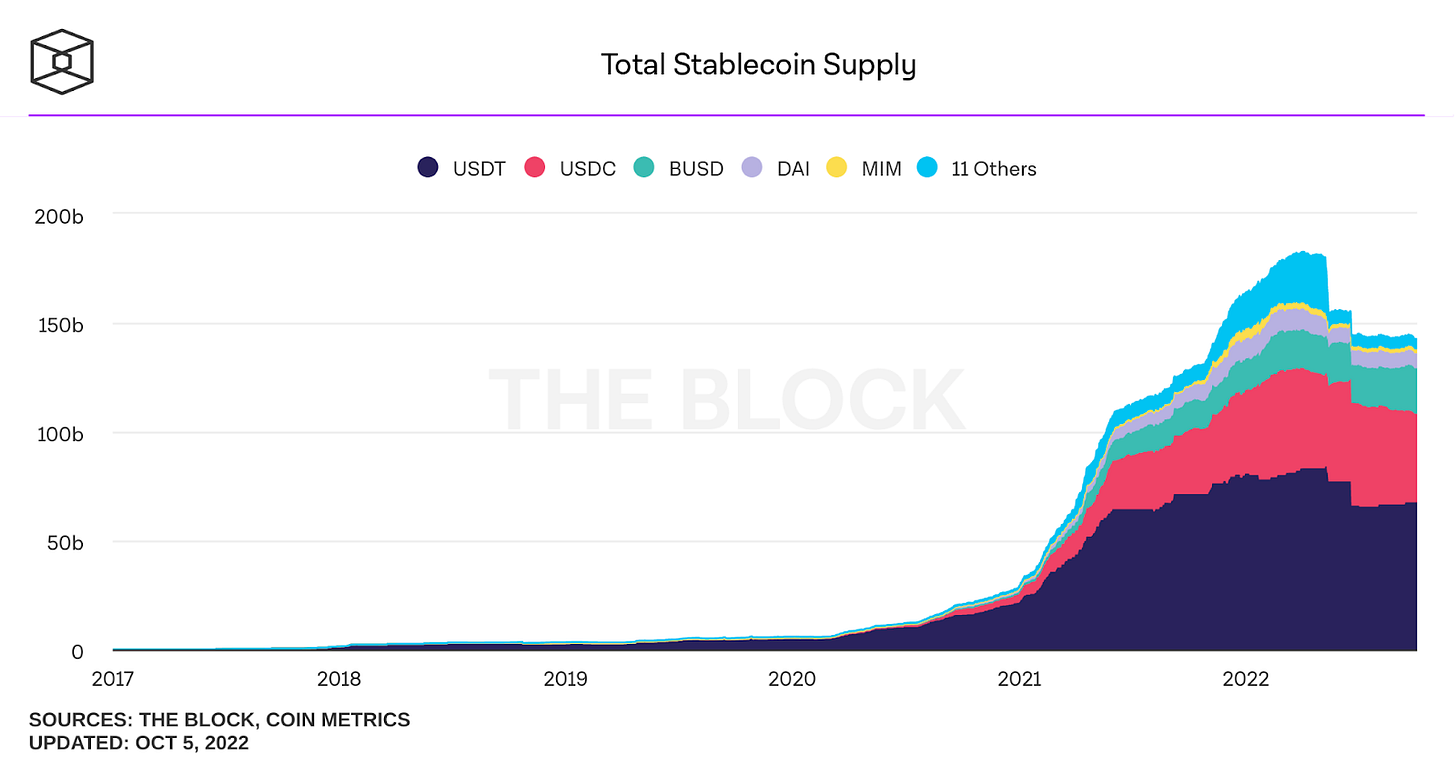

Cryptocurrency is known for its outrageous volatility. The huge fluctuations in valuations often make it a topsy-turvy investment. Still, investor attention in this new asset class is growing rapidly and when we talk about popularity or adoption, we can’t ignore stablecoins. The market capitalization of stablecoins grew four times in 2021 and they represent more than 10% of the crypto market now. Finance and technology have been co-developmental over the past decades. With the advancement of DeFi and Web 3 infrastructure, the demand for stablecoins is bound to grow exponentially in the coming time also. The strength of stablecoins is their attractiveness as a medium of payment. Low cost of transactions, speed of remittance and global reach are drawing more and more users to stablecoins. The DAPP ecosystem and blockchain networks are also providing a social experience to the users. The payments are no longer an act of transferring value. Stablecoins are connecting our digital lives and transforming finance today.

