The Netherlands has proposed one of the most controversial taxes in its history on unrealized capital gains for 2028: an annual tax on "paper gains", i.e., the investment at 36%, even if you don't sell it. This could affect:

- BTC and cryptocurrencies.

- ETF.

- Stocks.

- Bonds.

It does not apply to real estate, artwork, investments in startups, or anywhere there is no current market price. These investments are taxed only upon sale.

This law stems from a huge legal problem for the Dutch state. The previous system had been declared illegal. For years, the Netherlands taxed wealth with a fictitious return: the state decided how much you should have earned and taxed that. The Dutch Supreme Court (rulings 2021–2024) ruled that many people were paying taxes on returns they never earned, and this violated property rights, so the government had to overhaul the entire system. Although the Dutch government is not in crisis like France and Italy, it has a public debt of around 45-50% of GDP (very low by EU standards). The deficit is rising, and the Treasury estimates a €2.3 billion fiscal deficit without reform.

LIQUID ASSETS AFFECTED

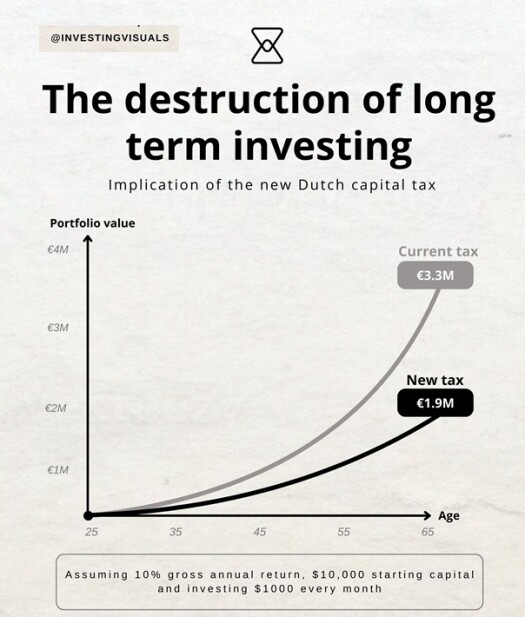

From 2028 (if the law passes as planned), all liquid assets will be taxed: cryptocurrencies, stocks, ETCs, bonds, deposit accounts, and dividends (even if they are not sold). The tax is 36%, with an exemption below €1,800 and the possibility of offsetting capital losses (from €500 and up) in future years. This offset is obviously not a refund of taxes already paid.

COUNTERFEITS

The snapshot is taken on December 31st of each year. When the tax is paid (May), those gains may likely no longer exist (due to market crashes), yet you still have to pay 36% to the state. Imagine having $100,000 in capital gains at the end of the year, and you'll pay $36,000 in taxes in May (even if that $100,000 has become $70,000 due to a crash). In addition to this major problem, the Dutch investor may be forced to sell some assets to pay taxes (losing the compounding effect over time and any future asset appreciation because you reduce the capital base by selling a portion of the investment). The system incentivizes less liquid and less productive assets (boats, yachts, works of art, luxury cars, etc.).

