While ASML's financial results today exceeded market expectations, its forward guidance did not please investors. While the financial results technically demonstrated strong growth and profitability metrics, their impact on investor expectations and the share price was significantly disappointing. In light of the company's recent statements and analyst assessments, it is necessary to re-interpret the financial results with a more critical perspective.

Guidance Below Expectations, Growth Failing to Reach the Upper Band

ASML updated its annual revenue growth forecast to 15% for the full year 2025 and announced a gross margin target of 52%. This suggests a turnover of approximately €32.5 billion. However, while previous guidance had called for a range of €30-35 billion, both the market and many investors expected a result closer to the upper band. Therefore, the new guidance was perceived as a downgrade in expectations despite a strong quarter. While some investors and analysts expect better growth, a 15% target necessitates downward revisions to operating profit estimates and increases valuation pressure.

Uncertainty in the 2026 Outlook and Selling Pressure on the Stock

One of the most critical points is ASML's inability to provide definitive growth guidance for 2026. While the CEO noted strong demand from AI-focused customers, he stated that growth in 2026 was not guaranteed due to increasing macroeconomic and geopolitical risks. This statement contrasted sharply with the company's stated statement at its investor day last November that "2026 will be a year of growth" and created significant selling pressure on the stock. Following the earnings report, the stock fell between 6-9%. This downward movement was a clear indicator of a lack of market confidence and a guidance revision.

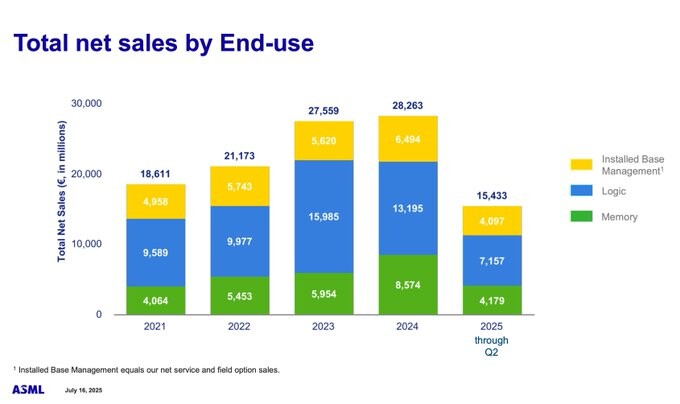

Segment and Product Trends, Demand, and Risks

Although high net bookings (€5.5 billion, primarily focused on EUV) and continued demand for high-tech equipment in the second quarter paint a positive picture, trade tensions between the US and China, coupled with the potential for new tariffs, are putting pressure on ASML. The threat of a 30% tariff the US is considering on semiconductor equipment from the EU, in particular, threatens the company's growth prospects. The company is working on various supply chain strategies to minimize the impact of such developments, but these risks cannot be completely eliminated.

Analyst Commentary and Target Price Revisions

Some institutions have downgraded ASML's recommendations and target prices both before and after the earnings report. For example, KBC Securities downgraded the company from "accumulate" to "hold" and lowered its target price to €686. These revisions are based on both the weakening growth expectations and the increasing risks surrounding 2026.

Strategic Assessment and Investor Perspective

ASML's Q2 2025 financials, while operationally and technically strong, indicate that it has entered a period where its medium- to long-term growth momentum and investor confidence are in question. While the weak base effect of previous periods has made growth figures appear "good," the outlook for the future is one of increasing macroeconomic and sectoral risks. The company maintains its leadership position thanks to its innovative product strengths and demand for AI and advanced technology, but investors' desire for "pricing power and stable growth" is not being met by the current guidance.

The share price highlights downside risks in the medium term due to the selling pressure that has developed after the earnings report. For ASML to reassess its strategically sustainable growth, its ability to manage macro and commercial uncertainties, along with operational efficiency and the ability to increase market share in innovative segments, will be critical.

Brief Summary:

While ASML's financial metrics appeared strong in Q2 2025, the tightening of growth guidance and increasing uncertainty about 2026 have created selling pressure on the stock. Beyond temporary positive base effects and currency advantage, it's critical for the company to reassert its sustainable growth and pricing power. For investors, the risk/reward balance should be viewed with caution as long as guidance remains at the lower band.

The information, comments and recommendations contained herein are not within the scope of investment consultancy. Investment consultancy services are provided within the framework of the investment consultancy agreement to be signed between brokerage firms, portfolio management companies, banks that do not accept deposits and customers. The comments in this article are only my personal comments and these comments may not be appropriate for your financial situation and risk return. For this reason, investments should not be made based on the information and comments in my articles.