The rise of DeFi

In part 1 of this article series I introduced you to my personal macro view on Decentralized Finance and its possible disruption of the financial ecosystem. Now, let’s dive deeper. In this article we’ll work on the important question:

What makes DeFi so attractive and different?

The short answer is certainly: Its promise for “high yields”.

Photo by James Wheeler from Pexels

Photo by James Wheeler from Pexels

But while this sounds simple and plausible, I’m afraid the truth is more complex than many might think. That’s why I’ll give you some “historical context” about what actually happened in the last ~18 months up to the stage we are currently seeing (December 2020). You can read about all of that in many articles, but you’ll need to make your hands dirty and try out many projects to actually “get it” (…which I did) — so let’s go.

And to make it more entertaining and tangible, I’ll now break down the most important DeFi projects into different “ingredients” that play an important role in recent developments. We’ll then use these ingredients to create a delicious (yet complex) DeFi meal. So, let’s start our cooking session:

Photo by Maarten van den Heuvel from Pexels

Photo by Maarten van den Heuvel from Pexels

Ingredient #1: Borrowing and lending

It all started with the old idea of peer-to-peer (P2P) lending — now with a cryptocurrency-mindset and (as insiders would put it) in a permission-less fashion. There have been many players trying to do that with fiat money, their success was limited.

You might ask:

Why should cryptocurrencies be more successful with P2P lending approach?

Short answer: Tokens and a lot of fantasy!

Many early investors of cryptocurrencies like Bitcoin ($BTC) or Ethereum ($ETH) are “hodlers” (why hodl instead of hold? See here) . Hodlers tend to hold their crypto investment over a (very) long time-frame to see it appreciate in value — hence the name. In reality, it can be quite challenging to be a holder…

- not selling in bull-runs like 2017 or 2020 when prices go up dramatically.

- not selling in bear markets (2018/2019) when all hope seems lost.

(On top, sometimes it’s kind of boring — just sitting and waiting what happens to your funds.)

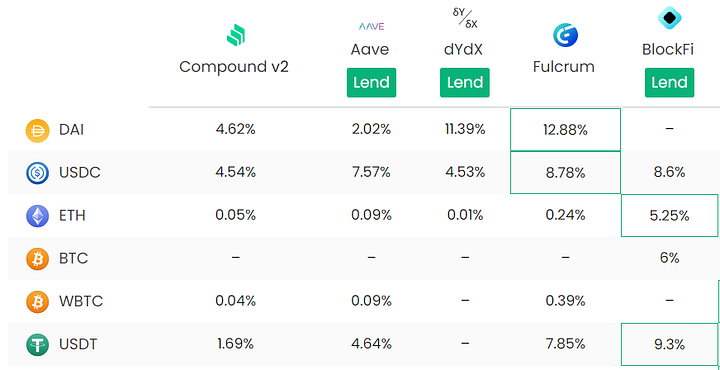

So, some DeFi projects started to innovate around putting your “crypto to work” through lending. Usually someone else (a borrower) takes the action. You are certainly putting your savings at a certain risk here (more on that later). In return, you get rewarded with a substantial (but usually fluctuating) yield. These projects sometimes reach impressive interest rates — check current rates here or see screenshot below.

DeFi interest rates (snapshot from https://defirate.com on 2020–12–25)

DeFi interest rates (snapshot from https://defirate.com on 2020–12–25)

Projects like Aave (formerly known as EthLend — the name says it all) and Compound have built their solutions exactly on top of these principles: You can deposit (lend) your crypto funds into pools (governed by a smart contract “on-chain”). Other users borrow these assets and “work with it” (e.g. by trading). These early DeFi players obviously investigated financial instruments form traditional finance and came up with their very own crypto variant.

Another interesting player in that field is MakerDAO — one of the pioneers for stable coins — with their Oasis app and stable coin $DAI. $DAI is a crypto “pure play” stable coin — no fiat money involved. $DAI is pegged to the US dollar, but not backed by fiat money. Instead it works similarly like the lending protocols above, with you lending and borrowing at the same time: You deposit your crypto to borrow/mint $DAI. Then you put that $DAI to work by e.g. putting it into Compound earning yield. If you want to dive deeper into MakerDAO, you could start here. If you want to get an idea about the overwhelming spread of MakerDAO alone in the ecosystem, I would suggest to have a glimpse here.

