The amazing parts of DeFi

In part 1 of this series we had a look at the broader picture of the financial ecosystem. In part 2 we went down the DeFi rabbit hole and discovered the first two ingredients for an excellent DeFi “meal” to understand the big picture. We talked about lending/borrowing as well as Automated Market Makers and Liquidity Providers.

With part 3 we’ll dig even deeper. You’ll learn about the truly amazing parts in this new DeFi world, before we’ll resurface and extract our lessons for retail users and retail banks in later parts.

So, here we go with the next DeFi ingredients: Let’s bring some spices into our meal…

Photo by Nastasya Day from Pexels

Photo by Nastasya Day from Pexels

Ingredient #3: StableSwaps & beyond

We talked about providing liquidity to a Decentralized Exchange (DEX) and the danger of impermanent loss in part 2. There are several tactics to avoid impermanent loss. An interesting one is to have the same(!) kind of asset on both sides of a liquidity pool.

You might wonder:

Why should someone set up a trading pair with the same asset on both sides? Well — nobody would.

I spoke about the same kind of assets — like different dollar-pegged stable coins.

And there are many reasons for these stable coin trading pairs on DEXes. The main one is that many exchanges offer just one trading pair to buy “your favorite token” with a stable coin — very often it’s Tether ($USDT). If you happen to own $DAI instead of $USDT you need to first swap your $DAI to $USDT before you can buy “your favorite token”. So, there is an obvious use case for these stable coin to stable coin trading pairs.

In fact, this use case is HUGE.

Firstly, there are quite some different stable coins on the market like $USDT, $USDC, $DAI, $BUSD, $PAX — just to name the ones currently in the TOP 60 of CoinGecko…

Secondly, many traders actively use stable coins as temporary “safe harbor” between trades if crypto markets are going down. If you have a quick look at the statistics in Uniswap stable coins sit on #2, #3 and #4 regarding liquidity (500m$) and trading volume (200m$) at the time of writing (see screenshot below).

Screenshot Uniswap / 2020–12–27

Screenshot Uniswap / 2020–12–27

Thirdly, there is an arbitrage opportunity in stable coins, because they are fluctuating themselves in value — even if they were meant to be “stable”. These price differences might be minimal but they exist — and this can be a business case if you happen to own lots of them.

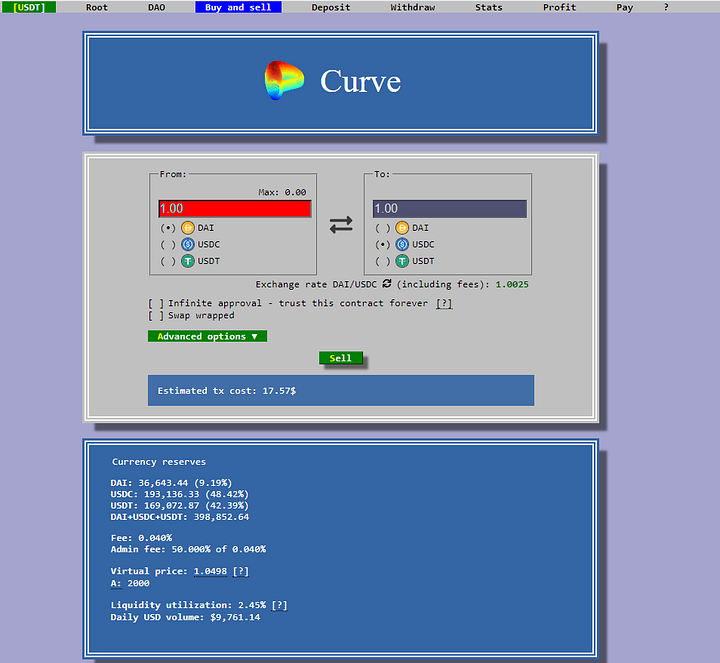

These opportunities brought very interesting new, specialized players to the DeFi market who only offer liquidity pools with the same kind of token. One of these interesting players is Curve.Finance with their retro-looking UI reminding me of my early days with computers. Have a look:

