In this article I will write about some great investors and traders with useful lessons for the world of investing thanks to successful strategies and traders' mindset. There are also some sentences that will surprise you.

BURTON MALKIEL

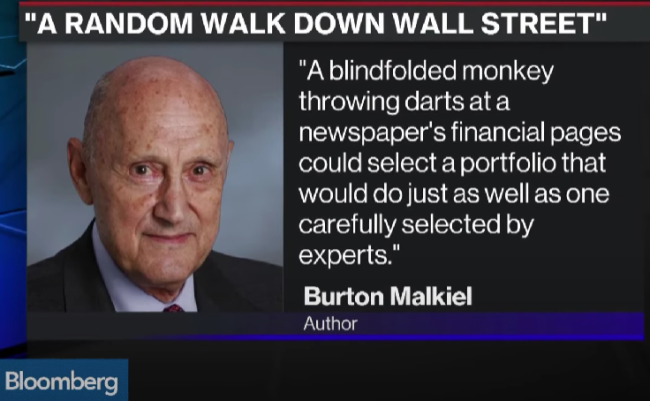

Burton Malkiel’s quote about “blindfolded monkeys” (“a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts” in his book “A Random Walk Down Wall Street”) is a way of illustrating a fundamental concept in the world of investing and finance:

1) It is often dominated by randomness: the idea is that if you could throw darts at a bulletin board with stocks, a blindfolded monkey could select stocks at random and, in some cases, perform as well as or even better than an expert investor. This serves to suggest that the stock market is unpredictable and that even experts can struggle to consistently achieve above-average returns.

2) Efficient market: Malkiel supports this theory which states that stock prices reflect all available information. As a result, it is not easy for an investor to beat the market unless you have access to superior information or truly exceptional analytical skills. What you see is already priced in, the next move is unpredictable.

3) Investing for the long term: He suggests that rather than trying to “beat the market” through active stock selection, investors should consider passive investment strategies, such as index funds, which tend to produce more stable returns over the long term.

EUGENE FAMA AND KENNETH FRENCH

Fama and French explore the distinction between luck and skill in investor success. Their research suggests that a significant portion of the market’s superior returns is attributable to chance rather than investment skill. They argue that active investors often fail to beat the market’s returns, suggesting that many of the positive outcomes may be the result of chance.

NCK MAGGIULLI

Nick Maggiulli in "Why You Shouldn't Pick Individual Stocks" argues that investing in individual stocks is risky and often ineffective compared to more diversified investment strategies. Analyzing historical data, he highlights that most investors fail to beat the market and that individual stock picking can lead to underperformance. He recommends opting for passive investments, such as index funds, to achieve more stable returns and reduce overall risk.

DANIEL KAHNEMAN

Daniel Kahneman, in “Thinking, Fast And Slow,” explores the two systems of thought that influence human decisions: fast, intuitive thinking (System 1) and slow, analytical thinking (System 2). Kahneman discusses how fast thinking can lead to cognitive errors and biases, while slow thinking requires more effort and can improve the quality of decisions.

JEAN MARIE EVEILLARD

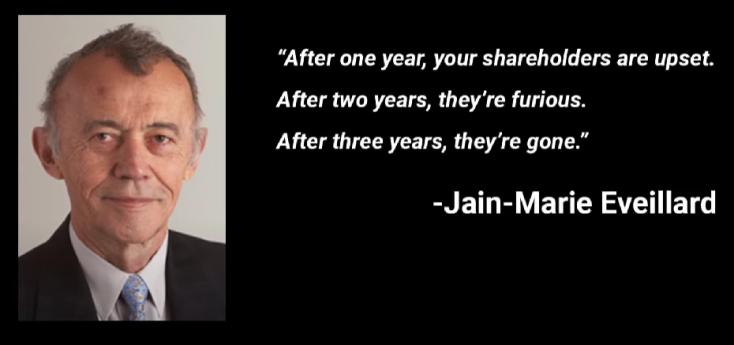

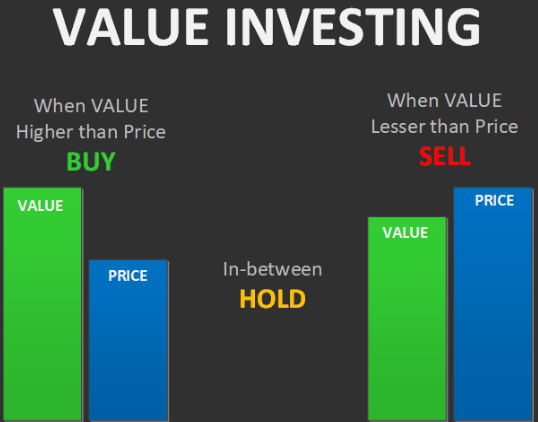

Eveillard is known for his conservative approach based on "value investing", an investment philosophy that aims to find stocks that are undervalued compared to their true intrinsic value. During the dotcom bubble in the 1990s, Eveillard chose not to participate in the general market euphoria for a few key reasons:

