The idea that news moves markets is so deeply embedded in how people think about investing that questioning it feels contrarian. Every trading desk has Bloomberg on a screen. Every algorithmic fund pays for high-speed news feeds. Every retail investor has, at some point, rushed to buy or sell something because of a headline they just read.

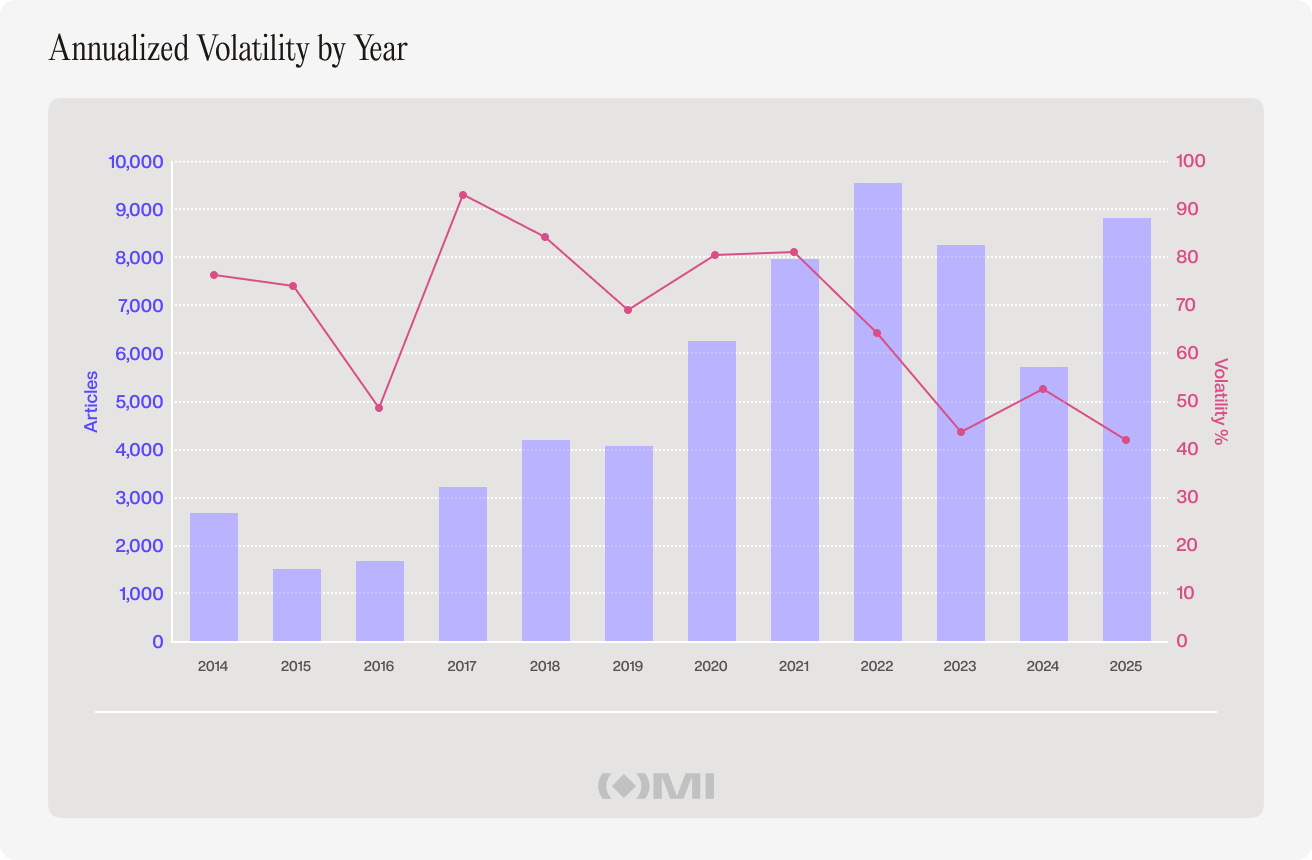

In crypto, this instinct runs even deeper. Bitcoin trades around the clock, every day of the year. The media ecosystem around it has grown from a handful of hobbyist blogs in 2010 to a sprawling industry producing dozens of articles daily.

When Bitcoin crashes, the headlines multiply. When a new law gets approved, the price surges. The two feel connected, and they do look connected.

But looking connected is not the same as being connected, and the direction of influence matters enormously. If news genuinely causes price movement, then reading faster and reacting sooner is a viable strategy. If price movement causes news, then the media is just a mirror reflecting what has already happened. And if neither causes the other, if they simply respond to the same underlying events with different timing, then the entire concept of news-driven trading is a cognitive illusion.

That is what we set out to test.

What we did

We collected 63,926 headlines from CoinDesk published between January 1, 2014, and December 30, 2025. We then matched them against daily Bitcoin closing prices from the TradingView composite index, which aggregates data across major exchanges into a single reference rate. That gave us 4,381 days where both a headline count and a closing price were available.