As you see:

These different projects obviously compete with each other, but they also work closely together. This coopetition is DeFi’s secret sauce and explains its tremendous innovation speed.

That’s also why the DeFi ecosystem is tenderly named Ethereum’s “money legos”. The sum of these projects is much more than their parts.

Picture by Alexandra_Koch on Pixabay

Picture by Alexandra_Koch on Pixabay

If you take the example above: With the launch of Compound v2, you get $cDAI tokens (explained here) in return for every $DAI token you put into Compound. You certainly need your $cDAI to claim back your $DAI later on — but in between you can put your $cDAI “to work” in other DeFi projects — e.g. trade it. The possibilities are literally endless.

But hold on — this is just our first ingredient and the very start into our big DeFi puzzle!

Ingredient #2: Automated Market Makers and Liquidity Providers

In traditional finance, we as users are simply working with a system that is set up by professionals. One important role in these systems are so called “market makers”. In layman’s terms, market makers are payed to “keep the financial market running” — even in situations when nobody wants to take an offer for a trade. These market makers might be humans — but usually these are bots programmed to keep the market running. They might make a loss with certain deals but all-in-all they still earn some margin. Centralized crypto exchanges (like Binance, Kraken or Coinbase) work with market makers very similar to traditional finance.

In contrast, decentralized exchanges (DEXes) started to try different paths with Automated Market Makers (AMM): Smart contracts that codify how trades are handled and prices get determined. Relatively simple and deterministic(!) code replaces the traditional “market maker”.

Photo by Digital Buggu from Pexels

Photo by Digital Buggu from Pexels

Here’s how that works: These DEXes usually work with token pairs and create a liquidity pool for each trading pair (e.g. your favorite token with $ETH or your favorite token with $DAI). If there is enough liquidity in a DEX liquidity pool, then you can trade tokens at a “fair market price”. If demand wanders towards one token and you want to buy it, then you’ll have to pay a higher price (usually defined by a “bonding curve”). You’ll experience more or less price “slippage” depending on the size of the liquidity pool.

This has some interesting effects: In pools with low liquidity each trade affects the price considerably. In practice, it might be wise to avoid big trades and rather break it down into several small trades and wait until the price “recovers”.

You might wonder:

- How could a price "recover" in such a fixed, rather deterministic system?

- How can someone trick that bonding curve?

Well, while this mechanism is very clean and simple — real world is certainly more complex. DEXes are not alone in the market. They are set up in a way that there is always motivation for market actors to align the DEX’s price with that of the broader markets through arbitrage: by either selling, or buying certain tokens because of better prices in other markets like centralized exchanges or other DEXes. Remember: Tokens are free to move (hence again like already mentioned in part 1: they are the decisive factor making all that possible).

While DEXes usually run completely “on-chain”, centralized exchanges and their order books run “off-chain”. If you want to access their prices you need to access “off-chain” data. If you want to do that automatically via an algorithm this is very tricky and critical because of potential price manipulations. In this context, you’ll read a lot about “oracles”.

Picture by christian hardi found on Pixabay — Delphi in Greece — famous for its oracle

Picture by christian hardi found on Pixabay — Delphi in Greece — famous for its oracle

Oracles in blockchain terms are gateways to get data from “off-chain” available to our “on-chain” smart contracts — in this case the DEX’s smart contract. I don’t want to go down that route for now. Just remember: Oracles are potentially dangerous and bear enormous risk. Whole projects like ChainLink try to tackle this problem space (you might already guess it: again via decentralization).

The other very cool and decisive aspect with DEXes is that every market participant can provide additional liquidity (at the current rate) — and remove it at any later time (at the current rate at that point in time).

It’s — again — a permission-less system. You are the system (not just the user).

And here we see the similarities to the lending examples from above. Instead of “lending in general” you trust your crypto assets with a specific liquidity pool of a DEX. You become a liquidity provider. Why would you do that? Well, you certainly get incentives: DEXes work with trading fees. And you’ll get a small percentage of each trade. Speaking for Uniswap (one of most prominent DEXes at the time of writing) this is currently 0.3% (proportional to your share in the liquidity pool).

