Authors Note: This is another interesting junction for me, since corporate analysis and statistics aren't really what I normally would post here. Yet, while my articles on Seeking Alpha are exclusively-tied, here I'd like to share one that's complimentary, and could be an interesting way to pass on time. In any case, I hope you enjoy the read :-)

And if you're wondering - No, this isn't a sponsored article.

In the age of globalising economies and changing trends in consumerism, much of our thoughts often gravitate towards those large, recognisable companies which have become the staple for human attention, and have made themselves the source of supply and demand. Whether its Apple, Rolex, or Ferrari, these venerable brands always dominate the front page of very news headline, and so much is the case that we often forget of smaller, less-recognisable brands.

It's noted that over 90% of the world's registered companies are classes as SMEs, or small and medium enterprises. While each country has their own definition for what classifies as SMEs, they all have the same modest construct, with small foundations to build upon, and large dreams ahead. Contrary to large corporations, SMEs have always had the natural advantage of nimbleness and focus - think then of the difference between a luxurious and lumbering Rolls Royce, compared to a lightweight and single-minded Lotus.

Yet, SMEs have always had key flaws that can often put their businesses of shaky grounds. Compared to listed companies, SMEs have little in the ways of acquiring additional capital, as it does not have the umpteen investors who are willing to hand in a blank cheque. SMEs may also lack the diversity in their business model to accommodate for the changing general trends around the world, thus leaving a small margin for error in running out of business.

The perfect business template then is a mixture of these two combined - with the small, agile, and focused structure of an SME; and with the diversification and capital that could be expected of a large, listed corporation. I have spent some time reading into new and interesting companies, and I have thus far failed to find that perfect blend, until only recently.

Perusing through the depths of new developments in the world of suit and tie, I have come across MBH Corporation, a company which has managed to find the Goldilocks Zone of business.

Source: MBH Corporation

The who, what, where and when.

You might be asking then, who is MBH Corporation, and what is it that they've done so differently?

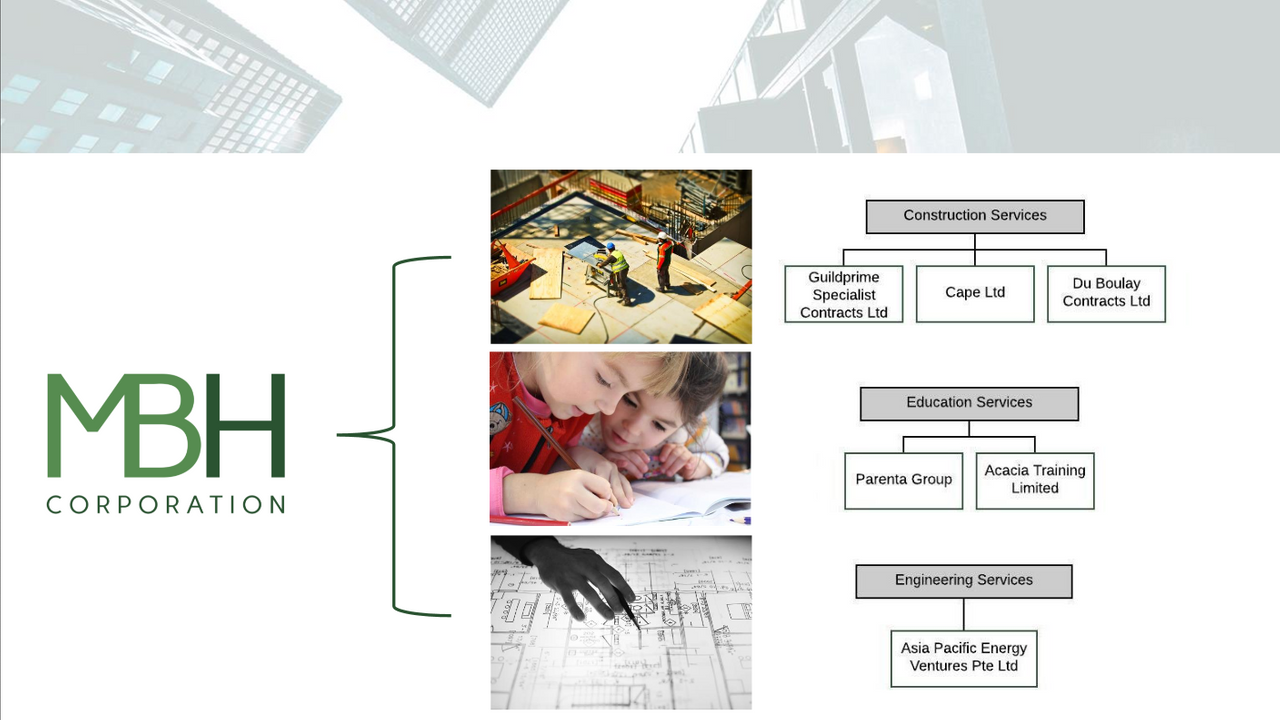

For a start, MBH Corporation is a diversified investment holdings company which uses an in-house and proprietary methodology of Agglomeration™ for deciding and making acquisitions of profitable and potentially breakthrough small and medium enterprises, and is itself a "Buy and Hold" strategy (or Hodl). The key difference - is that MBH offers those SMEs its own shares for acquisitions, thus allowing for private companies to have the benefits of trading as a larger listed group, hence providing these smaller companies a platform and ecosystem for continued growth.