1) Inflated Valuations: Eveillard noticed that many technology companies, especially internet-related startups, were trading at sky-high valuations, often without any basis in profits or business models. As a value-oriented investor, Eveillard believed that these prices did not reflect the true value of companies.

2) Rationality and Discipline: Eveillard was adept at following the principles of investors such as Benjamin Graham and Warren Buffett, who advised avoiding following the crowd when markets become too speculative. Rather than getting caught up in the hype, Eveillard maintained strict discipline, believing that investing in companies without solid fundamentals was too risky.

3) Capital Protection: His primary goal was to preserve investors' capital, preferring to avoid investments that he believed could result in significant losses in the event of a market crash. For him, protecting his wealth was more important than chasing potentially high but extremely risky returns.

Eveillard did not invest in dotcoms during the bubble because the prices of many companies were disconnected from economic reality, and the risk of a correction (which then occurred) was, for him, too high.

When the dotcom bubble burst in 2000, many technology stocks lost much of their value and investors suffered huge losses. Eveillard's prudence allowed him to avoid the rout, due to the collapse of technology stocks.

MICHAEL BURRY

Burry is famous for having anticipated the 2008 financial crisis and for his investment strategies based on the in-depth analysis of fundamentals and market anomalies.

1) Fundamental Analysis and Focus on Systemic Risks: Burry studied corporate fundamentals and systemic risks. For example, in 2005-2006, he studied the subprime mortgage market in the United States and detected a huge bubble, noting that many mortgages were high risk. This led him to invest in Credit Default Swaps (CDS), a bet against subprime mortgages, which proved extraordinarily profitable when the crisis erupted.

2) Contrarian Investing: he used to invest against market trends even in an irrationally way. For example, he has taken contrarian positions on stocks like GameStop and, more recently, against the stock and bond markets, suggesting that there are signs of risk similar to those in 2008.

3) Deep Value Investing: Influenced by Benjamin Graham, Burry looks for undervalued stocks that have a margin of safety. He focuses on companies that have good intrinsic value, which the market has little recognition of (this has led him to pick overlooked stocks, especially during times of high volatility)

BILL MILLER

Bill Miller is known for his "contrarian" investing style and for running the Legg Mason Value Trust fund. His fund beat the S&P 500 index for 15 consecutive years, from 1991 to 2005, a very rare performance. Here are the main strategies that made Miller a successful investor:

1) Contrarian Investing: Miller actively sought out undervalued stocks, betting on companies that the market tended to ignore or consider risky. During times of crisis, such as the market crash of 2008, instead of running away, Miller bought stocks that he considered "underpriced", often against the prevailing trend (short and fear). This strategy is based on the idea that markets sometimes overreact and that, with the right long-term vision, such stocks can rebound and provide high returns.

2) Long-Term View: He bought Amazon and Google at a time when they were not yet perceived as "safe", especially Amazon, which at the time was still considered a very risky company. Miller believed that these companies would be successful in the long term thanks to innovative and robust business models. This long-term view allowed him to achieve high returns when these stocks became global successes.

3) Growth Investing: Miller often moved away from "value investing" to also incorporate elements of "growth investing". He did not limit himself to investing in traditionally undervalued companies but also looked at future potential, as in the case of tech companies, thus mixing aspects of value and growth. His active strategy allowed him to quickly adapt to market changes.

Miller was willing to take large positions in specific stocks, demonstrating strong conviction. For example, during the 2008 crash, instead of divesting, he increased his exposure to stocks that he believed had good intrinsic value, waiting for a future market recovery.

4) Cost Average: During periods of strong decline, Miller continued to buy, thus lowering the average carrying price of his investments (cost average) and positioning himself to maximize returns in the event of a recovery. His confidence led him to have huge positions that paid off dramatically when the markets recovered.

