Over the last 70 years, financial services have changed beyond recognition.

High street banks are being replaced by online-only banks.

Savings accounts are giving way to loan investments.

Fred, the financial advisor who told you the best way to safeguard your dollars and euros, has been replaced by AI-driven programs that tell you how to invest your crypto.

But how did things change so much and what happened along the way? Let’s follow our time-traveling couple – Mr and Mrs Smith – as they discover the small steps, big jumps and giant leaps that have been made in finance over the last 70 years.

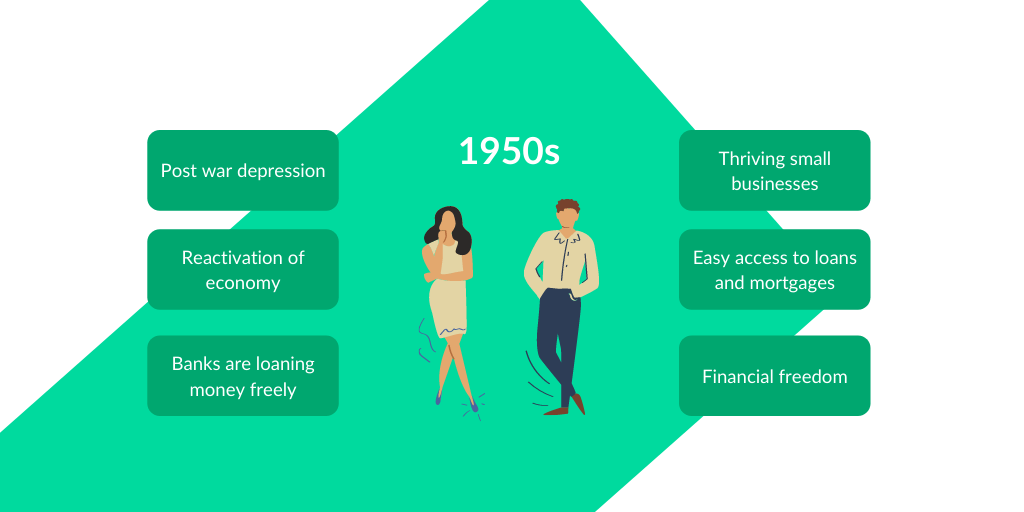

Finance in the 1950s

It’s the 1950s, America and much of Europe are rising out of a depression. A post-war economic boom is on the horizon and, for the first time in a long time, people are looking to the future with real hope.

Small businesses are thriving and banks are loaning money freely, giving people a chance to create their own financial freedom.

With the Wall Street Crash of 1929 and the Great Depression of the 1930s still echoing in the air, the public has no mood for taking risks financially. Overseas investment is still a long way off and stock prices are pretty hard to get hold of.

So, instead of investing money, people are saving.

Our time-travellers, Mr and Mrs Smith, have just tied the knot. The Smiths have started their own business and are looking to buy a house. They were able to get a loan and a mortgage from the bank – the process was simple, as regulations are loose and the bank was more than willing to lend money to stimulate the economy.

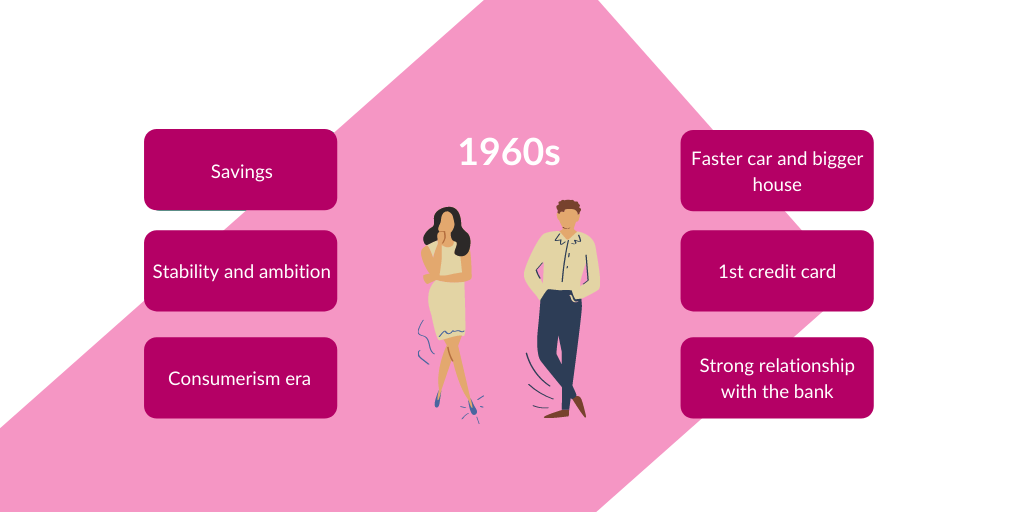

As the decade goes on, the Smiths’ business starts to grow and they save more and more money. With stability, comes ambition. Like their next door neighbors, Mr and Mrs Jones, the Smiths want more. They want a faster car and a bigger house.

