In today's weekly market updates, we are going to look at what has happened in the fixed income, money market, commodities and U.S. equity markets last week (i.e. the week ending 1 July 2022), and discuss what these would carry for the crypto market.

Investment Disclaimer:

- I am not a registered investment, legal, or tax adviser or a broker/dealer, and all opinions expressed by me are from my research for educational purposes only.

- Past performance presented here is not an indicator of future performance.

- This post expresses my own opinion about the financial market. It is not an offer to buy or sell, or a solicitation of any offer to buy or sell any security mentioned in this post.

Fixed Income and Money Market

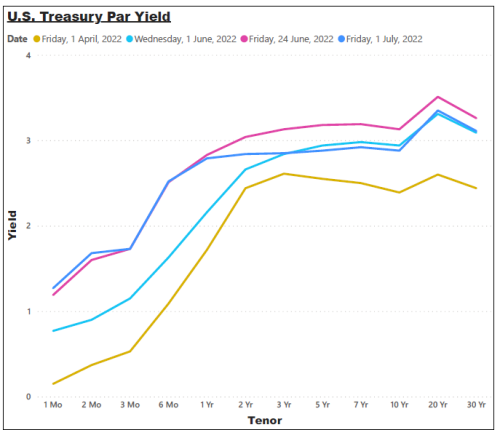

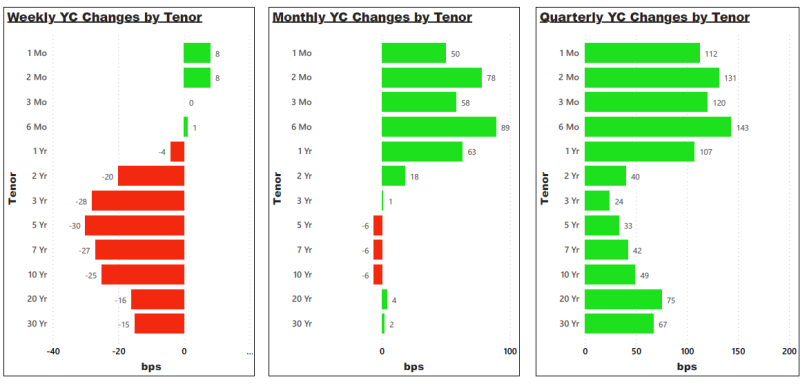

U.S. Treasury par yield curve was flattened last week as Fed's proposed 75 bps rate hike has sparked a recessionary fear. The curve's short-term tenors (1-month and 2-month tenors) are rising 8 bps while its intermediate-terms (3-year, 5-year and 7-year tenors) drop 27 bps to 30 bps.

(1 basis point, bp = 0.01%)

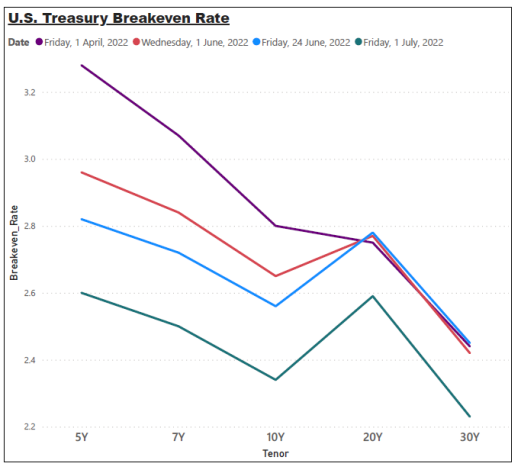

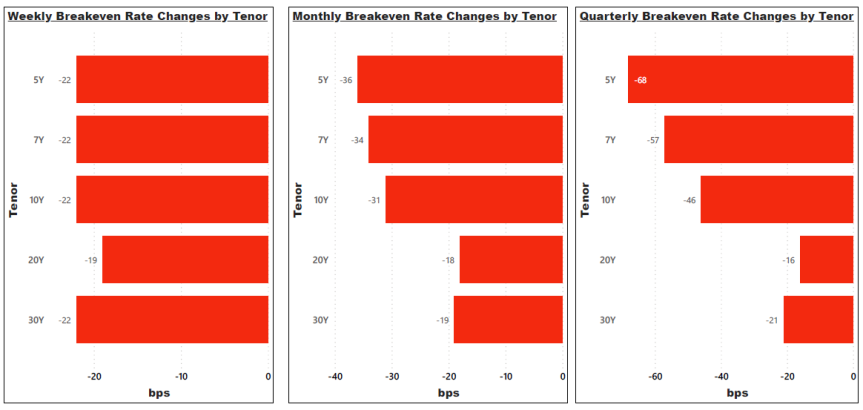

U.S. Treasury breakeven rate (a quantitative parameter that estimates the expected inflation priced in by the market participants) fell sharply across all tenors by double-digit bps over the week on an easing inflation outlook as the economy is expected to deteriorate.