Curve might look funny and playful, but they handle serious amounts of money…at the time of writing 1.6 billion (!) $ deposits in 26 different pools — see here. They started simple, but quickly joint forces with projects like Yearn.Finance and Synthetix to create interesting offerings to swap all different kinds of stable coins and even create “synthetic ones” on top of their pools to minimize the risk you might have with holding just one certain stable coin. More on these kinds of cooperation later…

Please notice: Here, we don’t see trading pairs anymore. We often see pools of three or more tokens of the same kind, usually well balanced with a similar proportion of liquidity. There are incentives set in place to hold a certain balance in the tokens’ distribution. You might get better conditions if you provide liquidity with certain tokens that are underrepresented in those pools.

What’s really interesting is that Curve now does the same thing for different kinds of “Bitcoin on Ethereum”. Remember: You need an Ethereum compatible ERC20 token (nicely explained here) to be part of Ethereum’s DeFi space. So, that’s what different projects did for Bitcoin — in technically different ways. They created Wrapped Bitcoins ($WBTC) or established decentralized bridges between both blockchains like REN project with $renBTC or KEEP project with $tBTC.

The goal is again: Bring your $BTC “to work” instead of just hodling it. And Curve’s BTC pools come into play if you e.g. own $WBTC but want to swap it into e.g. $tBTC.

Curve had an “interesting” token launch in summer 2020. You can find more on that crazy and entertaining story here (highly recommended read — but please come back).

Curve was one of the early players (shortly after Compound) attracting a lot of capital with the decentralized launch of their governance token $CRV — which is used as an “extra incentive” for liquidity providers on their platform. More on that topic in the next chapter — let’s talk about farming to bring some more color into our “DeFi meal”…

Ingredient #4: Governance Tokens and Yield Farming

Photo by mali maeder from Pexels

Photo by mali maeder from Pexels

Tokens are at the heart of DeFi. They are used for many different purposes. If you e.g. invest into a pool on Uniswap, you’ll get back Uniswap LP tokens (LP stands for liquidity provider) for that respective trading pair. Ownership of these tokens are your proof that you provided liquidity to that pool. To get your assets back later-on you simply give back your Uniswap LP tokens to the smart contract and get back your original assets (usually in a different ratio — as explained in part 2).

But these LP tokens are just one part of the story. Many DeFi projects that initiated after the ICO hype in 2017 (Initial Coin Offering) started without their own token. Even the Uniswap DEX didn’t have a token until September 2020 — despite overtaking big centralized exchanges in trading volume. That’s a problem if you claim to be “decentralized” and act in this crypto-world. In the end, your community should have an important say in the further development of your DeFi platform. Earlier DeFi projects like e.g. MakerDAO or 0x project certainly had launched their tokens in the ICO era, collected funds and established their governance processes — handing over the main control over their projects to their respective communities.

So, these newer DeFi players needed to launch their own token and (maybe more important) to distribute these tokens in a way that was fair and credible (in the eyes of their community), compliant to relevant legal frameworks (SEC is watching you!) and — certainly — bringing in funds to push the project forward. You may sense it already: With these tokens the hype around DeFi “Yield Farming” really kicked off in the summer of 2020...

Photo by Samuel Silitonga from Pexels

Photo by Samuel Silitonga from Pexels

The first trigger was again Compound with the launch of their $COMP token, that was spread out into their community as an extra incentive for active users of their platform. Other DeFi players followed suite.

The complete narrative “how to launch a crypto project” changed this year:

First, have a product with actual users.

Then, launch your token.