They want one of those new color TVs.

Ah yes… the age of the consumer. Mr Smith is now a big successful self-made businessman and wants to spend the money he’s earned. In fact, he’s just been approved for a new kind of club. His membership just came in the post – it’s called a Diner’s Card.

It means he can take Mrs Smith to fancy restaurants and not have to pay cash. Instead, every time the Smiths go to a restaurant, they just flash their Diner’s Card and pay later. At the end of the month they pay the total.

Ladies and gentlemen… the first credit card.

Financial services in this era are all about face to face interaction. Your bank manager knows Mr and Mrs Smith by name and wants to build a relationship with them. A relationship built on trust. Still, there’s something not quite right about him...

Key points to take away from finance in the 1950s:

- In the 1950s, the US economy grew by 37%.

- By 1960, the Smiths had 30% more spending power than they did in 1950.

- After living on the bare necessities for two decades, the Smiths were ready to party. They spent, spent and spent some more. TVs, fridges, cars, music, dining out, booze and more.

- They didn’t also pay straight away. This was the age of ‘buy now, pay later.’ After getting his Diner’s Club card in 1950, by the end of the decade Mr Smith got himself an American Express charge card.

- Borrowing brought private debt up $150 billion from what it was at the beginning of the decade.

- Financial services were based on close relationships – personal trust was a big part of the deal, although, as we’ll see later, it might not have been genuine trust.

Finance in the 1970s–1980s

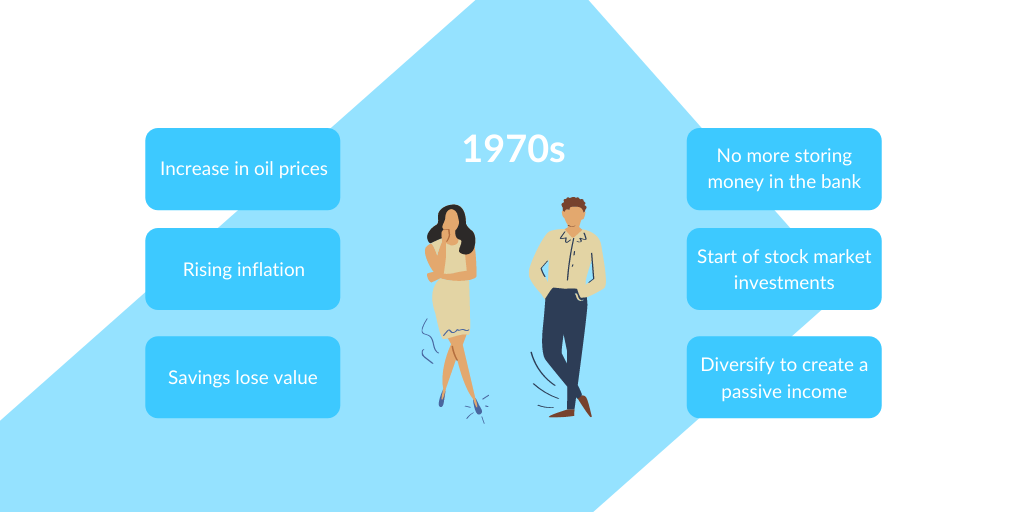

It’s 1970 and banks are losing their place at the center of the financial world. Federal restrictions are making it hard for them to compete. Also, rising inflation – due to a massive increase in oil prices – means that people with savings accounts are losing lots of money.

Up until now, Mr and Mrs Smith had been cruising. They had a nice little savings account and the interest rates were good. But now, with prices of goods and services going through the roof, their savings are losing value.

But Mr Smith has an idea. He heard the next door neighbor, Mr Jones, talking about something called a ‘no load investment fund.’ So Mr and Mrs Smith decide to find out more.

Instead of saving in a savings account, the Smiths decide to pool their assets into investments. They buy shares, which are distributed by the investment company – without a second party involved. This means there’s no sales charge or commission fee.

It’s not just the Smiths though. At this time, Americans are deciding to invest money, rather than store it in the bank – between 1977 and 1981, investments in mutual funds rise from $3.9 billion to $181.9 billion.