According to a Bloomberg report, as the financial market outlook turns gloomy, more than 70 bond deals have been postponed or canceled so far. Furthermore, initial public offerings (IPO) and M&A deals are also increasingly being put on hold.

2 main components that would impact bond market performances are interest rate decisions by the Federal Reserve (Fed) and the credit profile of the bond issuer.

A hawkish environment (an economic period where there are aggressive rate hikes, e.g. the year 2018) would exert downward pressure on corporate bond prices as borrowing costs are getting more expensive, and investors would prefer to park their money in the safe-haven government securities which now offer a higher yield. On the other hand, if rate hikes are the result of inflationary pressure due to an improving economy, the credit profiles of many bonds issuers are becoming better, hence, this would be positive for the corporate bond prices.

On the other hand, a dovish environment (an economic period where there are aggressive rate cuts, e.g. the year 2020 when there is a Covid-19 outbreak) would exert upward pressure on corporate bond prices as borrowing costs are getting cheaper, and investors would prefer not to park their money in the safe-haven government securities which now offer a very low yield due to rate cuts and would not mind taking some risks on corporate bonds in exchange of higher yield. On the other hand, if rate cuts are the result of an economic recession, the credit profiles of many bond issuers worsen, hence, this would be negative for the corporate bond prices.

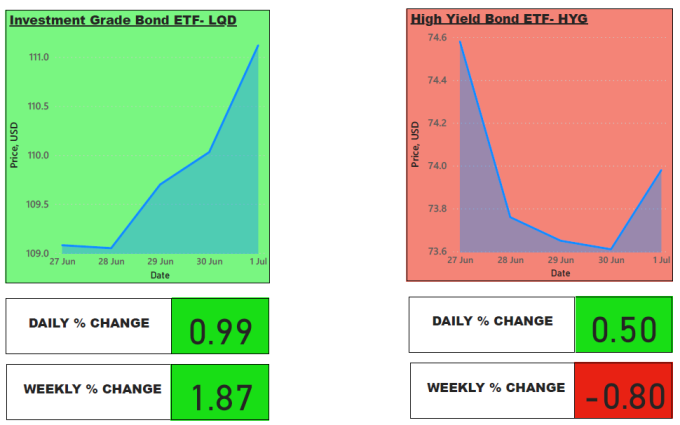

The high-yield bond ETF (NYSEARCA: HYG) is exposed to more cyclical sectors and has more exposure to bonds that are rated BBB and below than the investment-grade bond ETF (NYSEARCA: LQD), therefore, subjected to a higher probability of default and hence more sensitive to the credit component. Investment-grade ETF is exposed to more stable sectors and has more exposure to highly rated bonds (rating BBB and above), hence less sensitive to the credit component but more sensitive to Fed's rate hike decision. When the economy is booming, high-yield bonds would usually outperform investment-grade bonds and the opposite would happen during a recession.

Defensive strategies are back into play now, with rising inflation, a flattening yield curve and a gloomy economic outlook. Flight-to-safety behavior has been observed in last week's bond market as investors are selling off risky high-yield bonds to buy defensive investment-grade bonds. As a result, the investment-grade bond ETF rose by 1.87% over the last week while the high-yield bond ETF dropped by 0.80%.

