If you’ve followed my previous post on GMX, you’ll know that since we’ve entered the bear market that I’ve been looking for places to safely park my blue chips, in order to wait the storm out. Similar to GMX, Liquity is a decentralized protocol that generates rewards from people’s liquidations except with up to 100% of the profits being “kicked back” to stakers, rather than GMX’s 70%.

In addition the mechanics for Liquity are significantly different, for in order to participate in reward earning, users have to put up $ETH as collateral in order to borrow $LUSD, then deposit $LUSD in a “stability pool” where stakers get a proportional share of rewards off of people getting liquidated. For borrowers, Liquity is extremely attractive because there are 0% fees for borrowing against your $ETH.

Sound a little complicated? Well follow me as I walk through what I’ve learned through my research of the platform, and why you might want to consider Liquity as a place to park your $ETH while we finish out the tail end (hopefully) of this current bear market.

Frontends

First and foremost, an interesting feature (or lack thereof) is that Liquity does not have a native frontend to access the Liquity protocol. Instead, there’s a list different public frontends (or else in fact you could actually create your own). In a nutshell, a frontend is really just a user interface — all different options that you can access from Liquity’s website that differ in user interfaces and different Kickback rates. The Kickback rate is the percentage of rewards that you as the user will receive. I liken it to the fees that you might give to a validator that you use to stake your tokens to, with 100% equating to 0% fees taken or in other words, a 99% Kickback rate means that there would be a 1% fee.

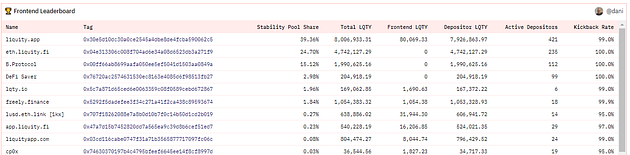

Not sure of what frontend to use? There’s a nice breakdown showing the Frontend Leaderboard and how many active depositors there are on each available on dune analytics. To date, here are the most widely used frontends with their corresponding Kickback rates:

After sorting through several different frontends, the only differences I could find were differences in UI or add-on features (for instance DeFi Saver allows you to access Stop-Loss protections), but essentially most will allow you to access Liquity fully if your main goal is to either borrow against your $ETH and/or profit from $LUSD staking. For the rest of the article I’ll be taking screenshots from app.defisaver.com, but by no means am I recommending (or not recommending) them. You should DYOR research and find which frontend is personally most comfortable for you.

Creating Troves

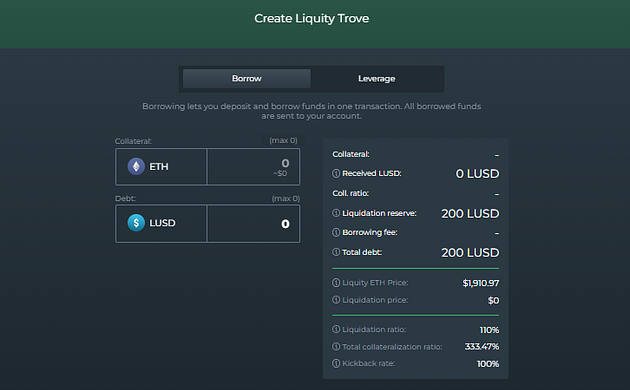

After selecting your desired frontend, in order to utilize Liquity you must create a “trove” by depositing $ETH as collateral and then borrow $LUSD, which is is Liquity’s native stablecoin:

As you can see above, you can essentially set your own collateral ratio which is dependent upon the amount of risk you want to take with getting liquidated. There are limitations with the platform, with the minimum collateral ratio needing to be at least 110%, meaning that the amount you lend in $ETH has to equate to 110% of what you borrow. An important thing to note is that if the value of your lent $ETH significantly decreases in value, your collateral ratio ratio readjusts putting you at risk for liquidation. You of course can customize your own collateral ration to decrease your level of liquidation risk, and it appears that the majority of Liquity aren’t that degen as the current total collateral ratio is at about 335.6%.

One more thing to note is that you’ll see 200 $LUSD being placed in a “Liquidation Reserve” which is set aside just in case if your trove gets liquidated, as the onus of the gas fees for liquidations are paid by the trove holders, not by the liquidators. Thus your collateral ratio is based on the amount you borrow minus the 200 $LUSD that has been set aside in the Liquidation Reserve.

