The NFT loan is a new trend that is becoming increasingly popular. It can be beneficial for both lenders and borrowers. Owners can lend illiquid NFTs to earn interest (or other NFT), while borrowers can take advantage of the NFT without actually owning it, by locking up crypto or another NFT as collateral. NFT is used as collateral, similar to the banking concept of lending or lending in DeFi.

NFT holders use their non-fungible digital assets as collateral to obtain a crypto loan which is then repaid with interest over a specified period.

The value of the loaned NFT is monitored throughout the life of the loan. Since the lender is entitled to a share of the appreciation or a percentage of any future sales of the NFT, lending it is a form of investment, except that the lender does not need to own the asset in which it invests.

In general, cryptocurrencies are highly liquid, i.e. they are easy to buy and sell, even in large quantities, quickly and at the current market price.

NFTs tend to be less liquid instead. NFT lending can provide a faster way for NFT owners to access liquidity through this system, instead of waiting for a buyer to express interest in their NFT.

The NFT loan gives owners immediate access to capital that could be used to buy a limited edition NFT or to do other things with it. By repaying the loan by a certain date, the collateral, or NFT, reverts to the rightful owner. NFT lending offers people a way to invest in NFT without buying them outright, thus limiting their financial risks to the loan period. NFT lending platforms typically feature smart contracts that facilitate the release of the NFT to the owner at the end of the loan term or the automatic transfer of ownership rights if a borrower defaults on a loan. Obviously if the NFT in question decreases in value, the borrower of the NFT could be stuck with an asset that is worth less than when the original loan agreement was entered into.

In the event that the loan holder does not repay it when due, the NFT lending platform may initiate a liquidation procedure. This procedure could include the sale of the NFT deposited on the market, in order to cover the value of the loan and the cost of liquidation itself. Ultimately, NFT lending models provide NFT borrowers with an alternative avenue to earn interest while enabling them to diversify their investment portfolios and sources of income. Other strategies involve borrowing an NFT, collateralizing it to borrow another NFT, and then borrowing crypto.

Among the best known platforms we find Zharta or Niftyx Protocol. Another similar dapp is Aavegotchi which allows you to borrow Gotchi, unique virtual creatures, and use them as collateral to borrow other crypto assets. There are also fractional NFT, owned in co-ownership (NFT is divided into shards which are basically erc20 tokens that can be sold to speculate).

LENDER

The lender lends cryptocurrency or NFT in exchange for the NFT deposited as collateral by the borrower. The lender basically can choose to lend cryptocurrency or NFTs on similar platforms in order to get interest on the loan. In general, the NFT lending platform sets the interest rates for the loans and the lender receives a portion of this interest based on the amount lent. The lender has the right to receive repayment of the loan when it matures, together with any agreed interest and fees. In the event that the borrower fails to repay the loan when due, the NFT lending platform can initiate a liquidation procedure of the NFT deposited by the borrower as collateral, in order to cover the value of the loan and the liquidation cost.

In general, the lender takes on a lower level of risk than the borrower, as he receives the NFT as collateral for the loan.

BORROWER

A borrower is someone who borrows NFTs or cryptocurrency in exchange for depositing an NFT as collateral. He deposits his NFT on the platform and receives the requested loan in return. During the loan period, the borrower has access to the loaned cryptocurrency or NFT and can use it as they see fit.

The borrower must repay the loan when due, along with any agreed interest and fees. Otherwise, the borrower risks losing the NFT deposited as collateral, as the platform may initiate an NFT liquidation process.

To avoid NFT liquidation, the borrower can choose to repay the loan before maturity or add more cryptocurrency or NFT as collateral to maintain the coverage percentage of the NFT deposited.

There are several NFT loan models:

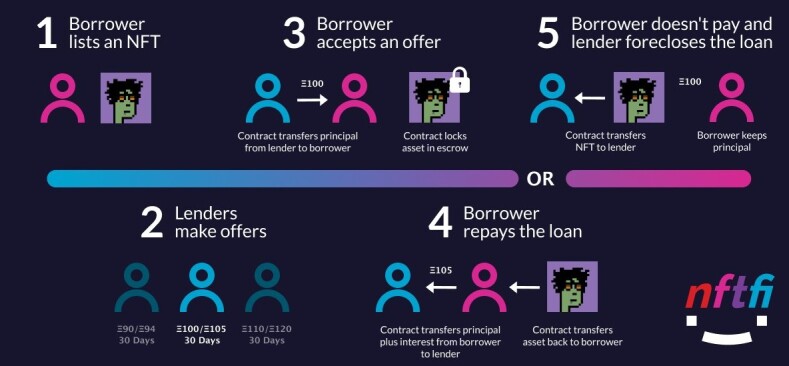

1) P2P peer-to-peer NFT lending (an owner lists their NFT on the platform and receives loan offers from interested parties. Once the match is made, the NFT is placed in an escrow vault until the loan defaults or expires. If the NFT owner does not pay back the loan, the NFT is transferred to the crypto lender's wallet, via a smart contract)

2) Peer-to-protocol NFT lending (here users can collateralize their NFT and borrow directly from the protocol. In return, they will receive funds from liquidity providers who add crypto to a pool. In a peer-to-protocol NFT lending model to-protocol, the liquidity providers are technically the borrowers of the secured NFT and earn interest as such.There is no maturity here, what is controlled is the health factor of the NFT loan, i.e. the difference between the value market value and the outstanding loan amount. As soon as the price falls below a threshold, the asset is typically transferred to the protocol, as a sort of liquidation. Depending on the platform, the owner of the NFT can be granted a period to repay the loan and request repayment of the same)

3) NFT Rentals (the primary focus for renters is not the interest but the benefits associated with the NFT, whether it be community or club membership or the right to receive merchandise. Since the primary utility extracted from such NFT is non-monetary, NFT rental agreements usually come with no repayment, interest or liquidation terms.The asset is returned to the owner of the NFT at the end of the term.In the meantime, the lessee enjoys access to the associated benefits to the particular NFT

4) Non-fungible debt positions (Here a unique digital asset representing a loan agreement is created, known as a non-fungible debt position also called NFDP. The NFDP is stored on a blockchain and serves as a record of the loan agreement, ensuring that the terms are not altered.Furthermore, the NFDP can be traded on a secondary market

For Lending Website: List Of 30 NFT Lending Dapps On Ethereum

Are you interested in ways to earn crypto bonus? Check it out here: Some Sites To Earn Crypto Bonus (Old & New)