"The underlying cause of the crash will be found in the preceding months and years, in the progressively increasing build-up of market cooperativity, or effective interactions between investors, often translated into accelerating ascent of the market price (the bubble). According to this “critical” point of view, the specific manner by which prices collapsed is not the most important problem: a crash occurs because the market has entered an unstable phase and any small disturbance or process may have triggered the instability."

-- Didier Sornette, "Why Stock Markets Crash: Critical Events in Complex Financial Systems"

For anybody that has been around in cryptoland long enough, Tether is a major household name of a perpetually unfolding controversy that has managed to pull off such elaborate and brazen crypto-scam stunts in its 5+ years of existence that it makes one really wonder about a lot of things. Especially in retrospect, but also in light of what follows next in the immediate future ahead. In any case, one lesson we should have all learned by now in 2019 is to have some notion of how to separate the wheat from the chaff in these irrationally structured markets running on peer-to-peer networks.

As the digital crypto-asset markets were just slowly starting to form back in 2014, things were even clunkier and even less user-friendly (or just "usable" in general) than they are today. And there were few mechanisms in place for doing much of anything and barely any standardization, people mostly focused on coming up with ways of building upon and extending the Bitcoin protocol itself -- or trying out various application-specific forks and modifications. One thing there was an obvious need for was a reliable fixed-price instrument or an asset to hedge with during times of extreme volatility or rapid market downturns.

Tether and Bitfinex were the first to go ahead and attempt to fill that gap in perhaps the worst way possibly imaginable (but seems to have made sense to many at the time). Which ended up triggering a series of disasters with long-lingering consequences and possibly critical systemic implications for the digital crypto assets markets in their present structural arrangement. In what follows, instead of reviewing the technological basis and functional aspects of USD Tether, we'll instead focus on the external factors and influences grounded in legacy financial systems that come into play when trying to bridge the two realms with a quick "dirty fix".

Stablecoins: On-Chain Representations of Non-Volatile Fixed-Value Assets

Stablecoins constitute one of the crucially important yet still unsolved problems in the cryptosphere. They are are digital crypto-assets that are pegged to the relatively stable value of some other asset through some mechanism or another. They are most commonly used as a safe haven to park funds at during periods of high volatility and rapid market downturns (or in other such hedging strategies where one needs to lean on the good old US dollar), providing an otherwise much needed service to the space.

Broadly, stablecoins can be divided into two categories -- asset-backed stablecoins and algorithmic stablecoins. The former rely on keeping reserves of the underlying asset (USD, gold, etc.) so that each token of circulation corresponds to an equivalent unit in reserve. The latter ones, the algorithmic stablecoins, implement some kind of feedback loops and set critical thresholds which trigger certain automated corrective operations in the event of losing the peg (and are systems actively governed, usually as a DAO).

Multi-collateral Dai. MakerDAO is to diversify the types of collateral (presently it only works with wrapped pooled Ether) that can be used for maintaining the soft peg of Dai to the US dollar. These will include other reliable and well understood assets such as DGX, REP, ZRX, OMG, WBTC and others. In the future and as the DeFi movement grows, MakerDAO may develop to allow for the programmatic composition of insurance strategy stablecoins in all kinds of configurations.

An example of asset-backed ones is the notoriously controversial Tether (USDT) as well as TrueUSD (TUSD), DGX (tokenized gold managed by a consortium DAO of provider, vault keeper and auditor) and others. The most well-known algorithmic stablecoin is the MakerDAO-governed Dai which has at this point become an integral component of the Ethereum ecosystem. Dai is soft-pegged to the US dollar and backed by an overcollateralized amount of pooled, ERC-20 wrapped Ether (WETH) conditionally locked in a smart contract.

However, the end goal of the MakerDAO organization (sometimes called the "Fed" or "central bank" of Ethereum, in the sense of managing the monetary/fiscal stability in the system) is to diversify risk profiles, standardize insurance strategies and broaden the forms of accepted collateral as well as types of pegs to other financially useful assets (see Multi-collateral Dai).