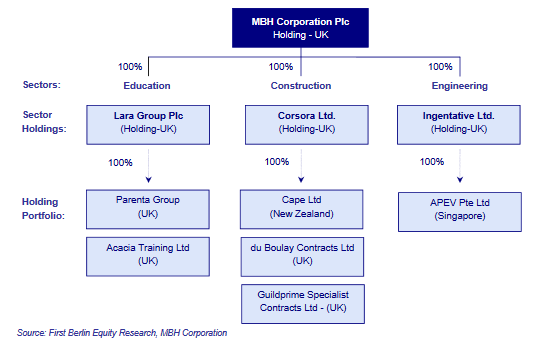

MBH's Holding Structure. Source: MBH Corporation

Alternative view of MBH's Holding Structure. Source: First Berlin Equity Research

The company's expansion has rapidly accelerated, especially since early-2019. Its largest acquisition was Asia Pacific Energy Ventures Pte Ltd (APEV) on June of 2019, which enabled MBH to enter a new industrial segment - energy services. Accordingly, MBH's 1-year pro-forma revenue growth is also shown within specific segments within the portfolio, with its educational services having grown from only GBP 0.4 million to GBP 10.2 million, and an addition of GBP 54 million for its APEV's acquisition.

MBH was incorporated in 2016 and does business in 4 different sectors: education, construction, engineering/energy, and telecommunications, media, and technology (TMT). Presently, MBH Corporation has 9 companies under ownership, where 6 were acquired within the first half of 2019 alone. It is based in the United Kingdom, while its shares are listed on the Frankfurt, and Duesseldorf stock exchanges since late-2018.

Source: MBH Corporation

MBH's full year performance between Q4 2018 and Q4 2019 has shown strong growth for the company since its listing. Its 9 companies under ownership have together generated a pro-forma revenue growth of +189%, from GBP 37 million (December 31, 2018), to GBP 107 million as of October 2019.

While pro-forma revenues do not comply with GAAP standards, it can show a clearer picture as to the company's true growth. Moreover, its standardised EBITDA earnings report for all 9 companies combined have shown a 1-year growth from GBP 3.3 million to GBP 9.9 million, a 200% year-over-year growth.

MBH's unique Agglomeration™ strategy allows the businesses under its ownership to organically grow their privately-owned SMEs with all the benefits provided of a listed-company, thus giving access to capital raise and investor funding, with plans to have between 15 to 20 more companies joining its portfolio in 2020.

Source: MBH Corporation

MBH's Agglomeration™ model was best described by First Berlin Equity Research;

"Small & Medium Enterprises are not easily accessible to investors, as they may be too small, illiquid, or too time-consuming to audit. MBH's stock overcomes these obstacles by allowing public investors to have exposure to smaller companies with good growth."

Furthermore, investors also benefit from the diversification offered by MBH through direct investment in key SMEs, and through future portfolio expansions by strategic acquisitions that will only better increase diversification, while at the same time minimising risk.

Future acquisition plans by MBH. Source: First Berlin Equity Research

So, how does this all work out?

MBH's acquisitions are done with transactions made with 100% MBH stock, thus aligning their business focus and strategy based on increasing earnings-per-share (EPS) and shareholder value. As MBH is using their stock as currency for SMEs undergoing acquisition, there is a commitment for both parties to cooperatively increase MBH stock value altogether, thus naturally incentivising both the parent and subsidiary to find a common language to work with.

Source: MBH Corporation

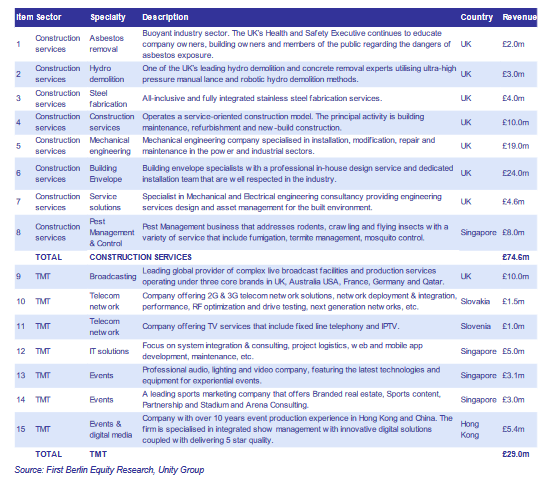

Each acquisition is expected to enhance shareholder value, as SMEs are acquired and put into MBH's portfolio only if they are EPS-accretive. Based on First Berlin's report, the current planning shared by MBH shows a potential of at least 15 more companies joining its portfolio soon, with a forecasted combined pro-forma sales of GBP 103.6 million (GBP 74.6 million for construction services, and GBP 29.0 million for TMT), and MBH's management commits to a risk-moderated strategy of making acquisitions at no more than 5x EBITDA, and preferably into debt-free SMEs.

