The Federal Reserve System

What is the Federal Reserve System? The Federal Reserve System (will refer to as Fed from here on out) is a carefully planned out, intentional, calculated, and malicious strategy used to progressively shift wealth from working-class citizens to the most affluent people on the planet. It is an organization run by unelected officials with unlimited and centralized power to control the United States economy. The people who started this organization were not dumb, they were among the wealthiest and most powerful people in the world and their plans to form a financial cartel would propel them to have control over the wealth of foreign nations, corporations, small businesses, and working-class citizens whose largest concern is how they will pay their bills or feed their family. Many people have not heard of the Fed, or they have no idea what they are capable of. Yet, this organization has by far the largest impact on your everyday life, far greater than the company that produced the phone you look at every day. It cannot be overstated how important it is that we understand the Fed and its capability to affect global and domestic occurrences and create phenomena that no one has experienced before. The fed will be mentioned often from this point forward because of the large impact it had on the world in the 20th and 21st centuries, and in plain speak is the biggest scam in American history.

(1913 newspaper front page discussing the creation of the Fed)

When we discuss the Federal Reserve, we need to talk about important financial and political figures that had significant influences on the creation and extension of the system. We are going to talk about its creation, then some basic facts, and finally, finish up with the impacts the Fed had not only on the United States but the entire world.

The Fed was established on December 23, 1913, two days before Christmas through the Federal Reserve Act, and had overwhelming support from the Senate and the House. However, we must rewind to 1910 and look at when the Fed was first conceived, in Jekyll Island, to get a complete picture of the situation. Jekyll Island is a piece of land on the coast of Georgia that served as a private and secluded getaway for the wealthiest businessmen in the world who sought to get away from the media frenzy in New York. In 1886, the island was bought out and turned into the Jekyll Island Club, which consisted of members such as the Morgans, Rockefellers, Vanderbilts, and other infamous entrepreneurs. In November 1910, a meeting was called by Republican Senator Nelson Aldrich that requested the United States' most powerful leaders to send representatives to a secret meeting.

(Rockefeller’s Jekyll Island ‘Cottage’)

Nelson Aldrich was one of the four most influential republicans in the senate and was appointed to become the chairman of the national Monetary Commission with the goal of reforming the banking industry after the Panic of 1907 and the country needing to be bailed out by J.P Morgan (Lewis Gould, The Most Exclusive Club). When the National Monetary Commission was tasked with creating legislation to reform the banking industry in the United States, it was kept secret from the public that the organization would rely on the richest bankers in the world to come together to restructure the banking system. Aldrich was well connected with the elite of the country. His daughter was married to Rockefeller Jr., therefore, making him the father-in-law of a Rockefeller and he had important connections on Wall Street in New York. When Aldrich called the meeting, he requested that the financial leaders come in secret, at night, under disguises and with fake names so as not to rise the interest of the press or the government or would be curious about a meeting with the world’s most important financiers. The meeting would last one week where the Money Changers would carefully craft a manipulative plan that would slowly concentrate wealth and power into the hands of the elite.

Among those Aldrich called to the meeting were A.P Andrews, who was the Assistant Secretary of the Treasury Department. Frank Vanderlip, was president of the National City Bank of New York. Henry P. Davidson, a senior partner at J.P Morgan. Charles Norton was also part of the First National Bank of New York. Benjamin Strong, who was representing J.P Morgan’s company. And Paul Warburg, representing Kuhn, Loeb and Co. Now let’s break down these important characters.

We have previously discussed Aldrich who was bestowing Rockefeller's interest as he was part of his family and took it upon himself to use his role in being one of the most influential politicians in congress to push forward the issue.

Frank Vanderlip was president of the National City Bank of New York, or what would become Citibank, and was owned primarily by J.P Morgan and had been the banker for Standard Oil and the Rockefellers. It was one of the major institutions that stepped up to loan money to the government in the Panic of 1907 and after the Federal Reserve Act was passed was the first bank to begin opening international offices, where they began overseas in Argentina in 1914 and quickly expanded to other areas around the world.

(Frank Vanderlip. President of Citi Bank from 1909-1919)

Charles Norton was the former Secretary of the Treasury and Secretary to President William Taft before leaving the white house and joining Citibank. In addition, he was a trustee at companies like Equitable Life Insurance, AT&T, American Express, and others.

(Norton at a Red Cross Luncheon in 1917)

Henry Davidson was a senior partner at JP Morgan and Company and became a chairman of the Red Cross during World War I while pushing for the League of Red Cross Societies, which is a centralized international organization with a huge bureaucracy focused on raising money for natural disasters. The key part there is raising money.