Dai is the stablecoin widely adopted in the Ethereum ecosystem and among the DeFi stack of financial applications. The dollar value peg is actively maintained with critical emergency response mechanisms put in place. The risk management of the system is managed by a competent and appropriately compensated DAO.

In any case, Tether is historically the very first stablecoin to be introduced and widely adopted by the market while at the same time one of the most problematic ones to the extent of the potential systemic risk it presents to the otherwise fairly self-enclosed crypto markets (which still tend to synchronize around the movements of BTC and the disproportionate concentration of centers of influence in a few centralized exchanges).

Tether was originally launched on Omni, a Bitcoin overlay network for assembling other types of assets on top of the Bitcoin protocol (which was itself incubated from the Mastercoin project), but has since also been deployed on Ethereum as an ERC-20, Algorand, TRON and EOS. With each of these implementations introducing some subtle changes as befitting the intentions and interests of the Tether company and to the extent the corresponding platforms allow to get away with (e.g., the ability of the contract owner to freeze and burn any user's funds arbitrarily, etc.)

The Bizarrely Convoluted Story of Tether, Everybody's Favorite Systemic Risk

Tether is one of those almost unbelievable hallmark trainwrecks from the earlier days of blockchain-based rogue crypto-hawalas when everything was a whole lot more chaotic and confusing and the complete absence of any regulatory constraints whatsoever (just preventing double spending in a digital world doesn't magically make everything "trustless"), it quickly led to the rediscovery of every dirty trick and crooked scheme outlawed since the last 200 years. A "wild wild west" where organized pump-and-dump operations were almost trivial everyday occurrences and things followed a logic of a perpetual Keynesian beauty circus chasing the lowest common denominator of big words, grand narratives and ultimately hollow promises.

Proof that one shouldn't ever relax assumptions in uncritically adopting/accepting the opinions of supposed experts and famous "smart people" or "influencers".

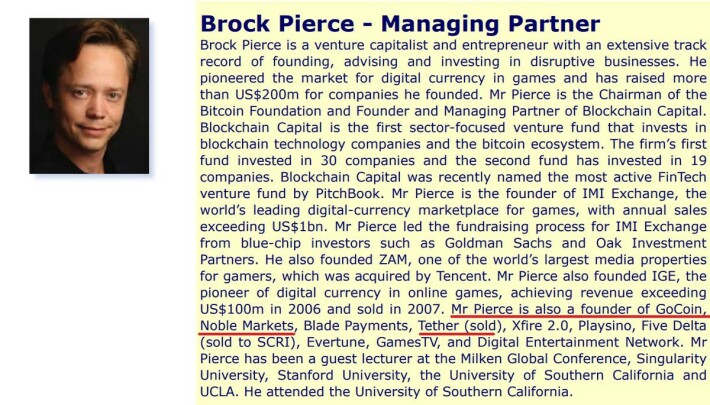

Tether's story begins with the specification of a second layer protocol for building other currencies on top of Bitcoin called Mastercoin. The technical specification of the protocol was published in 2015 and the protocol would become the technological foundation of Tether. Brock Pierce, not exactly unheard of by now, was one of the members of the Mastercoin Foundation and went on to become the co-founder of Tether with Craig Sellars (Mastercoin Foundation CTO at the time).

"If I need money, I just make a token."

-- Brock Pierce, co-founder of Tether, the Mastercoin Foundation and even at one point CSO of the EOS related Block.one

Initially announced as Realcoin in 2014, the project was officially renamed to Tether in November that same year. The company's website claims to be incorporated in Hong Kong with offices in Switzerland without providing any further details.

Bitfinex seems to follow in the steps of Mt.Gox in constantly accumulating bad karma and having been "hacked" a number of times itself already. The people running the exchange are also not the most savory bunch or people foreign to practicing financial fraud. How Tether had for some time been listed as USD instead of USDT on the platform is in itself saying. Bitfinex was also exposed to be directly associated with Tether and most likely running the Tether "printer".

