In the high-stakes world of investment management, few managers consistently outperform the S\&P 500 benchmark while maintaining a famously patient and selective approach. David Rolfe, the Chief Investment Officer of Wedgewood Partners, is one such 'quiet giant.' As the market cap of the 'Magnificent Seven' continues to dominate headlines, Rolfe's latest portfolio shifts, revealed in recent 13F filings, offer a compelling counter-narrative for value-oriented investors. His current strategy is a masterclass in separating true intrinsic value from fleeting market momentum.

A Disciplined Focus on High-Quality Growth

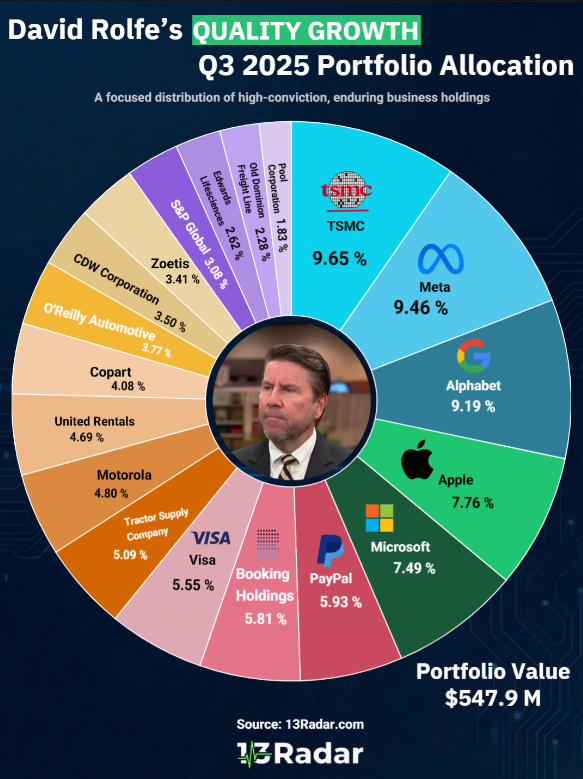

Rolfe’s philosophy centers on identifying companies with wide economic moats, predictable earnings growth, and exceptional management. Unlike funds that trade frequently, Wedgewood's portfolio turnover is remarkably low—often single-digit percentages annually—signaling deep conviction in their long-term picks. This quarter’s filing reaffirms this belief, showing a continued preference for businesses that generate massive amounts of free cash flow (FCF).

A look at the latest filings reveals that several long-held positions still form the bedrock of the portfolio. These are companies where Rolfe believes the market is underpricing the future stream of earnings. For investors seeking this disciplined, long-term perspective, an in-depth analysis of his holdings is crucial. You can explore the full details of the David Rolfe Current Portfolio.

Data Snapshot: Recent Moves and Portfolio Concentration

The recent 13F data provides concrete evidence of Rolfe’s current thinking. While many institutions aggressively piled into pure-play AI stocks, Rolfe maintained discipline. For instance, Rolfe has a notable exposure to companies that benefit from technology adoption but are not solely dependent on speculative hype. His top 10 holdings often represent over 50% of the total portfolio value, underscoring a belief that concentrated bets on outstanding businesses yield superior results.

Specifically, the data shows a marginal increase (or consistent holding) in certain tech-adjacent consumer brands—companies that leverage strong brand equity and robust global distribution networks. This suggests Rolfe sees better value in the execution and scaling power of established leaders rather than chasing nascent technologies at sky-high valuations. The key takeaway from the latest data is simple: Rolfe is paying for quality, not hype.

The Value Thesis: Why Rolfe Is Avoiding the Crowd

In a market where many stocks are trading at P/E multiples well above historical averages, Rolfe’s relative caution makes sense. His moves suggest that he views the current risk/reward profile of some market darlings as unfavorable. The fund is positioned to weather potential volatility by focusing on earnings quality. By maintaining exposure to companies with strong competitive advantages, Rolfe aims to generate alpha regardless of the prevailing macro climate. His portfolio remains a powerful case study for investors tired of chasing market trends and ready to embrace the power of fundamental, quality-driven analysis.