The Returns

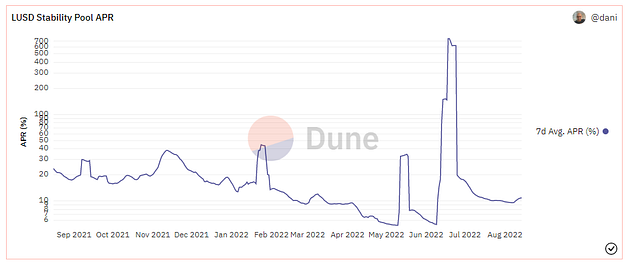

Sorry that it took me so long to get to this part, because this is probably the part that most people are interested in — the returns. Because market conditions can take rapid turns, so can the reward rates of LUSD stakers. This is why it’s no surprise that we see significant fluctuations in reward rates:

Looking at the historical 7-day average, there’s a gigantic range in returns, going from as low as 5.3% and as high as 751%. And just in case if you’re curious, that 751% spike corresponds to when $ETH dived from around $1800 dollars to around $900 in just a few days.

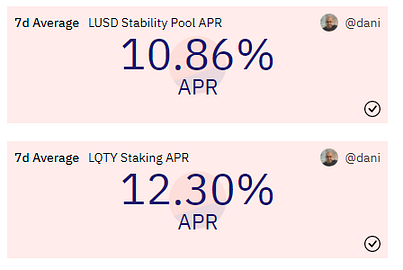

$LQTY Token: Similar to the $GMX token, Liquity also has their own native protocol token $LQTY which when staked, will provide a share of the protocol’s borrowing redemption fees. To date, the current rates for $LQTY staking are slightly higher than the returns of $LUSD:

Other key factors about Liquity

What you see is what you get: As listed in their whitepaper, Liquity is defined as a protocol and not a platform, which is also the reason why they have no native frontend. There are no governance proposals, there’s no administrators, or in other words, there’s no real way to stop the protocol — only ways to stop frontends. I think that this is probably the coolest thing about Liquity because the whole protocol is completely decentralized and algorithmically-based. The protocol is essentially immutable and has been that way since its initial release.

$LUSD Price fluctuations: If you take a look $LUSD’s price history you’ll notice something pretty concerning for a USD-pegged stablecoin, the peg has ranged from around $1.00 to sometimes $1.05:

From what I’ve gathered, the fluctuation is a product of simple supply and demand pressures — the price of $LUSD rises when there are relatively few new loans being taken out, which causes an increase in the token’s demand. Or in other words, no new loans means that no new $LUSD is being issued, which means there’s a scarcity of $LUSD which in turn drives up the price.

Redemption Fees: I’ve mentioned before that there you can borrow $LUSD against your $ETH interest free, but that does not mean that Liquidity is void of fees. Instead of paying interest, when you redeem your loan the protocol charges you a Redemption Fee that is determined by the following calculation:

Therefore because it’s algorithmically adjusted it’s hard to say what your exact fee will be, but the fee is only incurred one-time when you redeem and it can go as low as 0.5%.

Recovery Mode: As I mentioned before, under normal circumstances if the the collateralized ratio falls below 110%, the user is at risk of becoming liquidated, however one key metric to track is the protocol’s Total Collateral Ratio. If the total value of the $ETH on the protocol crashes quickly, because the total value of $LUSD remains the same, in order to compensate for the balance, Liquity enters “recovery mode” where the liquidation rate essentially is readjusts to a threshold of 150%, resulting in a higher liquidation price.

How does Liquity stack up against GMX?

Like I mentioned before, GMX is is a similar platform that allows stakers of $GMX/$GLP to profit off of liquidations; however, there are some significant key differences:

- With Liquity, unless you get liquidated, you still essentially own your $ETH. Although there’s technically no impermanent loss with GMX, you still are converting your $ETH to a different token all together to generate your returns.

- Speaking of $ETH, Liquity is on Ethereum Mainnet while GMX operates on Arbitrum and Avalanche. That is why with Liquity we see a required 200 $LUSD liquidation reserve requirement to compensate for Ethereum Mainnet’s potentially higher gas fees.

- Liquity is inherently more risky because there is always a possibility of your loaned $ETH becoming liquidated, however the potential ceiling for rewards is relatively much higher than GMX, as a bigger proportion of liquidations rewards are returned to Liquity’s $LUSD stakers.

Conclusion

After doing a deep dive on Liquity’s fundamentals, I truly believe that protocols Liquity are the next evolutionary step towards lending protocols, and I wouldn’t be surprised if we saw more Liquity-type protocols rather MakerDao’s in the coming years. In addition, despite the liquidation risks I truly wish I found out about Liquity sooner because just like I did with GMX, in future bear-market lulls I definitely plan to likewise utilize Liquity to park some of my idle $ETH.

Thanks again for reading and if you have any other questions or comments, feel free to leave them below. Thanks for reading, and be sure to follow me on my twitter account to get all my latest updates: https://twitter.com/CryptosWith

Disclaimer: And as a final reminder, this is not financial advice and this is for educational and entertainment purposes only. Please as always, do your own research and find what investments are best for you. Cheers everyone!