These strategies revolved around active management, long-term thinking, and the ability to identify contrarian opportunities.

CATHIE WOOD: INNOVATIVE SECTORS AND HIGH VOLATILITY

Cathie Wood is known for her investments oriented towards growth and innovation (artificial intelligence, biotechnology, blockchain and electric vehicles). Her vision depends on the fact that these technologies could impact the global economy and, as a result, she focuses her funds on companies such as Tesla, Roku and CRISPR Therapeutics. Wood promotes a long-term view, thinking of her investments as part of a 10-year or even longer horizon. Her strategy consists of not being influenced by strong market swings, using declines to buy more shares of the stocks she believes in. For example, during the decline of technology stocks in 2021-2022, ARK Invest continued to accumulate positions in companies such as Tesla and Zoom.

1) Highly volatile stock allocation: Wood is willing to accept high risk, allocating a significant portion of her funds to young or unprofitable companies, believing that their returns will explode as their technologies take hold.

2) Themes: ARK Invest organizes its funds by themes, not by traditional sectors. For example, the ARK Innovation ETF (ARKK) is designed to invest in innovations that are cross-cutting (i.e. the portfolio is divided by sector/theme).

WARREN BUFFETT: LONG TERM VALUE INVESTING

Buffett is one of the most famous proponents of value investing and the long-term approach, inspired by Benjamin Graham. He looks for companies with sustainable competitive advantages, known as "moats," and buys them at prices he believes are undervalued. He prefers companies with strong management, stable business models, and that generate cash flow. His philosophy is to buy and hold the shares of great companies for many years, often decades. His principles are: patience, discipline and understanding the intrinsic value of a company.

PETER LYNCH: GROWTH AT A REASONABLE (GARP)

Lynch, famous for his management of the Fidelity Magellan fund, used a strategy called GARP (Growth at a Reasonable Price). This strategy seeks growth stocks that are reasonably valued. Lynch led the Magellan fund to extraordinary returns in the 1980s, demonstrating the effectiveness of an active approach and a deep knowledge of individual companies. Lynch's strategy encourages looking for stocks of growth companies, but at a price that allows for a margin of safety.

CARL ICAHN AND THE ACTIVE ROLE IN THE COMPANIES IN WHICH HE INVESTS

Icahn is known for buying significant stakes in companies to gain influence over the boards and push them to make changes (selling assets, reducing costs, changing management) that increase shareholder value. Icahn has had success with several companies, including Apple and Netflix, but this approach can be risky, as not all companies respond positively to activism.

JOHN PAULSON: SHORT SELLING AND COUNTER-TREND BETS

Paulson is famous for betting against subprime mortgages before the 2008 crisis. Using derivatives such as credit default swaps, he made billions by predicting the collapse of the US housing market.

DAVID EINHORN: MIXED SHORT SELLING AND VALUE INVESTING

Einhorn, founder of Greenlight Capital, uses a combination of value investing and short selling on companies he considers overvalued or in financial trouble. He has had success with some short bets, such as against Lehman Brothers in 2008. Einhorn has had his ups and downs, getting off to a stellar start in the 2000s, but has suffered significant losses since 2015, in part because of his failed bet against Tesla.

GEORGE SOROS AND GLOBAL MACRO TRADING

Soros is known for Global Macro Trading, a strategy that exploits large macroeconomic changes such as fluctuations in currencies, interest rates and raw materials. Soros became famous for his bet against the British pound in 1992, a trade that earned him over $1 billion in a single day. Quantum Fund is one of the largest companies in the world, however, its high-risk investment style is not for everyone.

The great difficulty of this strategy is the understanding of macroeconomic movements and the ability to act quickly but precisely requires a high tolerance for risk.

JIM SIMONS: QUANTITATIVE TRADING AND MATHEMATICAL MODELS

Founder of Renaissance Technologies and the Medallion fund, Simons uses quantitative trading, a strategy based on complex mathematical models to identify patterns and predict market movements. His company is known for using algorithms and big data, combining science and mathematics to create automated trading strategies. This fund has achieved incredible returns, with annual performances exceeding 60%. However, this strategy requires access to data, advanced technology, and unparalleled skills in mathematics and statistics. Some strategies are still secret.

Are you interested in ways to earn crypto bonus? Check it out here: Some Sites To Earn Crypto Bonus (Old & New)