SOLUTIONS

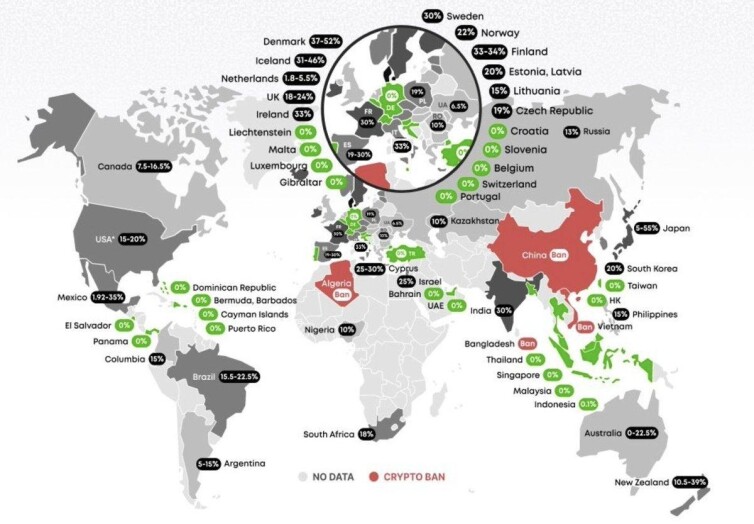

1) The main solution for many Dutch is to leave the country because the system hits hardest: long-term investors, the FIRE movement, passive accumulation in ETF and BTC. I read on X that the most discussed destinations are Belgium, Malta, Portugal (although less advantageous today), the UAE, and Switzerland.

2) I've read that some people talk about the possibility of circumventing the rule through a Dutch company (BV structure). However, from what I've read, a BV has a corporate tax (19–25%), and dividend taxes when you withdraw. There would be no annual personal tax, but administrative costs, anti-abuse rules, and future double taxation. This might only work for very large assets.

3) Others talk about moving toward "illiquid" assets that are taxed only upon sale: real estate, private equity, startup shares.

4) Moving toward luxury goods (art, yachts, collectibles), which, however, must be classified as personal use. If considered an investment, they fall under Box 3. Even if they don't have a certain market value, the investor can declare a lower value (using it as a capital loss). Although I imagine there are controls over: wash sales and unrealistic market valuations.

WHERE TO GO?

The government could still make some changes because the law is considered too controversial. A postponement beyond 2028 or a hybrid system between the old and the new is expected.

Upon closer inspection, a new Northern European tax model is emerging, which some economists (informally) call anti-compound taxation. Countries like the Netherlands, Denmark, Sweden, Finland, and Ireland have:

- very expensive pension systems.

- rapidly aging populations.

- fewer people working.

- large amounts of private wealth invested in financial markets.

As fewer and fewer workers pay taxes, capital grows autonomously in the markets. Over the past 15 years, thanks to global ETF and low interest rates, many private assets have begun to grow faster than GDP. From the government's perspective, compound interest creates an effect that is difficult to tax because if the worker is taxed annually on his income, the buy-and-hold investor can defer taxes for up to 20 years (a "tax deferral advantage").

All this worries governments because investing is much easier today than in the past thanks to global ETF, zero commissions, automatic accumulation, and even alternative payment systems without going through fiat (Bitcoin and Crypto). All this allows them to defer taxes or find alternative solutions without paying them. The state sees the rise of a class of people accumulating enormous capital without paying taxes. If no one sells, tax revenues collapse. This leads to annual taxes on assets (already present in Italy) and taxes on unrealized gains to raise revenue (often to cover debt and government mismanagement). The government's idea is to recover tax revenue, destroy compounding, and incentivize consumption rather than investment. However, this leads to other problems such as:

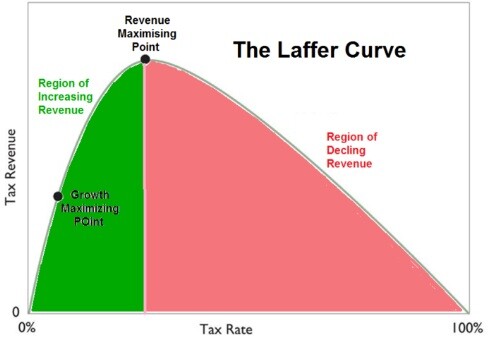

- tax evasion (the Laffer curve indicates that as taxes and aggressive fiscal policies increase, revenue decreases due to tax evasion/avoidance).

- less capital in public markets.

- less indirectly financed innovation.

- capital flight abroad.

Denmark already taxes foreign ETF annually, even if you don't sell them. Ireland has ETF with a "deemed disposal" regime: mandatory taxation every eight years even if you don't sell them. This, too, reduces the advantage of long-term compounding. With growing public debt, the Nordic model could expand elsewhere.

The question everyone should be asking is: can the state allow private capital to grow faster than the tax base?

Are you interested in ways to earn crypto bonus? Check it out here: Some Sites To Earn Crypto Bonus (Old & New)