Beginning 2015, crypto exchange Bitfinex introduced Tether on their platform and while representatives from both companies have persistently claimed that they are separate independent entities, the Paradise Papers leaks in November 2017 named Bitfinex officials Philip Potter and Giancarlo Devasini as responsible for setting up Tether Holdings Limited in the British Virgin Islands in 2014 (the BVI is notorious for its $1.5 trillion dollar off-shore economy providing the likes of Tether with a safe haven). According to Tether's website, the Hong Kong based Tether Limited is a fully owned subsidiary of Tether Holdings Limited.

At first, Tether was processing USD transactions through Taiwanese banks, using Wells Fargo as its partner bank for moving funds outside of Taiwan. This arrangement didn't last long since the relationship was severed in April 2017, blocking all international transfers. In June the same year Tether announced their launching of Tether/USDT as an ERC-20 on Ethereum and also introducing a Euro Tether alongside the USD "backed" token.

"We’re not criminals, but now we have to learn to bank like criminals."

-- Giancarlo Devasini, co-founder of Bitfinex in conversation regarding Tethers.

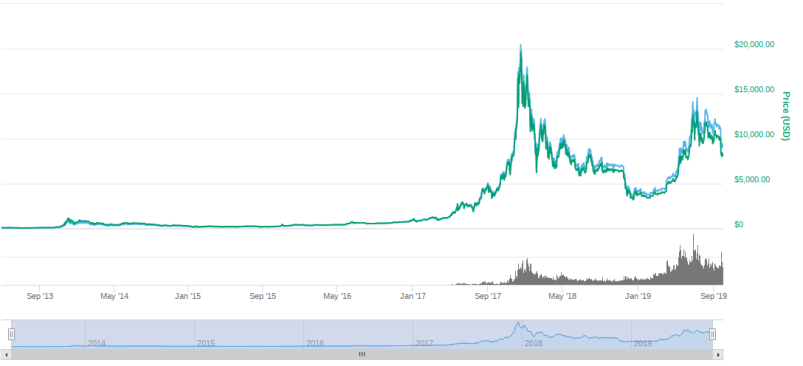

From Jan. 2017 to Sept. 2018 the amount of Tethers outstanding went from ~$10 million to to nearly $2.8 billion and then in early 2018 it was accounting for ~10% of Bitcoin trading volume going up to 80% by the summer that same year. Research suggests a market manipulation scheme had been set in motion, accounting for roughly half the price appreciation of Bitcoin in late 2017 (when it went from around 1k to nearly 20k USD in the interval of a few months). More than $500 million Tethers were issued in August 2018 and Bitcoin's sudden rises in price seem to be highly correlated with Tether issuance at the time.

The dramatic 2017 Bitcoin pumpathon. Peak is at 18 December 2017 at $18,734. An engineered bubble inflaming crowd sentiment and triggering the typically accompanying gold rush symptomatic to the phenomenon.

Needless to say, it never seems like a good idea to have a noncompliant crypto exchange of suspicious origins also have the levers for operating what basically amounts to an unregistered and unregulated money printing press and control the relationship of the entire market with the US dollar. The whole situation should immediately raise some red flags and call for further scrutiny, sober evaluation and asking of questions. (Although this mostly wasn't the case, with Tether instead showing no lack of apologists and defenders in Crypto-Twitter and only a handful few actually blowing the whistle and calling attention to the whole thing.)

A report/analysis of the events and the inflows/outflows of tokens/funds having taken place ("Quantifying the Effect of Tether") dating from January 2018 sums up the author's opinion so:

- Author’s opinion - it is highly unlikely that Tether is growing through any organic business process, rather that they are printing in response to market conditions.

- Tether printing moves the market appreciably; 48.8% of BTC’s price rise in the period studied occurred in the two-hour periods following the arrival of 91 different Tether grants to the Bitfinex wallet.