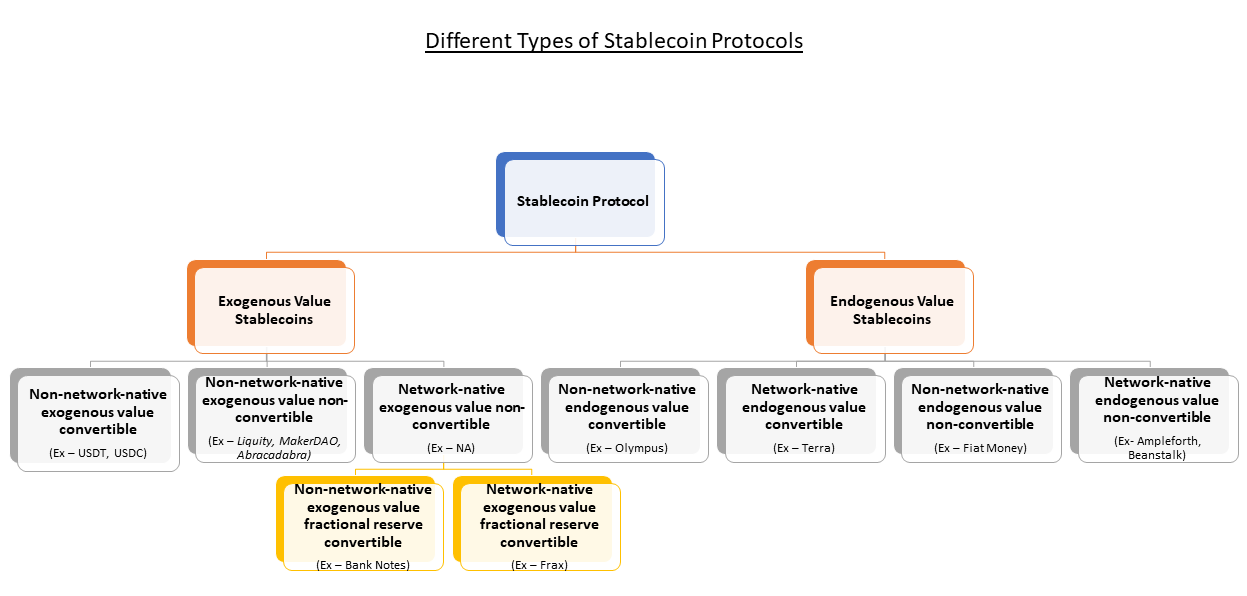

Different types of stablecoin protocols

A stablecoin is a fungible digital asset that maintains a stable value against an external asset class. The main purpose of stablecoin is to minimise price volatility and create a consistent and robust market environment. The history of money tells us that the market always accepts the least volatile assets as preferred currency. Post-emergence of DeFi, the Stablecoins like USDT, USDC, DAI etc. have already become the preferred currency of the decentralized world and they are playing a significant role in the growth of DeFi. Let’s discuss different types of stablecoins for a broad understanding:

Non-network-native exogenous value convertible stablecoin protocols: These are the most conventional protocols. They issue stablecoins which are collateralized. A custodian is responsible for convertibility to non-network-native exogenous value. The protocols act as permissioned bridges between their network and a stable medium (ex-USD). These types of stablecoins are generally less volatile but peg maintenance is often imperfect due to the frictions in convertibility. The carrying cost of such stablecoins is generally competitive. These stablecoins have decent liquidity but the off-chain collaterals don’t allow them to meet the demand in the market. Transparency issues regarding reserves of such protocols keep on resurfacing from time to time. Examples of such stablecoins are – USDT, USDC and BUSD.