The choice of CoinDesk as the sole source was deliberate. CoinDesk is the crypto industry’s longest-running major publication, with consistent editorial output spanning the entire study period. Unlike outlets that focus narrowly on token prices, CoinDesk covers the full spectrum: regulation, macro, institutional flows, technology, and market structure. This breadth makes it a reasonable proxy for the overall media environment a market participant would be exposed to.

We acknowledge that a single source cannot capture the full universe of crypto media influence, and we address this in the limitations section.

The dataset covers two complete halving cycles, three major bull markets, three catastrophic bear markets, including the COVID crash and the FTX collapse, and the spot ETF approval of January 2024. If a relationship between news and price exists anywhere, this dataset should reveal it.

We tested the relationship using four separate methods.

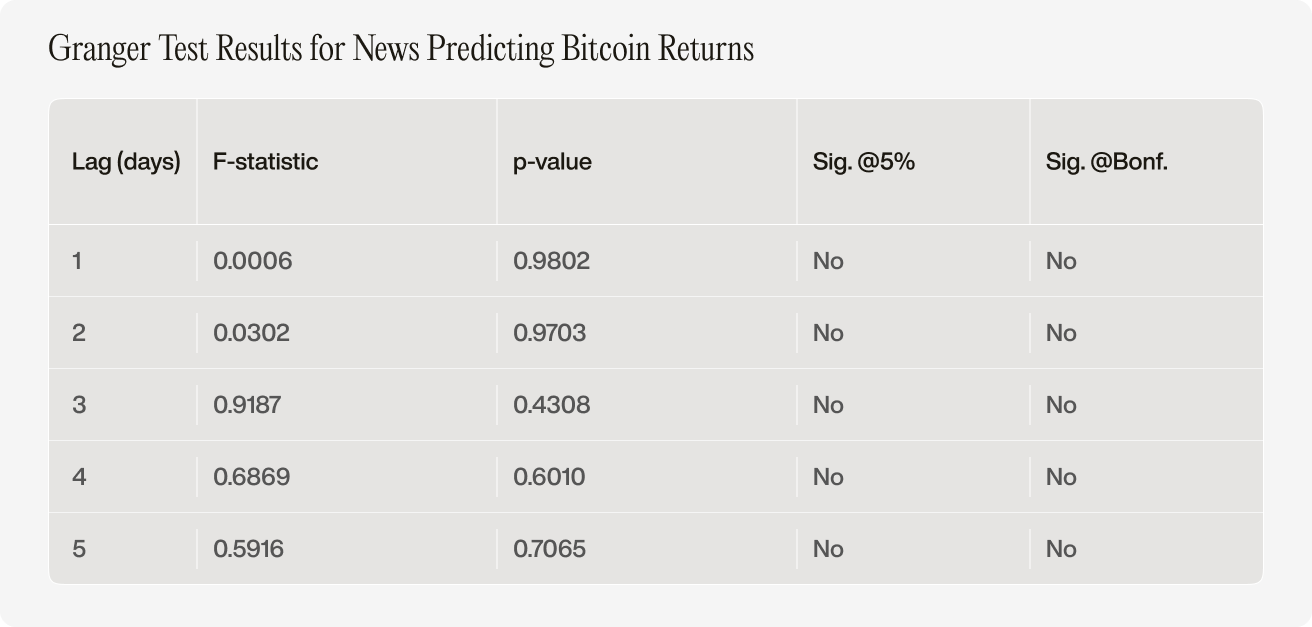

First, Granger causality, which asks: Does knowing yesterday’s news help you predict today’s price?

Second, an event study that tracks what Bitcoin’s price actually does in the days around major news spikes.

Third, a sentiment analysis using an AI model trained on financial language, which scored every headline as positive, negative, or neutral and checked whether the day’s tone predicted returns.

And fourth, a topic analysis that classified what the media was actually writing about on its busiest days.

Key takeaways

-

News does not predict Bitcoin’s price. We tested it across five different time lags, in both directions, and the result was zero.

-

If anything, price predicts news. Bitcoin tends to rise in the days before a major coverage spike, then drifts down afterward. The media reacts to markets, but it does not move them.

-

Headline sentiment is meaningless for trading. Whether a day’s coverage is bullish or bearish explains about half of one percent of what Bitcoin does next. The relationship itself flips direction every few months.

-

Most crypto news is noise. On peak-coverage days, 61% of headlines are general industry content with no identifiable price link. The only major category that could plausibly cause price moves, regulation, still fails to produce a tradable signal.

-

The market knows before the headline drops. By the time a story appears on a major outlet, the information it contains has already traveled through faster channels: order flow, on-chain data, social media, and insider networks. The headline is the last mile.

News does not predict price

The first test we ran, Granger causality, is the standard statistical method for determining whether one series helps forecast another. Think of it this way: if you build a model that uses only Bitcoin’s own past returns to predict today’s return, and then you build a second model that adds yesterday’s news data on top, does the second model do any better? If it does, news has predictive power. If it doesn’t, news adds nothing.

We ran this test across five different time horizons: Does today’s news predict tomorrow’s price? What about two days out, three, four, five?