The beauty of these systems is their extreme transparency. Let’s make an example and take the $DAI/$ETH pool on Uniswap. Please take the time and have a look here. You can easily see and analyze liquidity, trading volume and generated fees. But you can also see who trades what. Remember: we are on-chain. We can easily analyze single transactions like this one — someone just added $DAI and $ETH worth ~20.000$ to that pool. But we can also have a look into Uniswap’s smart contracts. This one (UniswapV2Pair) is from 2020–05–05.

Attributes like openness, transparency and clarity — mixed with low trading fees — brought the success to DEXes like Uniswap, Kyber, Balancer and Bancor.

One more thing: Openness on DEXes doesn’t end at providing liquidity.

You can even create your very own trading pair.

You just need to provide liquidity and there you go.

Fascinating, isn’t it?

Many new crypto projects now use this mechanism as an “on-ramp” to launch their tokens. Instead of paying high fees to list them on a well-known centralized exchange, they rather provide liquidity on Uniswap to kick-start their tokens. This is certainly no free lunch, because you always have to bring both tokens to a Uniswap liquidity pool. So, if you want to make your new token trade-able against $ETH — you also need to bring $ETH to the table.

Caution

I think it is important to speak about one dangerous aspect with providing liquidity into trading pairs on DEXes. While it all sounds very simple you are risking impermanent loss. The reason: Prices of cryptocurrencies fluctuate. This means the ratio of your trading pair will move up or down. That means you usually won’t get back the exact same ratio of both assets as you provided liquidity in the first place. You’ll usually see a disadvantage over just hodling your assets separately. This effect is called impermanent loss since you could theoretically wait until the ratio meets again to your entry criteria —but: you could wait forever. It is crucial to understand this dilemma before you take any action. I recommend this fantastic video from Finematics. They are doing a great job in explaining complex stuff like that visually:

Impermanent loss is — in my eyes — one of the major driver in DeFi innovation since summer 2020. Projects try to tackle that risk in various innovative ways.

Balancer attacks these three aspects:

- They eliminate the 50/50 distribution enforced by Uniswap’s trading pairs. Instead you can go for 80/20 pools when you are more bullish on one token over the other.

- You can add/remove liquidity for only one token in a pool.

- Balancer even enables pools with more than two tokens.

This works similar to TokenSets who design pools that resemble indices in traditional finance like their DeFi Pulse Index with the 10 most prominent DeFi tokens (from their point of view).

But it gets even better: Bancor used its latest upgrade (v2.1) to let you invest in one side of a pool and even gradually “insures” your assets against permanent loss. After some time period (currently 90 days) you can be sure to get all your funds back (if the system works as intended). Let’s see how this works out in practice — it’s still in beta. But I’m sure: Features like these show the way into the future.

👉 Are you still with me? 😎

I'm just recognizing that we’ve already come a long way and covered a lot of “DeFi ground”. I promised to keep it entertaining and digestible — so maybe it’s time for a break. We obviously didn’t prepare our complete DeFi meal yet. So, let’s have some quick snack in between before we continue…

Photo by Kampus Production from Pexels

Photo by Kampus Production from Pexels

In the meantime, I've published subsequent parts for this series:

- Part 1: How DeFi will innovate our financial ecosystems (Intro)

- Part 2: The rise of DeFi [this article]

- Part 3: The amazing parts of DeFi

- Part 4: The user's view on the DeFi jungle

- Part 5: DeFi opportunities for retail banks

- Part 6: DeFi lessons for Central Banks

- Part 7: Bringing it all together

Disclaimer: This article is not intended to be an investment advice of any sort. Do your own research and search for professional support if you intend to invest in one of the projects mentioned in this article.

Further reading: If you liked this story, you might also want to check out the start of this series or my earlier work about “Democratizing the digital markets” or “DeFi — an ecosystem made for whales?!?“

You are also welcome to follow me on Twitter or get in touch via LinkedIn (but please tell me your reason to connect and how you found me).