Network-native exogenous value convertible stablecoin protocols: Such protocols work with over-collateralization of network-native collaterals. Over-collateralization makes the protocols cope with price volatility but it also makes them capital inefficient. Rent payment is required to prevent the value of the stablecoin from trending towards the value of the underlying collateral. Trustlessness is an excellent feature of such protocols. Volatility is also less due to low frictions in convertibility. Carrying costs remain high for these protocols. Over collateralization and rent payment hampers liquidity. Examples of such protocols are Liquity, MakerDAO, Abracadabra. These protocols have obviously found decent acceptance among crypto natives and stablecoins like LUSD, DAI and MIM is quite popular.

Non-network-native exogenous value non-convertible stablecoin protocols: People prefer centralized protocols like USDC, USDT due to convertibility. Convertibility also reduces price volatility and ensures trust in the custodian. Without convertibility, there is no point to go for a permissioned protocol as continuous speculations will lead to a high price volatility range. This is the reason such a protocol does not exist in the market as of now.

Network-native exogenous value non-convertible stablecoin protocols: Trustlessness is a good feature of such protocols. It started with Olympus and they tried to build a ‘non-pegged stablecoin’ or ‘reserve currency’. OHM was the currency designed by Olympus that was supposed to be less volatile than traditional cryptocurrencies. It was not pegged to any fiat currencies. Protocol-owned liquidity was a novel feature of the protocol and the treasury was a key function. Treasury represented all assets owned and controlled by the protocol. Non-convertibility (Olympus allows convertibility under certain market conditions) was a major weak point of the protocol and it led to extreme volatility. Carrying cost-wise it was better than network-native exogenous value convertible stablecoin protocols but that came at the cost of volatility. Numerous Olympus forks came out after the initial success of the protocol but conceptually it can be considered a failure.

Non-network-native exogenous value fractional reserve convertible stablecoin protocols: These permissioned protocols are most comparable to ‘Bank Notes’. It creates competitive carrying costs by using fractional reserves. The collateral can be lent out and the ‘Note’ bearers can receive part of the yield. Such a protocol can resist price volatility to some extent but the asset-liability duration mismatch can lead to collapse. As the protocol is dependent on collateral, the supply may not be able to meet the market demand also. There is no wonder that such a protocol does not exist in a decentralized market as of now.

Network-native exogenous value fractional reserve convertible stablecoin protocols: Such a protocol can be total permissionless. The network-native structure helps to reduce the collateralization requirement and thus it offers a competitive carrying cost. Volatility risk comes as a cost of this structure. Liquidity is again limited to the availability of network-native collateral assets. Frax is an example of such a protocol. The protocol’s stablecoin FRAX is backed by external collateral (primarily USDC) and part is algorithmically backed with the protocol’s native governance token FXS. Such a protocol is often exposed to a bank run.

Non-network-native endogenous value convertible stablecoin protocols: Such a permissioned protocol can create competitive carrying costs but it is difficult to create the endogenous value for the underlying asset. Liquidity is again an issue as the supply will depend on the underlying asset and its endogenous value. The ideal example of such a protocol can be a private company issuing a stablecoin that is convertible to company stock at market price. Obviously, nothing such exists as of now.

Network-native endogenous value convertible stablecoin protocols: Permissionless is a good feature of such a protocol. Carrying cost can be competitive but creating and maintaining the endogenous value of the underlying asset is difficult. Convertibility helps the protocol to keep price fluctuations less but the collapse possibility remains high. Terra is a project that offered high hopes with its dual token ecosystem - LUNA and UST (stablecoin). The project failed miserably.

Non-network-native endogenous value non-convertible stablecoin protocols: Such a protocol is permissioned in nature and can offer very competitive carrying costs. Although no such protocol exists on any decentralised network, fiat money can be considered as an implementation of credit-based non-network-native endogenous value non-convertible stablecoin protocols. The non-convertibility makes it non-transparent but volatility is low due to regulatory forces.