In every single case, the answer was no. At the one-day lag, where the intuitive case for news-based trading is strongest, including news data in the model performed no better than random noise.

The raw correlation confirms this. When we compared daily changes in article volume to daily Bitcoin returns, the correlation was 0.019. That means changes in how much the media publishes explain roughly 0.04% of what Bitcoin does on any given day. For all practical purposes, that’s zero.

The takeaway: No matter how you slice the data, news volume carries no information about where Bitcoin’s price is going tomorrow. The most commonly assumed mechanism in crypto trading, reading today’s news to anticipate tomorrow’s move, does not hold up.

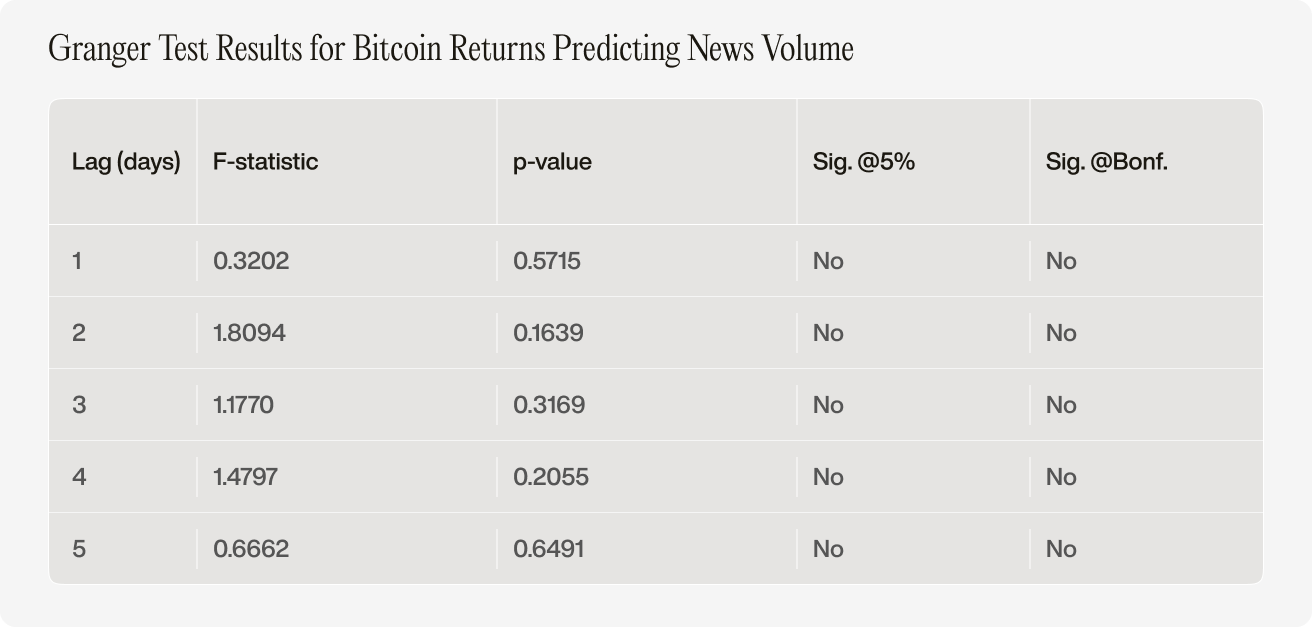

Price leads news

Testing the reverse direction, whether price movements predict future news volume, was marginally more interesting. The strongest result appeared at a two-day lag, hinting that a big price move on Monday might generate editorial meetings on Tuesday and published articles on Wednesday. But hinting is not demonstrating. The result still fell well short of conventional significance thresholds.