Its stock has not done too terribly well, as investors who bought the stock a year ago would've lost 56% of their value. However, as MBH is a fairly new listing, some time would be needed before the public can see the company at its stride, and for the stock to reflect that. As such, volatility with early listings are expected for any company.

MBH stock (M8H:Xetra), Source: investing.com

What's in store for the future?

Source: MBH Corporation

MBH's companies under ownership compliment each other well, with MBH providing and encouraging catalyst for growth and synergy between them. With a consolidating global economy, there becomes the need for its infrastructure to match the needs to power future economic growth, and its where MBH's construction, and energy services could help to meet demand, thus increasing further prospects for growth.

MBH's construction services provide commercial, retail, and residential fittings and refurbishments. It provides the need for quality interior refurbishments to match against the growing tide of e-commerce, which many people anticipate to decimate brick-and-mortar stores, but is still crucial and depended upon for different good and services in the commercial space, and remains popular today.

With energy demands growing alongside an expanding human population, MBH's industrial companies are prime for further growth, and its smaller size and more nimble company structure allows for them to better position against the changing tides of corporate strategies, all revolving around the needs for sustainable and responsible growth, with respect to the environment and human life.

One scenario that could display MBH's future potential is within the emerging economy of Papua New Guinea (PNG).

Source: MBH Corporation

Around the mostly untapped emerging market of PNG, the energy sector is generating a majority of the country's export earnings. Alongside the Asian Development Bank (ADB), the largest development partner for PNG expects to increase funding for development. Increased economic support from multilateral partners will help to grow the country's energy industry further, corresponding with economic growth elsewhere.

Hence, with a soon-to-grow energy sector in PNG, and a corresponding economic growth forecasted, there too will be the need to expand infrastructure. Here, MBH's construction services can help to move in, by providing modern refitting and refurbishment for PNG's commercial, retail, and residential sectors, with an especially interesting outlook for Cape, MBH's New Zealand based contractor with GBP 20.09 million in revenue for 2018.

Source: MBH Corporation

Meanwhile its educational services, among its earlier acquisitions, have shown massive pro-forma revenues, and it provides award-winning vocational services training for the industry, with specialties in business software. There is a growing demand for digitalisation in many companies, especially since many SMEs still use outdated and inefficient software to manage their companies, and also with specialties in the healthcare sector, where MBH's subsidiaries help provide education and staffing for Britain's NHS.

Source: MBH Corporation

With its future potential in play, there is also a healthy dose of risk to consider, especially surround the company's stock.

If MBH's subsidiaries underperform expectations, it could drive MBH's stock price lower, as is commonly expected, and possibly detrimental for MBH's future. As MBH uses its shares as the sole currency for further acquisitions, which is the bedrock for its future growth strategy, a low stock price could affect its operational abilities, since the success of all strategic and lucrative acquisitions to come are based on the holding company's share performance.

On a similar subject on stock price, there are concerns following the its value for shareholders. While MBH's management has made a strong commitment to enhance shareholder value by focusing on EPS-accretive investments following a risk-moderated strategy, there is potential that an acceleration of acquisition activity could dilute shareholders, as it prints more stock to dish out for buying new companies.

On a macro-economic level, fears of recession and Brexit could dampen hopes for MBH in the near future, as consumers and the industry are holding out on making any financially-heavy decisions. For MBH, this presents some risk for all its portfolio components. Its educational services are based in the UK, and provides for UK businesses and government agencies such as the NHS. With the uncertainty of Brexit, slowing employment could give MBH's educational services the cold shoulder.

Its construction and energy services could slow down as well, despite an accelerated 2019, and this again could be exacerbated with Brexit mood in the air. However, with MBH's diverse portfolio that stretches into Asia Pacific and Australasia, the more optimistic demand in those regions could upset any dampening in the UK and elsewhere.

MBH Stock. Source: Simply Wall St.

Earnings and Revenue Growth Forecasts. Source: Simply Wall St.

EPS Growth Forecasts. Source: Simply Wall St.

Financial Position Analysis (Short vs. Long Terms). Source: Simply Wall St.

MBH Balance Sheet (Assets = GBP 101.51 million; Liabilities+Equity = GBP 99.76 million; Red/Debt = GBP 1.36 million). Source: Simply Wall St.

Final Words.

MBH Corporation is an upstart and interesting company, one with bold visions and intriguing ideas for its path forward in a more complex corporate world. With projected revenues of GBP 62.25 million for FY2019 (a +397.6% surge from FY2018's GBP 12.51 million), projected EBITDA of GBP 7.5 million for FY2019 (a +416.67% rise from FY2018's GBP 1.8 million), along with a healthy debt-to-equity ratio of 4.5% and net positive cash flow - MBH presents as an incredible opportunity for investors looking into long-term growth, and is highly undervalued at its current stock price of EUR 0.63.

Thanks for reading! Tell me what you think about my posting of more analytical articles in the future, and is there are any companies that you may want me to review? While you're at it, follow along @zacknorman97 for more, coming soon :-)