(Henry Davidson Sr.)

Benjamin Strong Jr. was a president of the Bankers Trust and was working as an agent of J.P Morgan. Strong would go on to serve as the first President of the Federal Reserve Bank of New York, which is far and away the most powerful division out of the 12 Fed branches. Strong would serve as a Governor of the New York Fed until 1928.

(Benjamin Strong Sr. Governor of Federal Reserve Board from 1914-1928)

Paul Warburg was part of the powerful Warburg family who immigrated from Hamburg Germany and was a naturalized US citizen. Paul Warburg became a partner at the family banking firm of Warburg and Co. and married the daughter of Solomon Loeb, who created the investment bank Kuhn, Loeb and Co. When Paul Warburg finally stayed in the United States in 1902, he was already a leading partner at Kuhn, Loeb and Co. and was a senior partner with Jacob Schiff. Paul Warburg’s brother would go on to marry Jacob Schiff’s daughter, making the family ties even stronger within the bank. In addition, Jacob Schiff had close relationships and acted as the financial agent for English and French Rothschilds, as Schiff’s father had been the Rothschild's broker for years.

(Paul Warburg)

In February 1910 Paul Warburg became a director at Wells Fargo and Company, an investment bank created by Henry Wells and William Fargo in 1852 who also founded American Express in the same year. This bank flourished under the California Gold Rush and was an important contributor to the United States in World War I. Warburg would go on to resign from Wells Fargo in September 1914 when he was appointed to the Federal Reserve Board, and Schiff would take his spot at Wells Fargo (Noel M. Loomis, Wells Fargo, pp. 311, 315). Warburg would be appointed to be the 2nd vice chair of the Federal Reserve from 1916-1918. Warburg was among the most important and biggest advocates for creating a central bank in the United States that was derived from his experience with European Central banks, but the members at the week-long meeting had to come up with a carefully crafted and incredible plan that would win over the hearts of politicians and Americans without showing how similar they were to the centralized forces in Europe because of Americans desire for ingenuity.

The name of the Federal Reserve System was chosen carefully given as an illusion to Americans that this institution was created for their benefit. First, the Federal Reserve is not a federal institution. It operates independently from the government. The members, board, or directors are not elected and the extent to which they are accountable to the public is through congressional testimony that occurs occasionally throughout the year but is only used as a partisan tool for representatives to convince their constituents they are in control, they are not. The Federal Reserve does not have a reserve. It is not a bank; it has no reserve requirements and you can’t go to the Fed to withdraw money. The Federal Reserve System is not a system. It’s a centralized actor with buildings in 12 separate states to give the illusion that it is decentralized. In reality, the majority of the power is concentrated in New York and the appointees all have the same ideals, or else they wouldn’t be appointed to the position in the first place.

So, what is the benefit of the Federal Reserve for the stakeholders like the Money Changers and the politicians? After all, many of these people at the meeting at Jekyll Island were in direct competition with each other’s business for the last 60 years. Why would they come together to form a powerful organization with those who sought to drive them out of business? It’s because it’s expensive and costly to try and wipe out competitors who amassed nearly the power and wealth you have. Instead, it would be more profitable to form a banking cartel. What is a cartel? According to Wikipedia, a cartel is an independent group of market participants that plan with each other to improve their profit and dominate the market. Once you break down the definition, it makes complete sense. The richest people in the world were tired of competing with each other in price, quality, and service. They were tired of undercutting the competitors by lowering their prices or trying to create the best quality goods and services to win over customers. Instead of competing, the independent organizations could work together to get rid of competition by agreeing that certain organizations will take a piece of the supply chain, a specific geographical location, or agree not to undercut each other’s prices

The results of the financial cartel have two main purposes; increased profits and increased power. If it’s not clear how the cartel can control prices let’s take a look at an extreme example that will help us understand the strategy. Imagine there are only two companies in the entire world that create products and services. If these two companies are completive against one another, they will try to create the highest quality product in the most efficient way possible at the lowest cost, benefitting the end user. If these two companies were to agree to create products, but work together to determine the price, then the companies could be overcharging you for the product, and have less efficient and innovative tactics leading to lower quality and more expensive products for the end user. It’s the same thing with money. This is the benefit to Money Changers, increased profit, and increased power.

What was the benefit for the politicians who agreed to allow the Federal Reserve to be passed? Well to understand this we need to understand how money is created and how government raises money for its projects and where the money comes from. Get ready for a brain twist.

