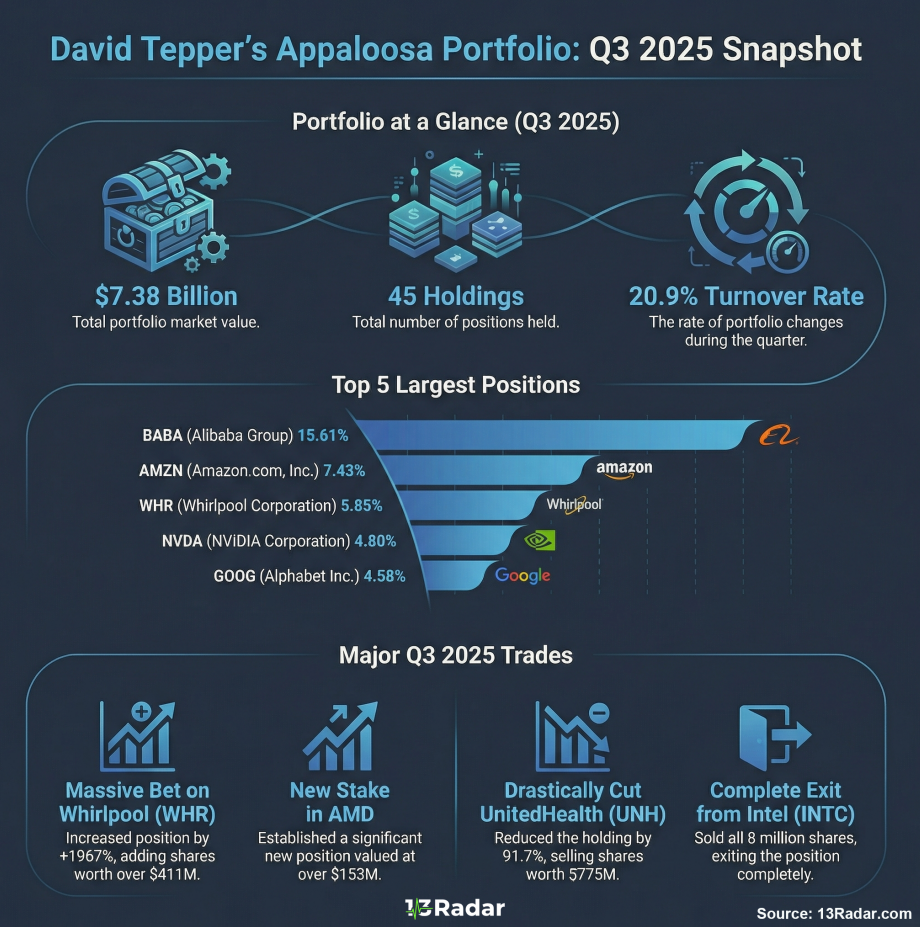

In a world where herd mentality often dictates market movements, David Tepper, the founder of Appaloosa Management, stands out for his willingness to walk alone. While Wall Street has spent the better part of the last year debating the sustainability of the US tech rally, Tepper has been quietly executing one of the most controversial macro trades of the decade. His recent filings reveal a distinctive shift that separates him from his peers: a massive, high-conviction bet on undervalued Asian equities at a time when geopolitical tensions are dominating the headlines.

Tepper has never been afraid of distress. From betting on banks in 2009 to buying energy when oil went negative, his career is built on the philosophy of buying when others are panicked. The current composition of david tepper’s top holdings reflects this classic contrarian DNA. While the consensus is to hide in US Treasury bills or stick to the "Magnificent Seven," Tepper sees a valuation disconnect in Chinese technology and consumer cyclical sectors that is too large to ignore.

>>> THE "BIG LONG": Looking East When Others Look Away <<<

The most striking aspect of the recent 13F disclosures is the sheer size of the allocation to specific Chinese tech giants. This isn't a small hedge; it’s a portfolio-defining stance. Tepper appears to be betting that the valuation compression in companies like Alibaba (BABA) and PDD Holdings has reached a mathematical floor, regardless of the broader economic sentiment. He is effectively arguing that the price you pay matters more than the macroeconomic headlines you read. When stocks trade at single-digit P/E ratios with double-digit growth, Tepper buys, irrespective of the zip code.

Reducing Exposure to Overcrowded Trades

Conversely, what Tepper is selling is just as important as what he is buying. There is a clear trend in his portfolio of trimming winners. After riding the semiconductor and AI wave to massive profits, Appaloosa has seemingly engaged in tactical profit-taking. This isn't necessarily a bearish call on AI, but a disciplined risk management move. By reducing weight in stocks that have doubled or tripled, he is freeing up capital to deploy into the aforementioned distressed assets, maintaining a balanced risk profile that isn't overly exposed to a single sector's valuation multiple expansion.

The "Everything to Gain" Mindset

Tepper famously said, "I think I’m the only one that doesn’t know what’s going on." This humility masks a sharp understanding of risk/reward asymmetry. His current portfolio construction suggests he believes the downside in his contrarian bets is capped, while the upside—should sentiment normalize even slightly—is exponential. For investors, the lesson is clear: True diversification often feels uncomfortable. If your portfolio looks exactly like the S&P 500, you aren't diversified; you're just average. Tepper is striving for exceptionalism by embracing the discomfort of the "uninvestable."