition away from the low-inflation, low-rate environment that dominated the post-crisis era.

Government Debt is Becoming a Growing Concern

The current bond market stress is not driven solely by inflation or war. Fiscal concerns are also playing an increasingly important role. Governments across advanced economies accumulated enormous debt loads during the pandemic years, followed by additional spending related to industrial policy, defense modernization, infrastructure programs, and social support initiatives.

At the same time, aging populations continue to place pressure on public finances through pension and healthcare obligations. As deficits expand, governments must issue more bonds to finance spending. But investors are now demanding significantly higher compensation to absorb that supply, particularly for longer-dated debt vulnerable to inflation uncertainty.

The result is a dangerous feedback loop. Higher yields increase government borrowing costs, which can worsen deficits further, requiring even more debt issuance. That dynamic has become especially visible in the United States, where Treasury issuance has surged amid rising fiscal imbalances.

Japan’s participation in this global selloff is equally important. For decades, Japanese government bonds anchored global fixed-income markets with extremely low yields due to the Bank of Japan’s ultra-accommodative monetary policies. The recent rise in Japanese long-term yields suggests even the world’s most persistent low-rate economy may be normalizing under inflation pressure.

Kevin Warsh Inherits a Difficult Federal Reserve

All of this now lands on the desk of newly confirmed Federal Reserve Chair Kevin Warsh. Warsh enters office at one of the most complicated moments in modern central banking. President Donald Trump spent much of the past 15 months publicly criticizing outgoing Fed Chair Jerome Powell and demanding interest rate cuts to support growth and financial markets.

But the market environment Warsh inherits may force the opposite response. If inflation continues accelerating because of energy shocks and geopolitical instability, the Federal Reserve may have little choice but to maintain tight monetary conditions despite political pressure for easing. That creates an exceptionally difficult balancing act.

Financial markets increasingly appear as fragile as the geopolitical landscape itself. The synchronized rise in global bond yields is not merely a technical market adjustment. It reflects a broader reassessment of inflation, risk, fiscal sustainability, and political uncertainty in an era where economic stability can no longer be taken for granted.

Originally Published on Substack.