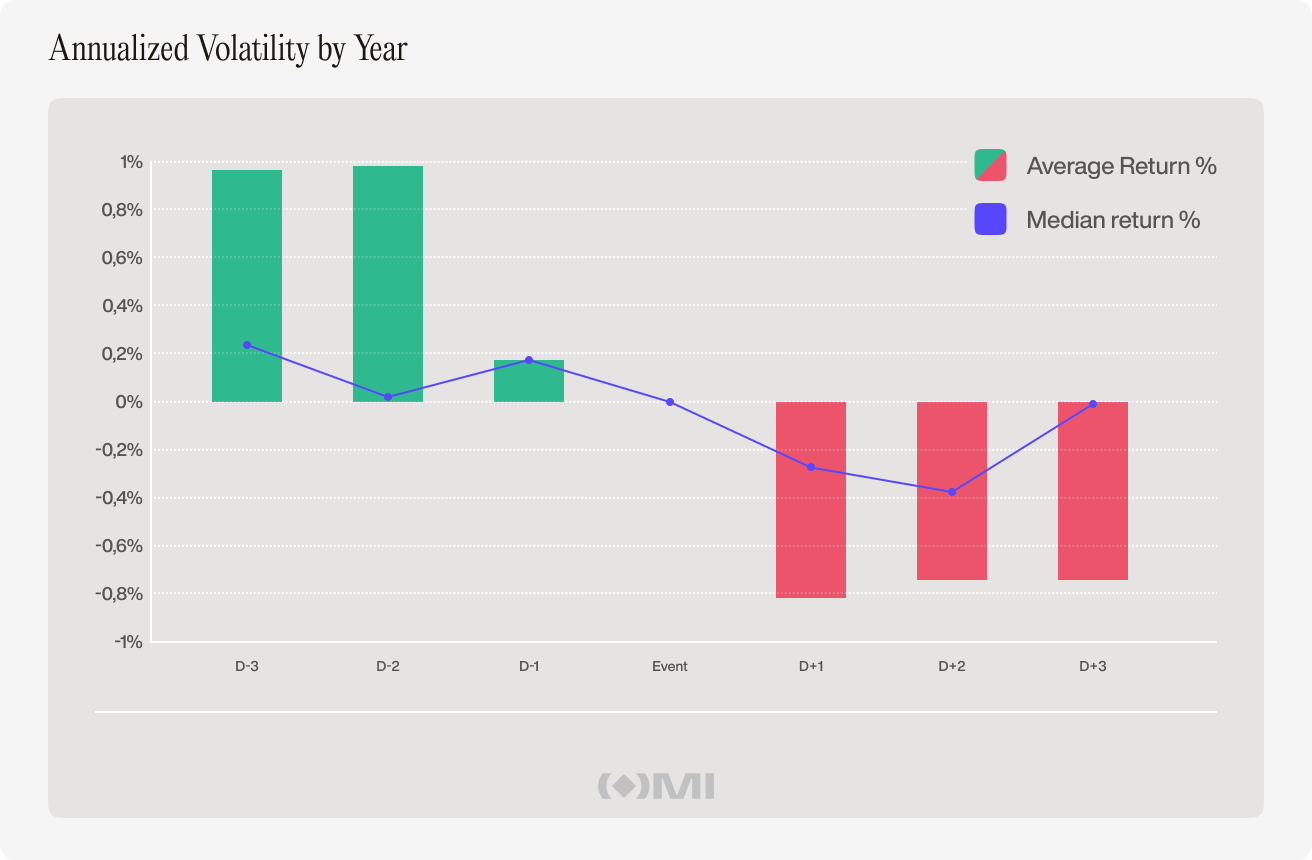

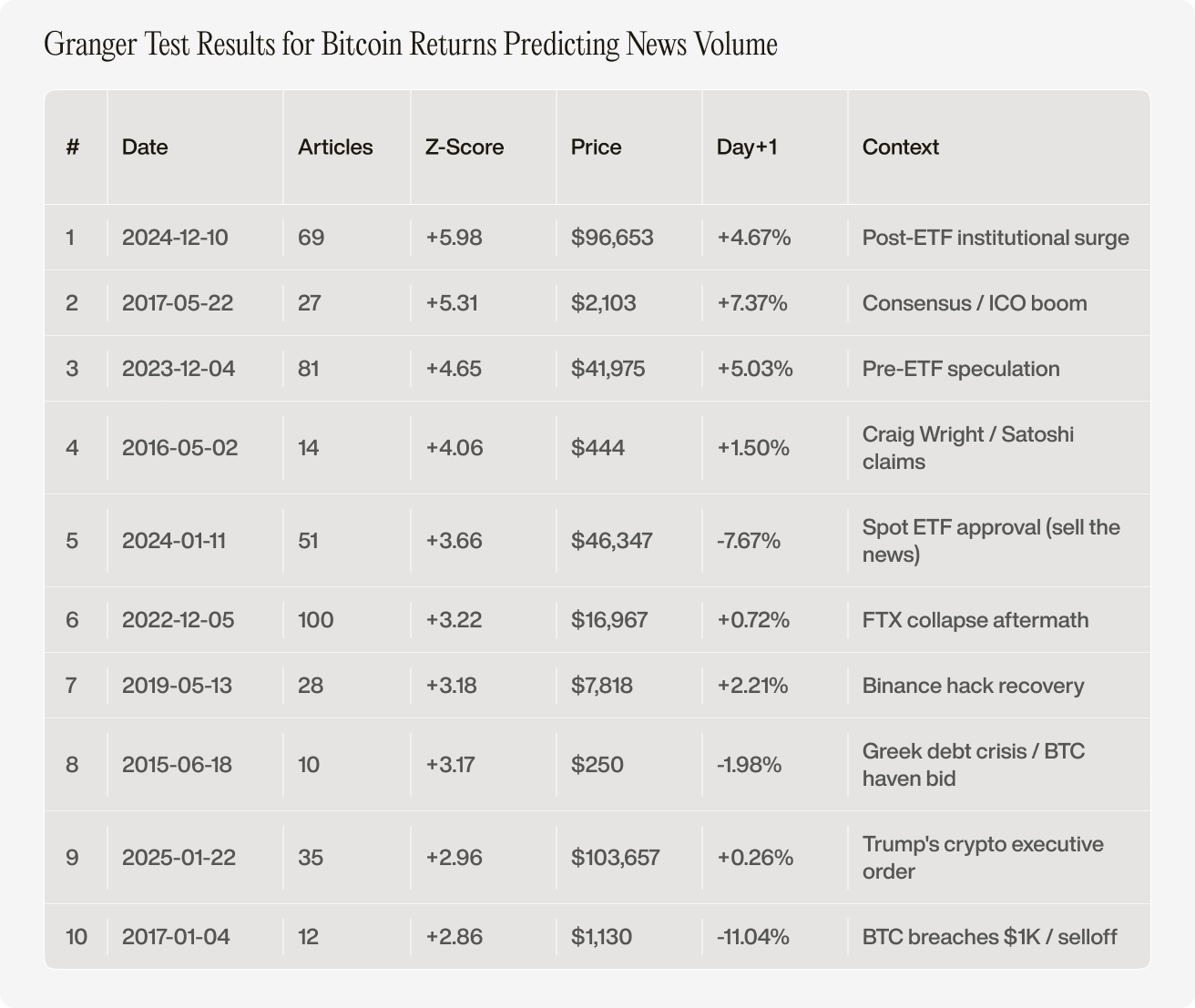

We then identified the 50 most extreme news days in the dataset, measured by how far above or below the recent average each day’s article count fell, and then tracked Bitcoin’s price in the three days before and three days after each spike.

The pattern is consistent and asymmetric. In the three days before a major news event, Bitcoin’s price is already elevated, averaging about 1% above the event-day baseline. Then the news hits. And then the price drifts down: about 0.8% on average by day three.

The interpretation is quite straightforward. Journalists see a price move and write about it. That creates a natural lag between what the market does and when the coverage appears.

And news spikes coincide with the resolution of uncertainty: a price that has been climbing for days on rumors or insider knowledge becomes “official” when the headline drops. At that point, the information is priced in, the marginal buyer disappears, and the price drifts back.

In both explanations, the news is the last thing to arrive.

The takeaway: The data suggest that prices move before news rather than after. The media reports on what happened. It does not cause what happens next.

The stories behind the numbers

Take January 11, 2024. The SEC approved the spot Bitcoin ETF, the most anticipated regulatory decision in crypto history. CoinDesk published 51 articles that day. Bitcoin dropped 7.67% the next day. By day three, it was down 10%.

It was the biggest news event in crypto, and the price went the wrong way.