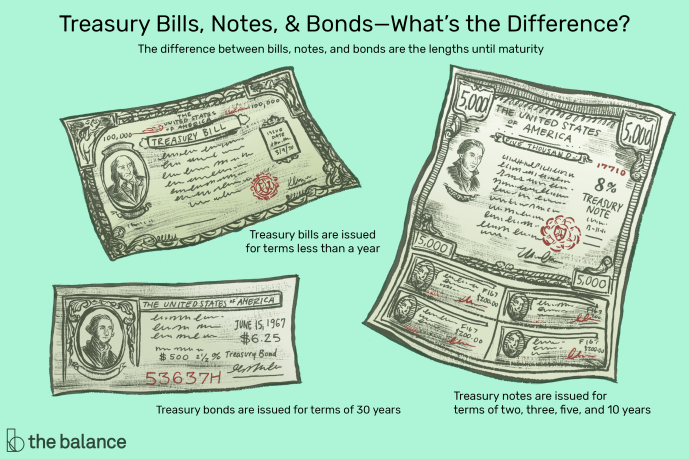

The two ways a government can increase its revenue is by increasing taxes or issuing debt. When politicians campaign on the basis of increasing taxes, they are generally unpopular with most citizens. However, the government needs to raise money for the various projects they are inefficiently attempting. So, what do they do? When all of the revenue from taxes runs out, Congress will issue bonds. What does it mean when Congress issues bonds? It means they are taking on debt, so when you are a company or an institution is buying government bonds, they are loaning money to the government. People will often claim that government bonds are the safest investment in the world because they are backed by the full faith and credit of the United States government. What that really means is that the US government will increase taxes, print dollars, issue debt, and have a monopoly on violence in order to pay back the interest they owe. However, when the desire to loan money to the government from the public runs out and the government still needs more money to spend, they will go to the Federal Reserve System.

(Difference between bills, notes, and bonds)

Have you ever thought about where Money comes from? At its face value, it may seem like a simple question, but once you begin to unfold the curtain behind the magician that is the Fed, then you might be surprised at how currency enters the economy.

Let’s say for simplicity it's 1 million dollars that are needed by the Federal Government for a specific project. The Federal Reserve will then buy the 1 million dollars of debt from the Federal Government in exchange for government bonds. Although today, they are not real bonds or real dollars, they are just bytes of code on a computer representing numbers. But wait, something important just happened, the Federal Reserve just gave the government a lot of money, where did the money come from? It didn’t come from anywhere, it never existed prior to this. There was a black hole that the Federal Reserve System reached into and typed into a computer 1 million dollars.

Now the government has 1 million dollars to spend on their projects and they didn’t have to raise the taxes one percent. Or did they? What occurred was debasement, a tax on the poor, a hidden tax or commonly known as inflation. There is now 1 billion more dollars in the world, which dilutes your holdings of cash, meaning you have less purchasing power, meaning your dollar buys less than it did when those 1 million dollars were not in the system. This is why Congress allows the Federal Reserve System to exist, they can get money on demand, with no questions asked, and don’t have to risk losing their office in Congress by advocating for an increase in taxes, or a decrease in spending.

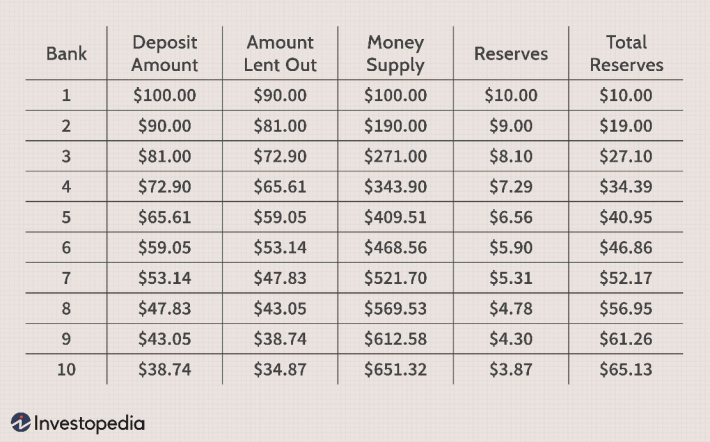

So, what does the government do with that money? Let’s say the government takes 1000$ of that money and uses it as an income subsidy for low-income workers. When the income is distributed to the low-income workers, they don’t send them 100$ bills, they will send them a check. With that check, you deposit the money into your local big bank. With the 1000$ deposited into your big bank in your personal savings account they now have the ability to loan out money. That’s what you are really doing when you deposit money in the bank, you are loaning the bank money. The banks also have a reserve requirement of just 10%, so with that 1,000$, the banks are able to keep 100 in reserves and loan out the other 900$.