The Smiths also decide to set up a portfolio of stocks from something called an index fund. They diversify their investment, with an idea to create a passive income and make their money work for them.

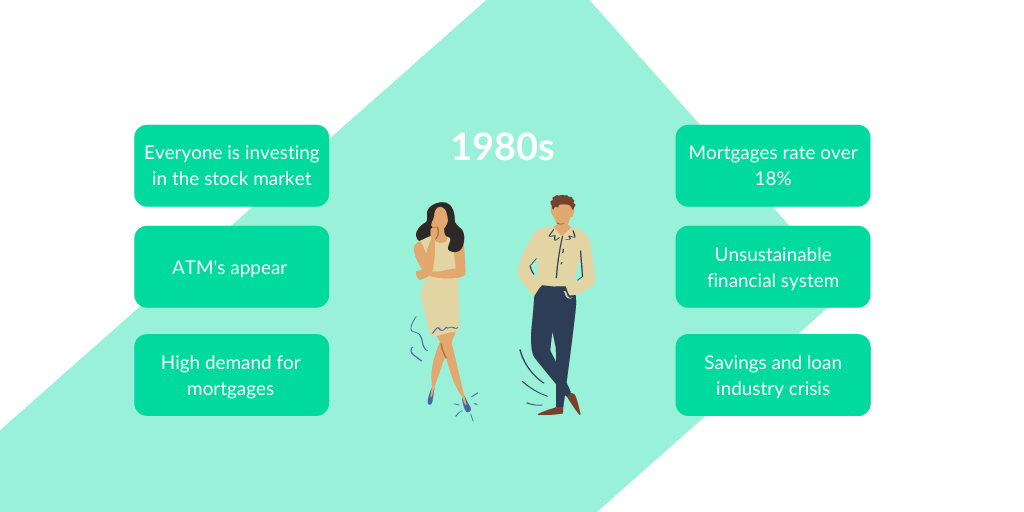

The way Mr and Mrs Smith get hold of cash is now totally different. Before, they’d have to wait in line in the bank, then receive the money from a bank teller. Now, ATMs (automatic teller machines) are everywhere. As the 1980s approaches, with money on the rise and patience on the decline, ATMs are a godsend.

The Smiths are looking to get a mortgage for a new house. Mortgage demands are huge, more than the supply. This means there’s a queue to get a mortgage.

By the end of the decade, major changes are also taking place in the Smith household. Perhaps the biggest change – aside from Mr Smith’s new ‘mullet’ hairstyle – is the way the Smiths are making money.

Keen to stay ahead of the inflation curve (not to mention ahead of Mr Jones, the next door neighbor), Mr Smith is on board too. He’s playing the stock market. And he’s making an absolute killing.

It’s August 1982 and the Dow Jones has risen 10% in just a week. Everybody is now investing in the stock market. Banks and traditional financial services are losing out to investment companies and the stock exchange.

It’s a good thing Mr Smith is making money on the stock market, because Mr and Mr Smith have finally got their mortgage and bought a new house. Mortgage rates are now over 18%!

But it’s the ‘get rich quick’ era. Credit card use is going through the roof – Mr and Mrs Smith have eight credit cards each and are borrowing like there’s no tomorrow.

At the end of the decade, the effects of deregulation and free enterprise are laid bare. The savings and loans crisis has hit and the saving and loans industry, which was riddled with fraud and corruption, is bailed out for $159 billion.

Also, financial services are now digital. Everything is becoming simpler and easier. Technology is about to completely reshape financial services forever.

Key points to take away from finance in the 1970s–1980s:

- By 1979, prices were on average 98% higher than they were in 1969.

- ATMs became hugely popular in the 1980s. Instant cash withdrawal completely reshaped the simple act of withdrawing money.

- In just four years, at the end of the 1970s and beginning of the 1980s, investments in mutual funds rose from $3.9 billion to $181.9 billion.

- By 1989, banks held just 26% of all the American population’s assets, down from 34% in 1960.

- The savings and loans crisis in 1989 was the first big indication in the modern era of how fraud and corruption would lead to an unsustainable financial system.

- By the late 1980s, financial services had become mainly digital.

Finance in the 1990s–2000s

It’s the 1990s and the diversification of financial services is in full swing. In decades gone by, if you wanted to borrow money you’d go to a bank. If you wanted insurance, you’d go to an insurance company. If you wanted to invest, you’d approach an investment company.

Mr and Mrs Smith want to do all those things and more. Instead of going all over town, from place to place, they can now go to just one company. In the 1990s, there’s a surge of companies offering lots of different financial services under one roof.