But the data tells us why. A month earlier, on December 4, 2023, when ETF speculation was at fever pitch, but nothing had been confirmed, CoinDesk ran 81 articles. Bitcoin rose 5% the next day. The market had already priced in the approval weeks before it happened.

The actual announcement was confirmation of what informed participants already knew. Classic “buy the rumor, sell the news.”

Or consider January 4, 2017. Bitcoin had just breached $1,000 for the first time since early 2014. The media celebrated with a dozen articles. The next day, Bitcoin fell 11%. By day three, it was down nearly 20%.

The headlines were celebrating a milestone the market had already moved past.

Then there is December 5, 2022, the single busiest news day in the entire twelve-year dataset: 100 articles, all in the aftermath of the FTX collapse. The next-day return was just a modest +0.72%. By the time 100 articles had been written, every ounce of the FTX shock was already embedded in the $16,967 closing price.

Across all ten of the biggest news events in the dataset, the pattern holds. Three produce next-day gains above 4%, two produce losses exceeding 7%, and the rest scatter in between. The volume of coverage tells you nothing about what comes next.

The takeaway: Even the biggest, most dramatic news events in crypto produce wildly inconsistent price responses. The ETF approval caused a crash. The FTX aftermath caused barely a ripple. The volume and intensity of coverage have no reliable relationship with what Bitcoin does next.