So now, another person comes along and says I need a 900$ loan to get a car so he gets the loan from the bank and what does he do with the money? He deposits it into his big bank or buys something with the money so the seller can deposit the money into his bank. Now the bank has not only had the 1,000$ that was originally deposited into the bank, but now they have another 900$ deposited. Totaling 1900$. Where did this money come from? It was created at the exact moment a loan was signed and the money was moved into your personal savings account, it never existed before that moment and now the dollars circulate through the economy.

This is a good time to bring up that when you deposit money into the bank you are technically loaning the bank money. So now, the banks keep the 90$ for the 10% Reserve Requirement on the 900$ deposit and loan out the other 810$. and this continues on and on through the cycle until the original 1,00$ deposit is multiplied to 10000$ and the original 1,000,000$ the Federal Reserve loaned the government added 9,000,000$ into the economy that is being loaned out and charged interest. So where does the extra 9,000,000$ come from? The same black hole that the Federal Reserve reached in to create the original money. It didn’t exist before; it exists at the exact moment that a loan document is signed and the money is transferred into your banking account. Then, with the money that was created out of thin air, the banks get to charge you interest, leading to a hefty profit.

That’s how money is created, that’s called debasement and inflation which causes you to lose purchasing power, the prices of your goods and services increase, the quality of your materials decreases, the efficiency of the supply chain diminishes, and ultimately you feel poorer.

(How the Money Multiplier works, up to 10 levels, this continues until Money Supply is 10x original amount)

So, who benefits the most from the largest scam in American history, and who earns the loss in purchasing power the lower- and middle-class citizens suffered through? Since the money never existed before the Federal Reserve printed it and when the money hits the banks the dollars in circulation increase by a magnitude of 10, the entities or people who benefit the most are the ones who receive the money first, because those dollars have the largest purchasing power. Who gets the money after the government? Well, companies that have contracts with the government to build the projects and the large banks who get the deposits and loan out money and charge interest on money they’ve created from a black hole. By the time the money has reached people like you and me, then it has gone through its full cycle and the money is fully diluted.

The banks have a blank check to loan out to lower- and middle-class citizens and charge obscene interest while taking no risk. This creates a certain mentality in the American people that drives boom-and-bust cycles and is caused by the creation of the Federal Reserve System. This system of money creation incentives people to borrow, and disincentives people to save. Because if people borrow money, then they are the first ones touching the new money and they know that as time passes the money, they owe will be worth less in real terms, even if the numerical value of their debt obligation stays constant.

So why is it the biggest scam in the world, the deadliest thing that our planet has seen? Why is it dangerous for small groups of unelected individuals to have the power to print money at will with no one looking over their shoulder to make sure they aren’t causing issues? Because now the government, the institution with a monopoly on violence, can spend above and beyond what its capacity should be, resulting in the research into atomic bombs, the largest military budget in the world, the creation of terrorist groups, funding foreign wars, giving military support to countries across the world, some of which are our enemies, poverty, hungry children, ran down cities and more. Maybe these consequences weren’t intended from the creation of the Federal Reserve System, maybe some of them were, but these travesties are clearly a byproduct of the Fed’s doings. How can we be sure? Because using the law to empower an independent organization to have the power to print money at will and loan that money to the United States government, a bureaucracy known historically for its inefficiency, ineptitude, and high costs; gives the government the power to spend magnitudes beyond their capacity.

(Photo from 1936, Source https://www.flickr.com/people/92618257@N08 )

When we look at how this bill was passed, it was originally proposed in the Alrich Plan. However, public sentiment at the time understood Nelson Aldrich represented big business and large banks and therefore immediately shot down the bill. Therefore, to get the bill past the big banks and Senator Aldrich convinced democrats, important democrats, such as former presidential candidate William Jennings Bryan and others to pass the bill as the Federal Reserve Act. Once the bill was passed hundreds of amendments were created to the bill that would empower the Federal Reserve to create money out of different types of debt, corporations, real estate, foreign nations, and others.

