As it seems some people actually did like my posts about my token portfolio and its evolution, I decided to share my P2P portfolio as well. I'll try to update it similarly to my crypto portfolio on a monthly basis and share not only the services I'm using but also why and how I'm using them.

But first, this is an important disclaimer: I'm not an investment professional or a licensed financial adviser. This post represents my personal opinions and decisions, which may not be appropriate for your personal case. Please use common sense or consult with an investment professional before investing your money. I am not responsible for the outcomes of your decisions, nor am I responsible for the comments posted by readers or the contents of any linked websites. This post should be viewed for educational or entertainment purposes only.

What P2P services?

Mintos

I opened an account at Mintos in June 2019. I selected Mintos at that time after a careful study among blogs and reviews and I'm currently not disappointed by my choice. If Mintos is probably the biggest P2P lending platform in Europe, it does not provide its own loans but let companies register to the platform and offer their loans to investors. There are currently around 70 loan originators registered on Mintos providing various loan types to end users in 33 countries. My initial deposit was only 1500 Euros and I followed with a 11000 Euros deposit in July 2019 once I was convinced by what I tried.

Strategies used on Mintos

I started by using the "Invest & Access" tool. This is basically the easiest way of using their platform, the advantage is that you can get back most of your money very quickly if needed, the issue is that you do not control at all on what your money is invested. So, the interest received is sub-optimum AND the risk is actually high as the diversification algorithm might select very risky loans in a very concentrated way. So, I quickly decided to use instead their "Auto Invest" tool.

The "Auto Invest" tool allows defining custom strategies with very precise parameters controlling how investments are done. So, I selected first:

- only Loan Originators with a rating higher than C (so it's 62 of the 70 possible Loan Originators)

- all 33 countries were selected

- only loans with Buyback guarantees

- all loan types were selected

- interest to be 11% minimum

- 24 months maximum loan duration

- between 10 and 100 Euros per loans

- specific diversification settings to be as close from possible to the equal distribution

This worked very fine until the virus came, the first warnings from Loan Originators arrived and I realized that my portfolio of loans was mostly (80%) invested in "Personal Loan" and "Short term Loan". Those loan types are basically the most risky in those difficult times. So, I stopped my previous strategy, sold part of my loans on the secondary market and tried to refocus my portfolio to something less risky: So, I am now using the following strategy:

- only loan types with collateral meaning "Mortgage loan", "Business loan", "Agricultural loan", "Pawnbroking loan", "Car loan"

- only loan originators with a rating higher than B-, so it's only 17 of the possible 70

- only 17 countries are now used

- only loans with Buyback guarantees

- interest is 7% minimum

- 80 months maximum loan duration

- between 10 and 50 Euros per loans

- specific diversification settings to be as close from possible to the equal distribution

Today, this is the current allocation of my loan portfolio, currently composed of 400 loans:

Mintos Buyback guarantee ? Really ?

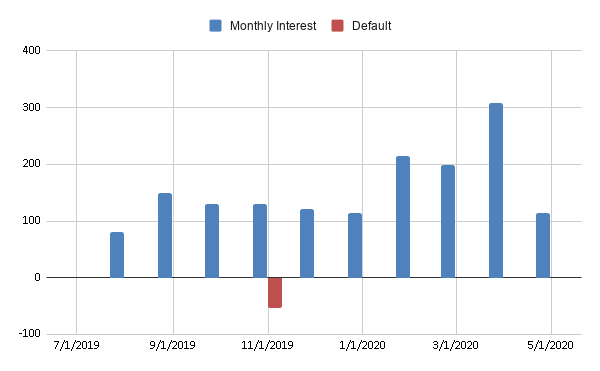

All my loans are with "buyback guarantee", meaning that if the end user stops repaying the interest or capital, after 60 days, the loan originator will repurchase the loan and return my money with interests. That's very good ... until the loan originator gets out of money. So, it happens on my loans already once and I expect that it will happen again in the following months. Mintos is still trying to get back the money of all investors that invested in those defaulted loans but it is very slow. Currently I lost 50 euros like that.