Sentiment doesn’t help either

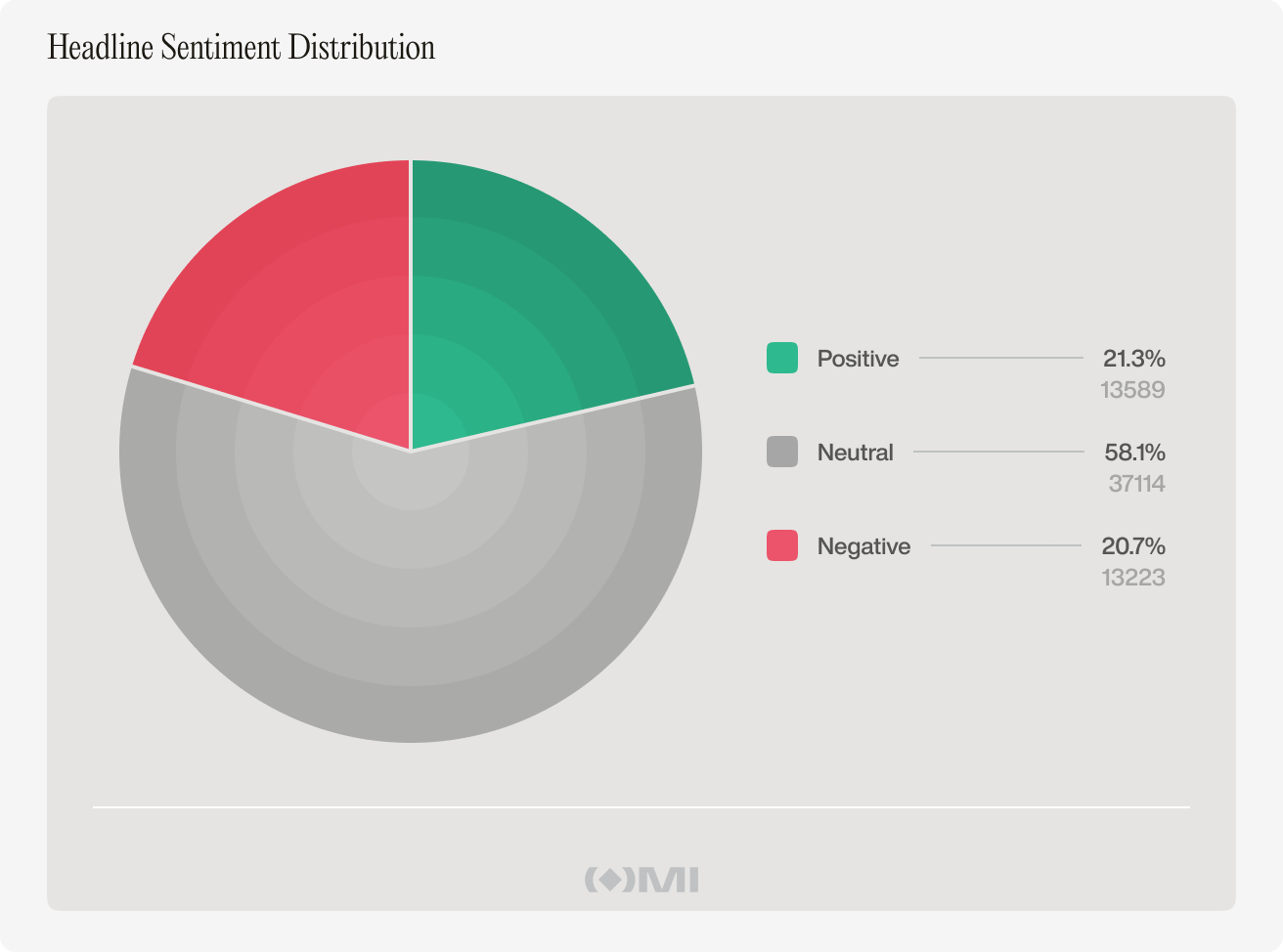

We ran every headline through FinBERT, an AI model specifically trained to classify the tone of financial text. It scored each headline as positive, negative, or neutral, and we averaged those scores across all articles published each day to create a daily sentiment reading.

