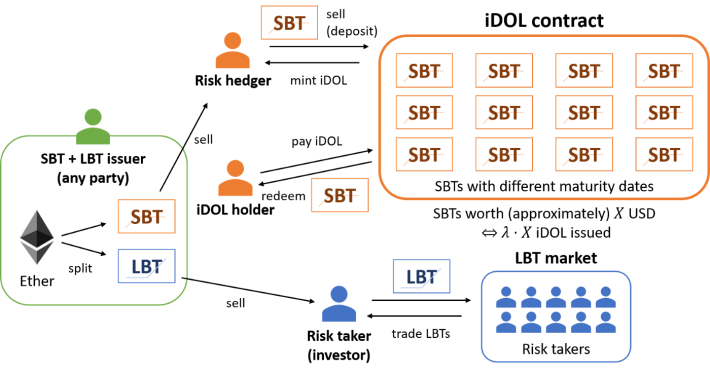

Lien was recently announced (white paper dated April 1st, 2020) DeFi project which describes a new stablecoin mechanism where Ether (ETH) is sliced into two tranches of derivatives — Solid Bond Tokens (SBTs) and Liquid Bond Tokens (LBTs). LBTs absorb the exchange-rate risk associated with the market (fiat) value of Ether, making in turn the price of SBT stable. The stablecoin itself is the iDOL token which is backed by and issued in return of SBTs.

The system is constructed in two steps — first, the two classes of derivatives are introduced (the SBTs and LBTs), whose corresponding tokens are generated by splitting/"tranching" Ether (ETH). On the maturity date, the derivative contract returns a fixed dollar amount to the SBT holder and the remaining (if any) amount to the LBT holder. That way nearly all the exchange-rate risk is absorbed by the LBT holder in minimizing the volatility of the SBT token.

Flows of Ether (ETH), SBTs and LBTs. Source: White paper.

Second, a basket of SBTs with various maturity dates is put together and the iDOL token is developed as a stablecoin backed by the basket. Anyone can deposit SBTs to an iDOL contract and receive a proportionate amount of iDOL tokens. iDOL is a representative money in the sense that its value is backed by a basket of SBTs held by the iDOL contract. The value of each SBT remains stable as it is part of “senior tranches” within the system and (almost) all the price volatility of ETH is absorbed by the LBT which is paired to the SBT. In this way, a fiat exchange rate of the iDOL token is kept stable.

Rather than requiring overcollateralization, one can simply provide SBTs as stable-value collateral for the exact corresponding amount of iDOL in return— it's this“exact-collateralization” that makes the iDOL token reliable representative money. The scheme can also provide a pegging mechanism for many other assets as well.

The white paper explains the derivative contract implementation thus:

The derivative contract will be implemented in the following fashion. First, Q ETH is deposited to a smart contract for the issuance of the derivative tokens. The smart contract then returns two tokens, the Solid Bond Token (SBT) and Liquid Bond Token (LBT). We will then peg the value of SBT to K USD. Now, let P0 be the USD/ETH exchange rate on the issuance date and P1 be the exchange rate on the maturity date. The USD/ETH exchange rate, a proxy for the peg will be provided by a reliable oracle (e.g. ChainLink). Upon maturity, the smart contract returns min{K/P1, Q} ETH to the SBT holder and returns the rest of the deposit, or Q − min{K/P1, Q} = max{Q − K/P1, 0} ETH, to the LBT holder.

And the use case/utility of the LBT token/derivative:

In contrast, if you want to speculate on the changes in the exchange rate, you can use LBT and capitalize on its volatility. Note that, as long as the rate is higher than K/Q, the LBT holder takes all the risks. We expect a demand for LBT from investors who wish to speculate on the price development of Ether. LBT is riskier than holding Ether because its value becomes zero when the exchange rate goes below the threshold (K/Q). An investor can engage in leveraged trading by holding LBTs and, unlike leveraging through debt-finance, he does not have to provide a collateral to conduct the leveraged transaction. Hence, there is no margin call even if the exchange rate falls.

Given a large number of speculators in the cryptocurrency market, we could expect a reasonably high demand for LBT. At the same time, the demand for SBT will also be large because people can use the token as a hedge against the exchange-rate risk. We can therefore expect people with diverse risk profiles to generate many SBTs and LBTs by putting on Etheras collateral. LBT will be traded as a class of liquid speculative assets on various platforms such as cryptocurrency exchange platforms while SBT will be utilized as a component for our stable coin.

Personally, am not yet quite clear as to the details of how all this works in practice/production, but it does sound like an interesting idea worthy of further consideration...