By now, technology is completely changing the financial landscape. Mr Smith, once again listening over the garden fence, hears his next door neighbor Mr Jones talking about something called the ‘Internet.’ A few weeks later, the Smiths have an internet connection.

While it takes ages to connect and Mrs Smith keeps complaining about a funny noise when she picks up the telephone, Mr Smith is soon investing money through a new thing called ‘online investment services’ or ‘e-commerce.’ Mr Smith doesn’t know it yet, but he’s at the forefront of the birth of FinTech.

Credit cards are even more popular than ever, with a seemingly endless number of cards offered to consumers. Paying cash for goods is becoming less and less frequent – Mr and Mrs Smith nearly always ‘stick it on the credit card.’ Digital money is here to stay.

The merging of two giant companies from different sides of the financial system sees the beginning of a new era. Citicorp (a commercial bank) and Travelers Insurance (a financial services company) shake hands on a $70 billion deal and merge in 1998. They form a new company called Citigroup. The infamous merger ushers in an era of deceit, treachery and fraud on an unprecedented scale.

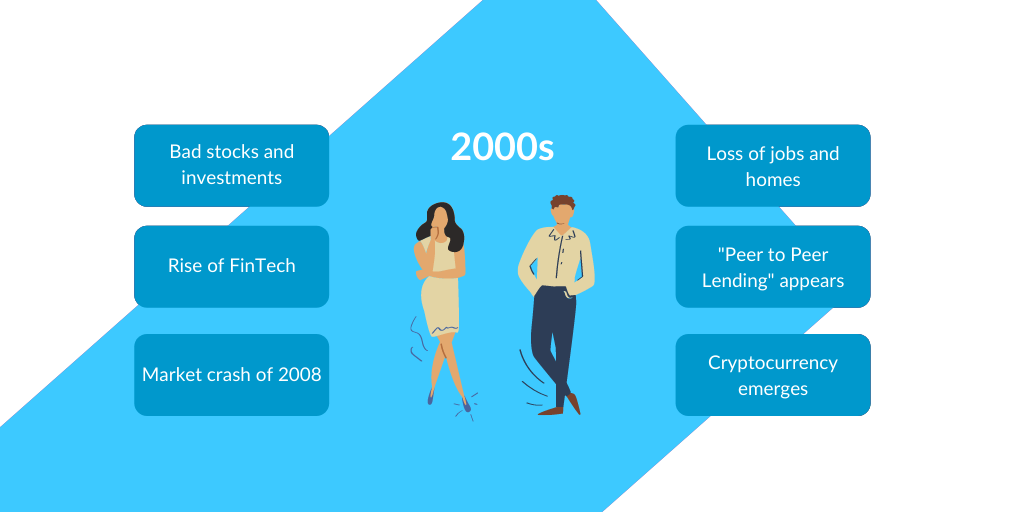

Over the next ten years, Wall Street is given free reign. Bad stocks and investments are sold at a rapid rate. Still, with the rise of FinTech, consumers are enjoying more efficiency, less bureaucracy and less waiting around. Everything is faster and the machine is running like clockwork. But the machine is about to break down.

The market crash of 2008 is the biggest financial disaster since 1929. Millions of people lose their jobs in the US as well as their homes. Trust in the traditional financial system hits an all-time low and people start to look towards new systems of finance.

After lots of reckless speculation on the stock market before the 2008 crash, Mr Smith loses a lot of money. Luckily, Mrs Smith starts to spend her nights on the internet, researching new forms of finance.

She signs up to a robo-advisor and begins to reorganize their investment portfolio through an easy to use, intuitive online interface.

She also looks into a new form of currency known as crypto, which is starting to make waves in tech communities around the world.

While Mr Smith is stashing money under the mattress, cursing “those lying thieving banks”, Mrs Smith discovers a new form of investment known as ‘peer to peer lending.’ She starts to slowly invest money in small businesses, rebuilding the money Mr Smith lost in the 2008 crash.

As cash money becomes less and less used in everyday life, contactless payment – a new innovation – is starting to take hold.

Key points to take away from finance in the 1990s–2000s:

- The digital era was in full swing and most financial services became digitalised, meaning a faster, more efficient customer experience.

- The diversification of financial services truly began, as companies looked to dominate every area of finance rather than specialize in one.

- The market crash of 2008 caused public trust in traditional financial services to plummet.

- New online financial services – such as robo-advisors and peer to peer lending, emerged out of the rubble of the 2008 crash.

- A new form of currency known as cryptocurrency emerged.