Advanon

I opened an account in Advanon in November 2019. This Swiss platform is fairly confidential and is in the market of invoice financing for Swiss and German companies using peer to peer investors. The principle is simple: twice per day Advanon proposes to investors to buy parts of invoices between companies so that those companies can get access to the invoice money immediately and not wait between 1 or 3 months as it is usual business practice. Obviously the companies have to pay back the invoice and some interest to the investors when they get payed back by their creditors. Here, the amount are not the same, the usual part of an invoice is at least 1000 Euros or CHF. The benefits of this mechanism is that I can select the local company that I want to help based on their financial information, their website or their online reputation and I also can avoid the currency risks that I have usually with Euros or USD.

Strategies used on Advanon

I first read the financial data of the company and in particular the Altman Z-score needs to be higher than 2.9. Then I go look the company website and if I do not understand the company business model in less than 2 minutes, I basically do not invest. Finally the annual return on the investment (ROI) needs to be at least 10%. I started by investing the minimum and gradually increased to around 3000 CH/Euros per investment.

I significantly reduced my new investments on the platform when the virus came, both because I was a bit scared of what would happens to the companies during that time and because the offers decreased a lot. I am gradually increasing again the amounts now that the situation in Europe is getting a bit better.

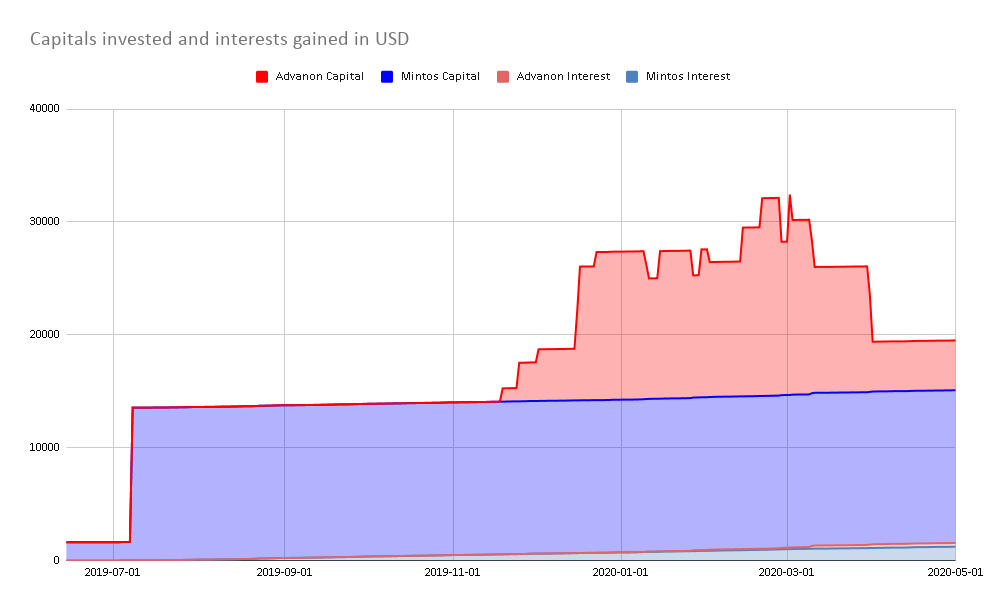

What are the results until now?

The previous diagram shows that there is delay between the investment and the interests for both Mintos and Advanon, but it is increasing nicely. It also shows the difference in capital management between both platforms. With Mintos, the capital is basically automatically re-invested all the time unless you manually decide to do sell actions. With Advanon, the capital and interest come back to my bank account each time the companies pay back their invoices and it is up to me to manually re-invest in each invoice if I want.

To compare with my crypto interest, this is the details of my earnings in USD using both platforms since I'm using them:

So, this diagram shows clearly that the interests were growing nicely until I stopped investing in Advanon. It also shows the loss of 50 Euros in October and I'm expecting for more losses in the following months with Mintos.

What's next ?

- I'll continue monitoring the performance and potential new warnings of loan originator on Mintos and potential losses

- I think I'll try another P2P service, I'm tempted by something specialized in real estate. If you have some good recommendations, I would be interested to read that in the comments.