- Bitfinex withdrawal/deposit statistics are unusual and would give rise to further scrutiny in a typical accounting environment.

- If there is questionable activity, the author believes a 30-80% reduction in BTC price could be forecast.

This period of an artificially engineered bubble (with subsequent smaller bubbles) is in a crucial way what fueled the mass speculative crypto-craze euphoria and ICO fever, additionally inflamed by an avalanche of empty-promise ICOs (often not even making the effort to put together a convincing proposition/white paper, but hastily copy-paste hack-and-slash, plagiarizing from previous ones and mixing in some of the common marketing pixie-dust buzzwordery), absurdly exaggerated claims violating basic laws of physics and the public demonstrating of confident self-assurance grounded in the hard certainty of belief (as it is often the case that during such sudden and dramatic pumps or in the midst of a bubble, many are inclined to think of themselves as more intelligent than before, even geniuses sometimes, as they’d add “polymath” to the description of their Twitter profile).

In their white paper, Tether make two claims which proved to not hold at all:

"This method uses the Bitcoin blockchain, Proof of Reserves, and other audit methods to prove that issued tokens are fully backed and reserved at all times."

And:

"Tethers may be redeemable/exchangeable for the underlying fiat currency pursuant to Tether Limited’s terms of service or, if the holder prefers, the equivalent spot value in Bitcoin."

On the first point, Tether have made repeated assurances about making their reserve account holdings transparent via an external third-party audit made publicly available. However, as is known, such audits have never been provided and in the beginning of 2018 Tether announced they've severed their relationship with their auditor. On the second one, Tether Limited actually states in their terms and conditions that Tether holders really have no contractual rights or entitlement to any other legal claims, including no guarantee whatsoever that Tethers will ever be redeemed or exchanged for actual US dollars.

If we stop for a moment and consider the entangled market correlations involved in this arrangement, it's easy to recognize the gravity of the problem. The entire crypto-currency market is heavily correlated with Bitcoin and more or less moves with it. That in itself doesn't make much sense, but it is largely the consequence of how centralized exchanges operate (which have often been themselves complicit and colluding, as well as regularly engaging in wash trading and faking of volume).

In other words, whatever crypto you might hold, it's really actually denominated in BTC and not USD (i.e., whatever you're holding, you're really for all intents and purposes holding BTC). And the way CMC displays values, it's never quite entirely clear how these are calculated and derived, on the basis of what factors and data feeds (there's obviously no unified mechanism for establishing a common price of BTC across all markets) -- not to mention that the notion of market capitalization in these markets is also itself misleading and problematic.

And at some point, trading of Tethers enters and people trade them just how they would actual US dollars, tainting the price of everything in the process and turning the entire market toxic. And if one goes on to look into the Tether matters even closer to discover the kinds of unsavory folks and criminal associations involved in this scheme... it's really not surprising. And it also becomes ever more weirder. Corrupt judges, Ukrainian oligarchs, casinos implicated in money laundering and human trafficking operations, financial fraud in particularly sizable amounts and more.

Co-founder Brock Pierce had his own 'bank' in Puerto Rico (Noble International controlled through Noble Markets) which is at the same time the bank Tether uses. Buying small community banks in loosely regulated jurisdictions with weak controls and endemic corruption is a favorite activity of money launderers.

All in all, and given how Tether Limited operates as a centralized custodian of the reserve assets, this relic of times now by-gone must somehow be disassociated from if crypto is to mature as an efficient market to be taken seriously. Yet, perhaps inevitably, the majority of exchanges trade pairs with Tether.

Future Prospects and Expected Developments

In April 2019 NY Attorney General Letitia James filed a lawsuit against Bitfinex accusing them of using Tether's reserves for a cover-up for a $850 million loss. Since Bitfinex hadn't been able to secure normal banking relationships, reads the lawsuit, it went on to deposit $1 billion with a Panamanian payment processor known as Crypto Capital Corp. Oddly, no legally binding contract was ever signed with Crypto Capital and they're said to have not long after disappeared with the money and investors had never been informed of the fact.