Finance from 2010 to 2020

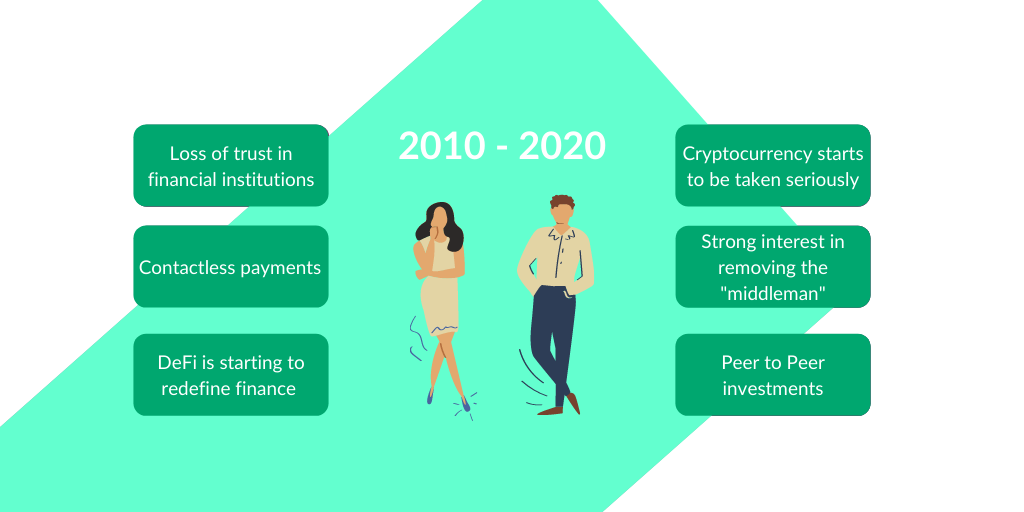

In the wake of the 2008 crash, the financial system starts to change radically. The consumer experience is almost unrecognizable compared to just a few decades before.

While Mr Smith is frantically cutting out coupons in an effort to save money, Mrs Smith has other ideas. She’s learning more and more about FinTech. Soon, she’s using her new smartphone to pay for goods and services, as well as budget for weekly purchases.

Eventually, all the financial services she uses are accessed through her smartphone. Then, one day, while having a coffee with the next door neighbor Mrs Jones, Mrs Smith learns about DeFi.

Before long, more and more people are taking the idea of decentralized finance seriously. A new system that promises to do away the old tired financial services, DeFi starts to change finance on a fundamental level.

Cryptocurrency – a new form of currency that didn’t rely on centralized governments – starts to be taken seriously. More and more people begin to trade in crypto, as a greater number of coins becomes available.

Built on the revolutionary technology of blockchain – an open-source network that enables anyone in the world to collaborate – the new system creates a secure financial ecosystem, where innovative products are produced every day. Transparent, traceable and trusted, it’s a new form of finance that completely removes the middleman.

By now, Mrs Smith has built a diverse investment portfolio, including peer to peer investments. She has made connections with new businesses in emerging industries, putting her money into causes she cares about and making great returns at the same time.

Meanwhile, Mr Smith hears Mr Jones talk about a great new pyramid scheme…

Key points to take away from finance in 2010–2020:

- The effects of the 2008 crash were catastrophic for traditional finance. After a decade of giving their trust to banks and traditional investment services, consumers decided that their money wasn’t safe with these archaic institutions.

- As contactless payments and online finance became a part of everyday life, the revolutionary potential of FinTech started to be realized.

- Cryptocurrency gained greater traction, as governments around the world started to recognize it as legal currency.

- Peer to peer lending and other new forms of investment started to replace outdated forms of investment.

- DeFi – the decentralization of finance promised to revolutionize everything.

Finance – the future

With a profit decline of 20-60% predicted for legacy finance over the next five years, it’s clear that the old systems are very much on the way out. The DeFi wave is in full crest and the old corrupt financial models will soon be swept away forever.

Automation and AI will be the biggest drivers of financial services in the future. While Mr Smith is wondering what went wrong with his failed pyramid scheme, Mrs Smith will be making investment choices based on complex data-driven algorithms. New platforms will be offering services in the blink of an eye and they’ll all be decentralized.

Money won’t be controlled by a centralized institution – instead it’ll be created and regulated on the blockchain, as FIAT currencies all but disappear. The new financial ecosystem will seamlessly spread around the globe, giving everyone the chance to control their own financial lives.

The days of large greedy institutions taking a huge percentage of people’s money for doing next to nothing will be long gone.

And Mr Smith will stop trying to keep up with the Joneses. Instead, he’ll join his wife in learning about the DeFi revolution.