In President Wilson's book, “Woodrow Wilson the New Freedom” he stated his justification for signing the bill into law, “it Is more important still that the control of credit also has become dangerously centralized. It is the mere truth to say that the financial resources of the country are not at the command of those who do not submit to the direction and domination of small groups of capitalists who wish to keep the economic development of the country under their own eye and guidance. The great monopoly of this country is the monopoly of big credits. So long as that exists, our old variety and freedom and individual energy of development are out of the question. A great industrial nation is controlled by its system of credit. Our system of credit is privately concentrated." In Wilson's eyes, the Federal Reserve would shift the strength of finance into a different power that was controlled by the government. In reality, the private bankers-maintained control over the system with a different name.

So, if the Federal Reserve is not an agency of the Federal Government, then who is the corporation owned by? The stock certificates that are issued, just like stock certificates for publicly traded companies are owned by the member banks. The member banks are the largest independently owned banks in the country that are handpicked by the Federal Reserve to serve as its cartel subsidiaries that will carry out the Fed’s functions. These stock certificates are a little different than publicly traded companies in a few important ways. The member banks cannot sell their ownership in the Federal Reserve. In addition, the banks with the largest assets under management get the most certificates, allowing them to take in the most profit. The member banks cannot choose who runs the Federal Reserve, those people are handpicked and appointed by the President. This excerpt was taken directly from the St. Louis Fed’s website, “So is the Fed private or public? The answer is both. While the Board of Governors is an independent government agency, the Federal Reserve Banks are set up like private corporations. Member banks hold stock in the Federal Reserve Banks and earn dividends. Holding this stock does not carry with it the control and financial interest given to holders of common stock in for-profit organizations. The stock may not be sold or pledged as collateral for loans. Member banks also elect six of the nine members of each Bank's board of directors” (https://www.stlouisfed.org/in-plain-english/who-owns-the-federal-reserve-banks)

So, the largest member banks in the world have the most power when it comes to electing the Board of Directors of the Fed; Private banks like J.P Morgan, Morgan Stanley, Wells Fargo, Citibank, and others get that responsibility for us. Good thing they are trustworthy institutions that never look to partake in illegal activity or scams. I could write an entire book on legal action taken against these 4 entities alone. Furthermore, these banks I just mentioned are too big to fail. Therefore, if they were to ever get into a financial struggle, the companies can go to the Federal Government or Federal Reserve which acts as a banker’s bank, and the government's banks and get money instantly. The bad decisions made behind closed doors, terrible investments, and risky loans made by these corporations, that are unable to be audited by the common person, cause the largest corporations to be bailed out by your tax dollars. However, if you own a small business and you ever get into a financial struggle, don’t expect to get a loan from one of these banks or especially the government. You may think this only happens in times of crisis, like the Great Depression or Great recession, but in fact, it happens much more often than you think: The Penn Central Railroad in 1970. Lockheed corporation in 1970. Commonwealth Bank of Detroit in 1972. New York City in 1975. Chrysler in 1978. First Pennsylvania bank in 1980. Continental Illinois in 1982 and countless third world countries that are paid by inflation or direct taxes (G. Edward Griffin. The creature from Jekyll Island) In fact, there is a more complete list of more recent bailouts at www.projects.propublica.org/bailout/list that includes names such as Citigroup, Bank of America, JP Morgan Chase, Wells Fargo, Morgan Stanley, AIG, Goldman Sachs, the US Bancorp Corporation and more that totals nearly a trillion dollars.

The next point I want to make is bringing up the purpose the Federal Reserve System was created for. In the words of famous economists, politicians, and Money Changers, the Fed was created to stabilize the United States economy. However, since the Fed was created, they have overseen the Post WWI Recession, a depression from 1920-1921, a recession from 1923-1924, a recession from 1926-1927, the Great Depression from 1923-1933, the recession of 1937-1938, Recession of 1945, Recession of 1949, Recession of 1953, Recession of 1958, the recession from 1960-1961, The recession from 1969-1970, The recession from 1973-1975, the 1980 recession, the 1981-1982 recession. The Early 1990s recession, the early 2000s recession, and the Great Recession from 2007-2009.

It appears that the Fed has done a marvelous job at stabilizing our economy, decentralizing the powers from New York, and creating an efficient marketplace. But how did we get to this point where the Fed has a strangle on the economy and the ability to create a recession at will? Well, we need to look at the next century of American history to figure out that answer. Now that we have a strong understanding of the Federal Reserve System, we can look at the United States economy, politics, and society post World War I.

(Money Supply During the creation of the Fed and the Great Depression. http://www.sjsu.edu/faculty/watkins/depmon.htm)