This is a very different approach than these whitepaper-based ICOs in 2017. Compound’s token launch was such a success that - as mentioned above - projects like Uniswap got under a lot of pressure by their community because they hadn’t launched their own token in summer 2020. Uniswap even got attacked by Sushiswap — a team from their community who just copied Uniswap’s open source smart contracts, included their newly created $SUSHI tokens, launched their own platform and attracted liquidity away from Uniswap — before it soon came back once Uniswap launched its $UNI token. We speak about hundreds of millions of dollars that moved from Uniswap pools to Sushiswap pools (and back) in a matter of days…more on that little “DeFi war” can be found here.

You may ask: But how do these governance tokens work? And why should we care?

Photo by Artem Podrez from Pexels

Photo by Artem Podrez from Pexels

These governance tokens are usually at the heart of a projects DAO (decentralized autonomous organization). They are used to take important decisions like governing the future fee structure on the DeFi platform or their incentive regime. Usually it’s one governance token, one vote. If you own a significant part of these tokens you have a significant say in the future of the platform. That explains their high valuation.

But — with the arrival of governance tokens, crazy things started to happen. Projects got really creative to lure market participants onto their platforms to “earn” tokens and keep them involved. There have been many variants, but it usually works more or less down the following steps:

Photo by Leon Macapagal from Pexels

Photo by Leon Macapagal from Pexels

- Team collects Ethereum addresses of early active users on their platform like traders, liquidity providers, etc. (remember: we are on-chain — we have all the data 😎).

- Team mints their new governance tokens — reserve some tokens for investors and themselves, others for initial filling of liquidity pools (see below) and a good pot for the community (it is certainly worth while to investigate how big that pot is!).

- Team sets up liquidity pools for their new governance token and $ETH (and maybe $DAI).

- Team sends a part of the minted tokens out to the active community — or more clever: team makes the new tokens available to “be claimed” by these users (thus, users have to pay the gas fee to get them into their wallets).

- Team sets up kick-off incentives to motivate the community to “lock up” their tokens into the newly created liquidity pools (so you need their tokens AND additional funds in $ETH or $DAI. Sorry — again no “free lunch”). In return you get LP tokens — and maybe additional rewards in governance tokens for the first weeks. But remember impermanent loss. You now care for the further development of the token price…

- Team sets up an additional farming dashboard where you can now “stake” your LP tokens to get even more rewards (more governance tokens). Often, these rewards are initially locked up and get gradually released over a longer period of time. With this staking, you get (hopefully) long-term committed with this platform.

If you made it that far, you can call yourself a “yield farmer”! 🚀

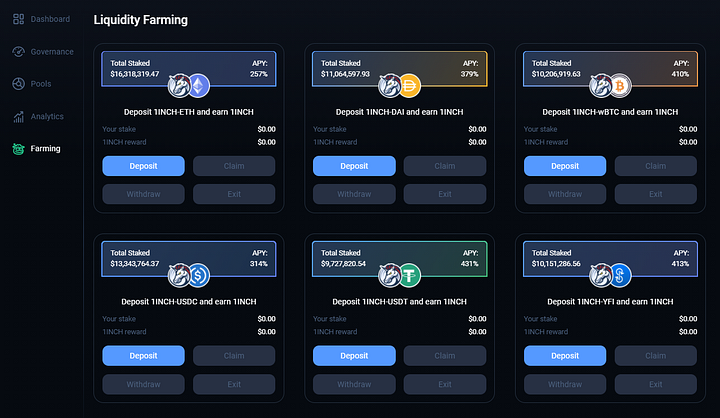

The 1Inch DEX just did exactly that over Christmas 2020. You can read their story here. It’s fresh off the press…just in time for my article.

Their new farming dashboard looks like this:

Screenshot of 1Inch’s liquidity farming

Screenshot of 1Inch’s liquidity farming

This kind of token release strategy is absolutely smart and has many advantages for the DeFi projects:

- Because they initially fill the liquidity pools, they determine the initial pricing of their tokens (usually quite high). [But they certainly need the other 50% of liquidity in $ETH or $DAI].

- They activate their community with these “airdrops” because they give away tokens “for free”. This certainly attracts a lot of media attention and hype around their project.