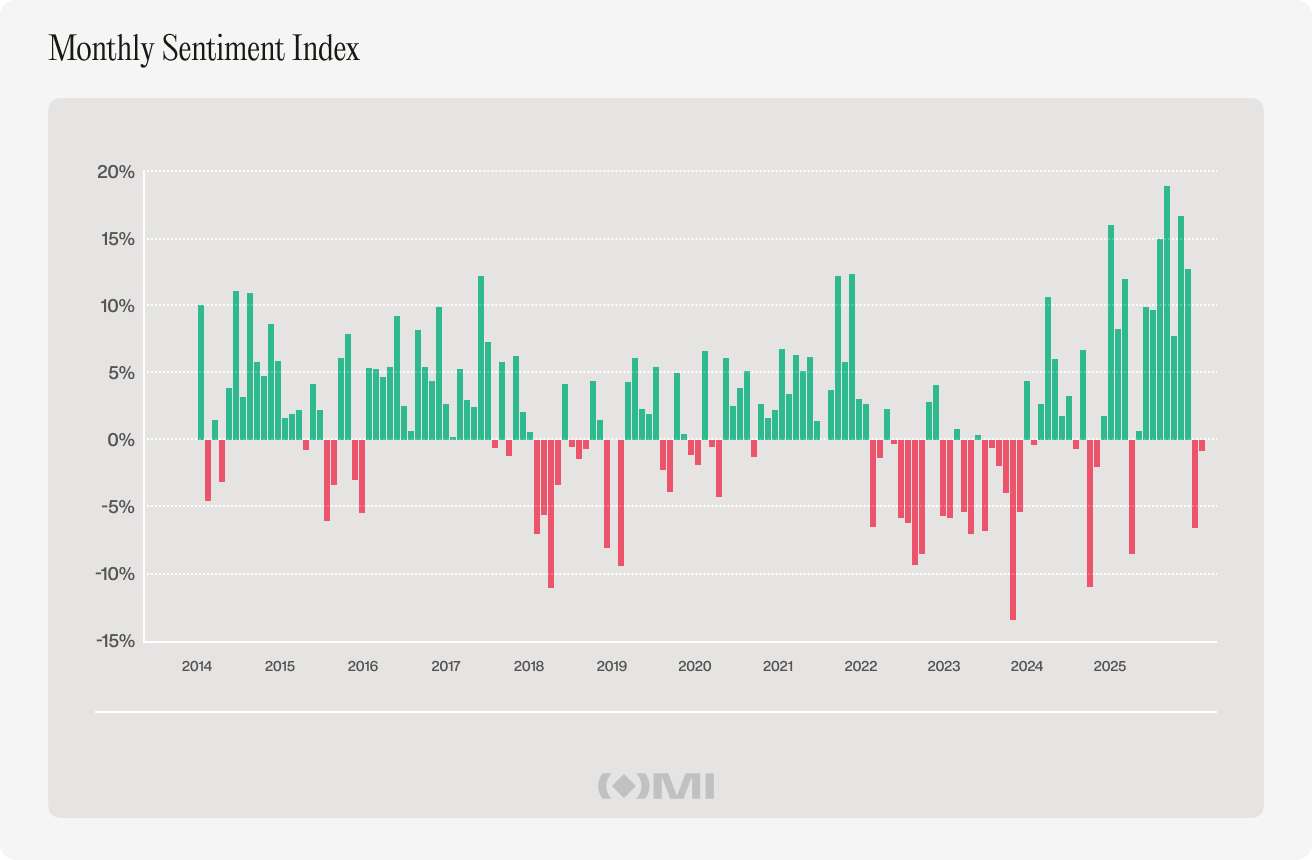

Across the full dataset, CoinDesk’s coverage turned out to be quite balanced: 58% neutral, 21% positive, 21% negative. But whether coverage on any given day was bullish or bearish had almost no relationship with what Bitcoin did. The correlation between daily sentiment and daily returns was 0.07, meaning sentiment explained about 0.5% of price movement.

What is worse is that this already tiny relationship is unstable. When we measured the correlation in rolling three-month windows, it swung from negative (sentiment and price moving in opposite directions) to positive (moving together) with no consistent pattern. There is no stable signal to trade on.

This makes sense once you think about what the AI is actually reading. A headline saying “Bitcoin falls below $40,000” gets a negative sentiment score, but the price decline it describes is already reflected in that day’s closing price. The sentiment measure is partly just echoing the price move it’s supposed to be predicting.

The takeaway: Headline tone contains essentially no usable information about future returns. The relationship is tiny, unstable, and likely reflects prices influencing language rather than language influencing prices.