Network-native endogenous value non-convertible stablecoin protocols: Ampleforth can be considered the pioneer of such protocols. They maintain the price peg of the stablecoin by rebasing. AMPL, the stablecoin of Ampleforth is pegged to 1 USD (technically fixed to 1 USD in 2019 since the protocol considers Consumer Price Index data). If the value of AMPL goes above 1 USD, the protocol mints more AMPL. The high supply of AMPL leads to less demand for it and the price comes back to 1 USD. When AMPL trades below 1 USD, the protocol contracts circulating supply and less supply leads to more demand. The price comes back to 1 USD. Ampleforth has become successful to maintain the peg of the stablecoin but it could not create utility for the stablecoin. During the low demand periods, the extreme negative carrying cost kills all use cases of it.

Let’s explore Beanstalk

The borrowing rate on exogenous value convertible USD pegged stablecoins like USDC and USDT is higher than borrowing rates on USD. The reason is the high demand for such assets despite an increase in supply. DeFi is based on the principle of trustlessness, so we need alternatives to centralized stablecoins. The issue is the non-competitive carrying cost of network-native trustless assets. This can be improved by network-native credit. The current financial system runs on fiat money which is a credit-based system and the Central Banks issue credit. Beanstalk is trying to do that with its credit-based network-native endogenous value non-convertible stablecoin protocol. It is just like the implementation of fiat money on the Ethereum blockchain. The project was launched in August 2021 by a group of anonymous developers called Publius.

Bean is the stablecoin issued by the protocol and it is currently pegged to USD. The Bean Farm has two main components – the Silo and Field. The Silo is the Beanstalk DAO that helps to govern the protocol in a decentralized manner. The Field is the credit facility of Beanstalk. You can sow Beans in the Field in exchange for Pods when the protocol wants to issue debt (i.e., when there is Soil in the Field). The Pods are the native debt assets of Beanstalk (also tradeable on the native marketplace). The Temperature refers to the interest rate for sowing Beans (the maturity date is determined by the protocol). Bean is a rebase stablecoin and maintains its peg a bit similar to AMPL but the credit facility of the protocol makes it different.

The innovation

The Sun is the protocol-native timekeeping mechanism of Beanstalk. Beanstalk adjusts the price of Bean to 1 USD at the beginning of every Season. Each Season is designed to be ~1 hour long but Seasons do not begin until the sunrise () function has been called through an Ethereum transaction. Every season changes the Soil supply and Temperature. A rebase protocol like Beanstalk prints more Bean when the price of Bean is above 1 USD. The additional supply helps to keep the price down to the peg. The newly-minted Beans are distributed to Silo members in accordance with their share of the total outstanding Stalk (you receive the governance token Stalk in proportion to your deposited amount to the Silo) and to pay down debt in the Field, on a 50:50 basis. The protocol also sells Bean directly on Uniswap so that Bean’s price returns to 1 USD. Maintaining peg often becomes difficult for rebase protocols when the price keeps on falling! Beanstalk issues debt and Soil appears in the Field when the price of Bean drops below 1 USD. The high APY of the Field (denoted by Temperature) encourages the investors to buy Bean from the market to Sow (i.e., lend) in the Field. Beans are burned when sown, which reduces the total supply of Beans. Less supply pushes the price back towards its peg.

Beanstalk is evolving continuously. A lot of new features have been added post-launch of the protocol. The protocol governance is already launched and the network nativity makes it completely decentralized with no probability of a single point of failure. There is no reliance upon any centralized price oracle. Instead USDC: ETH and BEAN: ETH Uniswap V2 liquidity pools are used as decentralized price oracles. The usage of credit makes Beanstalk more resilient compared to other rebase stablecoin protocols. There is no supply shortage of Bean and the protocol is capital efficient by design. The competitive carrying costs of trustless Bean make it a really attractive option for investors. If you want to earn interest from your Bean, you can deposit it into the Silo to earn high interest just like a bank account. There is a long way to go but Beanstalk promises to surprise you with its native yield-generation mechanism. The holy grail of the ideal stablecoin protocol is being built to create the next-generation financial stack. Keep a close watch on beanstalk!

Follow Beanstalk on Twitter to get regular updates and join their vibrant Discord. DYOR before investing.

Note: The article was first published here.

Follow Me

👉 Twitter @paragism_