Alliance of American Football investor Reggie Fowler, said to be closely associated with Crypto Capital, was indicted on April 30, 2019, for "running an unlicensed money transmitting business for virtual currency traders". He is believed to have failed to return about $850 million to an unnamed client. Investigators also seized $14,000 in counterfeit currency from his office. And in 2019 Bitfinex went to shamelessly launch yet another ICO (the LEO utility token, entitling holders to some benefits and privileges on Bitfinex) in hopes of managing to keep the boat afloat awhile longer compensating some of the stolen funds to calm things down a little.

The LEO token is #11 by market capitalization. Must be kept in mind that without much liquidity or in stagnant markets, market cap is an unreliable and misleading metric since the way its calculated is multiplying the circulating supply of an asset by how much it was bought for in the latest trade having taken place. Thus making it too easily gamed.

At this point there should be no possible twist of reasoning or logic, no half-truths left to cherry pick or fabricated reassurances to pull that could make a case in justifying Tether and Bitfinex in their actions and conduct (as we've observed in the occasional Crypto Twitter debate). And not only that but it turns out that what these series of inter-related companies, legal entities, individuals and relationships appears to reveal is criminal networks of cooperativity -- criminal in every sense of the word that is (as defining of a criminal thinking mindset and intentions, legal, ethical, moral, etc.). But also and just as disturbingly the presence of some very well connected and influential individuals among them makes an impression. People with extensive experience in the financial engineering of sizable fraudulent schemes, operating dirty money laundries, soaked in corruption, etc.

In retrospect, it really isn't that unusual that Bitcoin in its earlier days would be such an attractor for the likes of just such people. We remember how in the first years of its existence Bitcoin was mainly taken up as the means of exchange in the murky waters of darknet marketplace bazaars for illicit goods (both digital and physical, mostly drugs and pharmaceuticals and stolen credit card information). That itself reflective of the distinctively libertarian attitude and politics that permeated the movements and culture Bitcoin was born from, if one grounded in a somewhat more extreme and anti-statist end of the political spectrum.

American-style libertarians abound on the Internet. Computer programmers are highly susceptible to the just world fallacy (that their economic good fortune is the product of virtue rather than circumstance) and the fallacy of transferable expertise (that being competent in one field means they’re competent in others). Silicon Valley has always been a cross of the hippie counterculture and Ayn Rand-based libertarianism (this cross being termed the “Californian ideology”).

Meanwhile, as the circle around Tether and Bitfinex tightens and the arsenal of dirty trick moves and tactics for buying time is getting fast exhausted, Tether keeps on printing its regular batches of millions of Tether tokens and releasing them on the market. The original claims of being 100% backed, every token with a corresponding US dollar in reserve, has also been revised to claiming to be in possession of 74% or so, in US dollars, equity and other unspecified "money equivalents". The Tether controversy is really an ideal point of departure for beginning to get some realistic sense of the kinds of machinations that may be taking place behind the illusion that gets projected through the medium of technology.

Further Resources and References

Bitfinexed at Medium (his series of blog posts exposing the Tether/Bitfinex fraudulent schemes in more detail and depth) and his Twitter account.

The Tether white paper. (In many ways not corresponding to present facts.)

Some disturbing investigations into Tether's associations and networks by Bennett Tomlin in a blog post of his.

Omniexplorer, the explorer for tracking Tether movements on the Omni overlay.

Tether ERC-20 on Etherscan.

The LEO ICO white paper value proposition.

A very informative and insightful analysis of systemically important cryptocurrency networks from the perspective of fintech in the real world by Tim Swanson (coining the expression "matryoshka stablecoins").

"The Tether Saga, Illustrated Timeline", a Hackernoon blog post by Alex Krüger.

-- @rhyzom (Martin B.)