Most crypto news is noise

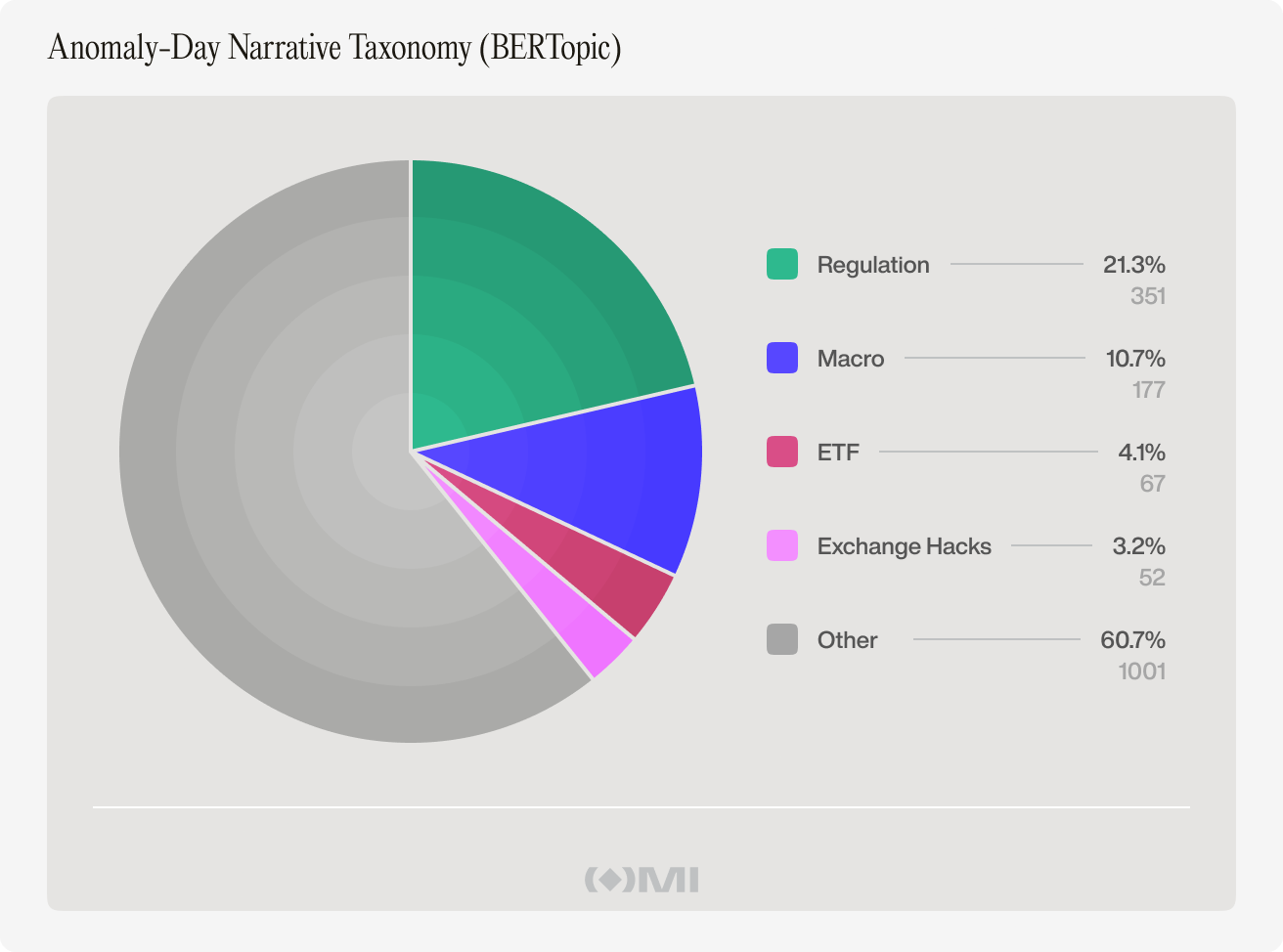

We used a clustering algorithm to sort the headlines published on extreme news days into thematic groups. About 61% of peak-day coverage is general industry content: blockchain partnerships, startup fundraising rounds, stablecoin updates, NFT developments, and Web3 gaming. None of it maps onto any identifiable price signal.

The single largest identifiable category is regulation, at about 21%. SEC enforcement actions, crypto legislation in various countries, and banking rules. This is the one category where you might expect a clean causal relationship with price, because regulatory announcements are genuinely external events: they are not caused by Bitcoin’s price. The fact that even regulation fails to produce a systematic price signal in the data tells us that the news-to-price channel is either too noisy to exploit at a daily level or genuinely absent.

Perhaps the most surprising result is what didn’t appear at all. The halving, widely considered the most important fundamental driver of Bitcoin’s long-term price, produced zero identifiable clusters among the extreme-day headlines, despite two halvings occurring during the study period. The media appears to treat halvings as slow-burning background stories rather than acute events. Either way, the most discussed driver of Bitcoin’s price operates through channels that have nothing to do with daily news cycles.

The takeaway: On the days when crypto media output is highest, the vast majority of coverage is thematically diffuse industry noise. Even regulatory news, the strongest candidate for genuine causal impact, does not produce a tradable signal.

Why these findings matter

These findings matter because the opposite belief is so widespread. Hundreds of millions of dollars have been invested in news-based trading signals, sentiment platforms, and algorithms that ingest headline feeds and trade on their content. This study doesn’t suggest those platforms are fraudulent. It suggests they are solving a problem that may not exist at the daily frequency.

By the time a headline appears on CoinDesk, the information it contains has already traveled through faster channels: order flow, on-chain data, social media, insider networks, and algorithmic pattern recognition. The headline is the last mile of an information relay. Trading on it is like reading yesterday’s weather report to decide whether to bring an umbrella.

This does not mean news is irrelevant to crypto in every sense. At much shorter time scales, measured in minutes, breaking headlines might create brief windows that a daily study like this one cannot detect. At much longer time scales, multi-week narrative shifts like the gradual build of ETF anticipation through late 2023 could influence prices through slow-moving channels that our methodology is not designed to capture.

What the data shows is that the most commonly assumed mechanism, today’s headlines influencing tomorrow’s price, does not hold.

Limitations

The dataset uses CoinDesk as the sole headline source. While CoinDesk’s breadth and longevity make it a strong proxy for the broader crypto media environment, social media channels like X, Reddit, Discord, and Telegram may carry more immediate price-relevant information than traditional outlets, and those are not captured here.

The daily frequency of analysis may also be too coarse. If a major headline moves Bitcoin’s price by 3% within 30 minutes of publication and the price then reverts over the remaining 23 hours, the daily closing price would show no effect. A study at minute-level resolution might reach different conclusions.

The sentiment model classifies headlines based on language patterns rather than deep understanding. It cannot distinguish between a crash caused by genuine fundamental deterioration and one caused by a brief liquidity squeeze that reverses within hours.

And the news-price relationship could be nonlinear: news might matter only when sentiment reaches extreme levels, or only when headlines conflict with the prevailing market trend. Our tests look for consistent, linear relationships and would miss these conditional effects.

Conclusion

The noise and the signal are not the same thing. The noise is abundant, relentless, and superficially compelling. The signal, to the extent it exists, has already been absorbed by the time the noise reaches your screen.

Twelve years of data, four analytical frameworks, and 63,926 headlines all point to the same conclusion: the market knows before the headline drops.

P.S. This article first appeared on OMI Blog.