When you place a stop loss, you're creating a barrier: if the price touches it, your trade closes immediately. This completely changes the distribution of your strategy's results: it's no longer "bell-shaped" but becomes distorted. The closer you place the stop, the greater the distortion, and the more likely it is that your trade will be closed due to normal market fluctuations. A stop loss that's too tight makes your strategy fragile because it can't tolerate natural volatility. It also cuts off the "good" portion of profits (the right tail) and increases the "bad" portion of losses. This is why stops must be placed with volatility in mind, not randomly or by "feeling". Dynamic stops (which follow the market) are better than fixed, rigid stops. A good risk/reward ratio isn't enough if the stop loss distorts your strategy. The paper "Trading With a Stop" by Nassim Nicholas Taleb clarifies, mathematically, what happens to a trading strategy when a stop loss is introduced. What many traders find intuitive ("the stop protects against risk") actually becomes much more complex once an "absorbing barrier" is inserted into a stochastic dynamic.

THE STOP LOSS AS AN ABSORBING BARRIER

Taleb analyzes a strategy with the key phrase:

"We analyze a trading strategy containing a stop loss at level H".

Mathematically, this means one thing: the stop loss is treated as an "absorbing barrier." If the price touches it, the trade ends, and the payoff is fixed at the stop loss.

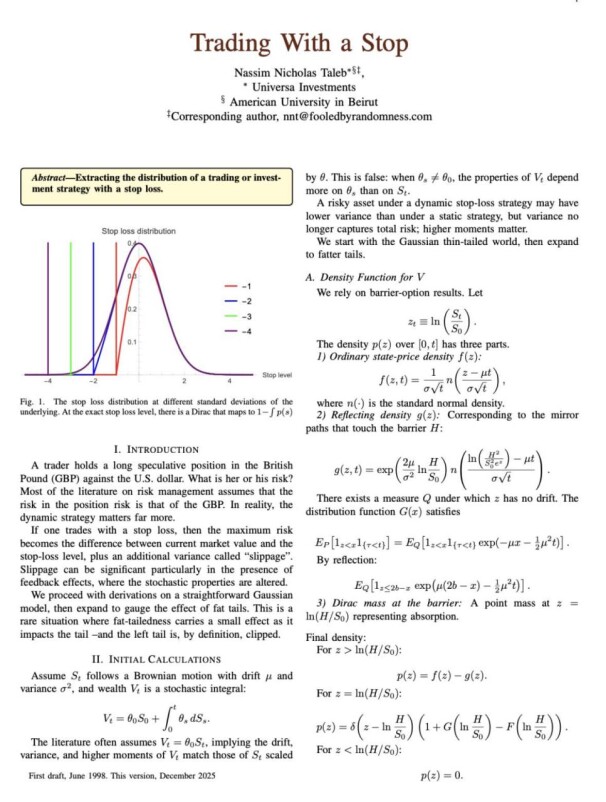

The final distribution of results is no longer Gaussian and symmetrical. Instead, it becomes the combination of: a portion derived from the asset's normal distribution, not touching the barrier, and a mass point (Dirac delta) at the stop loss position (which represents all trades touching the stop loss).

Taleb writes:

"A Dirac mass at the barrier".

This indicates the probability associated with scenarios that reach the barrier. The result is a distribution:

- More flattened on the left.

- With a "clipped" right tail.

- More leptokurtic (higher probability of extreme values).

- More fragile.

EFFECTS OF THE STOP ON MAXIMUM LOSS AND REAL RISK

Taleb defines the theoretical maximum loss:

"The maximum risk = V₀ – H + slippage".

So the stop nominally limits the loss but introduces structural slippage (not optional). The important thing is that the risk is no longer symmetric nor measurable through simple variance.

Then he adds: "The variance may decrease, but the total risk increases because the distribution is distorted. The higher moments (skew, kurtosis) become dominant".

THE BARRIER ALTERS THE DISTRIBUTION

The simulation of a Brownian process (Gaussian type) with an absorbing barrier sees the paths touching the stop fixed to the value of the barrier. This is the distribution obtained:

- A very thin and very high peak (the numerically approximated Dirac mass).

- A distorted remaining distribution.

- A shorter right tail than in the case without a stop.

- A left tail that concentrates more mass.

ANTIFRAGILE AND DYNAMIC HEDGING

Mathematical analysis connects naturally (almost didacticly) to Taleb's ideas in his books.

From Antifragile: "Artificial barriers make systems fragile".

A tight stop is, by definition, an artificial barrier. Anything that cannot tolerate volatility breaks and becomes fragile.

From Dynamic Hedging: Taleb shows how a barrier introduces path-dependence, radically alters the behavior of the process, and ensures that the dynamics are no longer governed by the same signals.

Hence the interpretation: the stop turns part of the "signal" into "noise". The stop breaks the stationarity of the process, and interpreting the market becomes more difficult.

Again from Antifragile: "Volatility should be embraced." The market "breathes." A stop too tight interrupts this breathing, disrupting the natural dynamics of the price. Stops that are too tight become fragile in the presence of non-stationary volatility, volatility clustering or jumps.

SHOULD A TRADER DO QUEUE?

- Stops should be based on volatility, not arbitrary levels.

- A stop should not be a fixed number or an emotional value.

- Stops should take into account market structure: ATR (or other proxies of σ), primary trend, volume nodes (POC, VAH, VAL), and market-specific intraday volatility.

- Overly tight stops are fragile in most cases, not only because they "exit before the impulse" but also because they introduce concavity to the payoff, increase the probability mass in the left tail, and artificially reduce the right tail (where large profits are generated).

- Dynamic stops (based on volatility) are more robust because they absorb noise, do not collapse on normal fluctuations, and keep the right tail of the distribution alive.

- A good R/R ratio is not enough. Taleb shows that with an absorbent barrier, a high theoretical R/R does not compensate for the distortion introduced by path dependence. This is a common mistake of "static" trading approaches.

FINAL NOTES

- The stop creates a concave payoff (which, according to Taleb, is the definition of fragility).

- Variance can even decrease. This is dangerous because a trader believes the strategy is "less risky" because it fluctuates less, but in reality: it is more fragile to shocks, has more mass in the left tail, and a concave payoff can break in a single event.

TRADE CONCLUSIONS

Determine the direction on high timeframes, then place stops: as deep as necessary, based on real volatility (not arbitrary percentages), aligned with the volume structure and the trend, and capable of surviving market rebounds.

Are you interested in ways to earn crypto bonus? Check it out here: Some Sites To Earn Crypto Bonus (Old & New)