- Because users get additional incentives to not immediately sell their tokens, but rather lock them up and farm, the price stays very stable.

To give you an example: For Uniswap, this meant tokens worth above 1.000$ per user and an instant market capitalization of 200 m$ — which quickly rose to 800 m$.

As stated above, there are many different variants how projects play these incentive games. But the rough structure is always the same: You get something for free. And to get more of that, you need to stick with the platform, lock up your funds, bring some of your own crypto etc.

It is obvious that this process isn’t sustainable for very long. It’s great to kick-start a new platform, but you certainly need more if you want to be successful in the long-term. It will be very interesting to see how this all plays out. The competition for the best mid-term strategy is certainly heating up. Every week, you can watch something new. Liquidity moves heavily between all these projects. As you might imagine, it gets more and more complex to keep track on what’s actually going on.

Which leads us to the next point: How to mix all these DeFi ingredients together for the best DeFi meal we could imagine…

Mixing it all together: Synthesizers & Aggregators

Photo by Christiann Koepke on Unsplash

Photo by Christiann Koepke on Unsplash

Some people realized early on that it is quite hard to keep track with all these developments and shift funds manually to the projects with the highest yields. Instead, they wrote smart contracts to codify their investment strategy and regularly shift their investment to the project with the best conditions.

Andre Cronje, founder of Yearn.Finance, is one of those pioneers who got a lot of admiration and followers in 2020 (90k on Twitter). It’s amazing to read or listen to his story on Laura Shin’s Unchained podcast (highly recommended). Don’t be fooled: Yearn’s UI looks somewhat clumsy, its power lies under the surface…

Andre started with simple strategies to find the best yields on platforms like Compound or Aave. He gradually found better ways to integrate with more complex platforms like Curve. Over time, he created his own single-asset vaults to avoid impermanent loss, constantly maximize yields and automatically reinvest all incentives to further optimize yield.

Andre started to code different strategies for his own needs, but quickly realized that it is very beneficial to open up his code for a broader community. I don’t want to go down that route for now, but just mention one aspect that was eye-opening to me: He re-shifts his positions with every event when someone adds or removes liquidity from his pools or vaults. The more people get involved, the more often he can rearrange his strategy. And the best aspect is that in Ethereum you’re transaction cost doesn’t depend on the amount of money you move. That means:

If someone invests 10$ in one of Yearn’s pools and covers the transaction cost, Yearn can rearrange the other millions of their funds in that pool “piggy-back” in that single transaction. Imagine the efficiency of these systems!

A somewhat older, but similarly groundbreaking DeFi project is Synthetix. They create their own “synthetic assets” — derivatives for fiat money and different cryptocurrencies and also work closely together with many other DeFi projects like Curve. Synthetix created sETH and sBTC, which you might have seen in the Curve screenshots from above.

Total value locked in Synthetix is currently >1b$…

You see: there is literally no financial instrument from traditional finance missing in DeFi.

Enough for now…

I think, let’s call it a wrap for part 3 and this deep dive into the amazing parts of DeFi. I hope you enjoyed the ride.

I’m proud that you made it this far! 👍

In the meantime, I've published subsequent parts for this series:

- Part 1: How DeFi will innovate our financial ecosystems (Intro)

- Part 2: The rise of DeFi

- Part 3: The amazing parts of DeFi [this article]

- Part 4: The user's view on the DeFi jungle

- Part 5: DeFi opportunities for retail banks

- Part 6: DeFi lessons for Central Banks

- Part 7: Bringing it all together

...and I'm not finished yet...

Disclaimer: This article is not intended to be an investment advice of any sort. Do your own research and search for professional support if you intend to invest in one of the projects mentioned in this article.

Further reading: If you liked this story, you might also want to check out the start of this series or my earlier work about “Democratizing the digital markets” or “DeFi — an ecosystem made for whales?!?“

You are also welcome to follow me on Twitter or get in touch via LinkedIn (but please tell me your reason to connect and how you found me).