Commodities

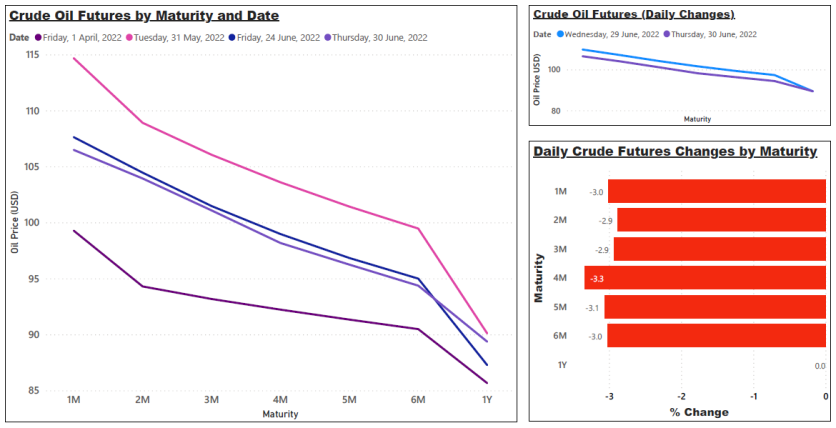

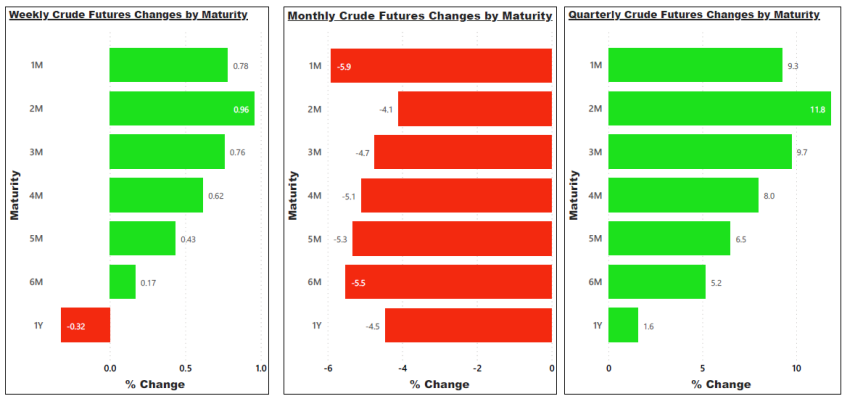

Crude oil futures with 1-month to 6-month maturities rose slightly as concerns for tightening oil productions outweigh the recessionary fear. Intensification of Russia-Ukraine conflicts, Libya political unrest and Norwegian offshore oil and gas workers' strike are causing fears in the oil market, contributing to the rise in crude oil futures.

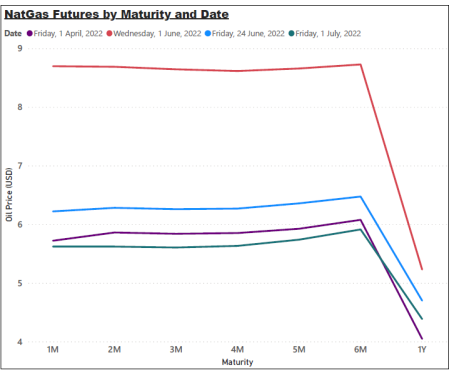

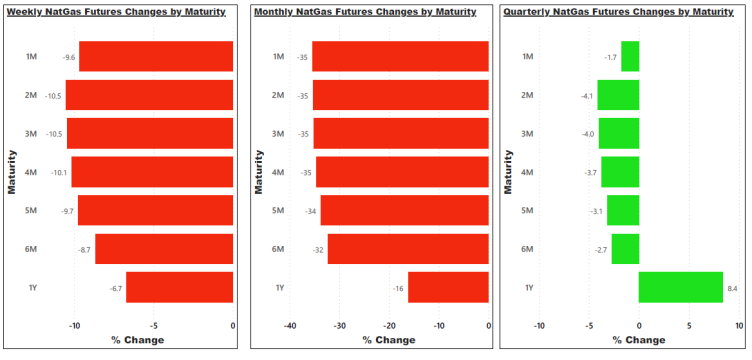

Natural gas futures on the other hand were traded in the opposite direction to crude oil futures, with futures prices across near-term maturities falling by 9.6% to 10.5%. The sharp fall in natural gas futures was contributed by the shutdown of the U.S. second-largest LNG export plant, Freeport over safety concerns in Texas.

Freeport was expected to leave around 180 billion cubic feet (bcf) of gas available to the U.S. market. This plant was consuming about 2 billion cubic feet per day (bcfd) of gas before it shut on June 8. Natural gas futures fell due to expected excessive supplies from this incident.

Equities

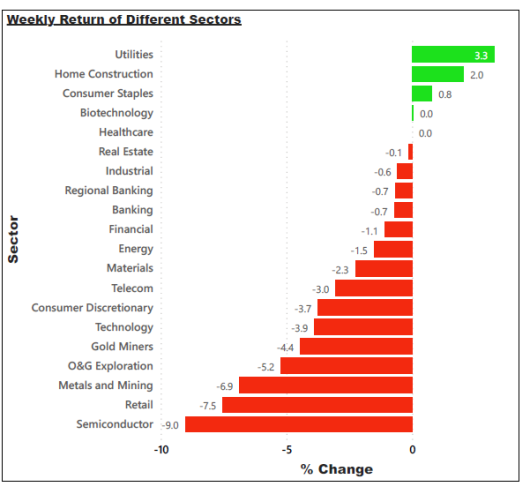

The semiconductor sector fell on the warning given by Micron Technology's (NASDAQ: MU) CEO, Sanjay Mehrotra which indicates a slowing consumer demand. During the earning calls with analysts, he expected smartphone sales to fall significantly behind the previous 2022 projection figures. As Micron Technology is the major vendor of memory chips for PCs and smartphones, this has sparked fears in the equity market.

Semiconductor sales are often used as a barometer to gauge consumer sentiment and economic performances as semiconductors are widely used across different sectors such as electrical appliances, smartphones, personal computers, data centers and artificial intelligence. A significant slowdown in semiconductor sales could be a leading indicator of weakening consumer demands and an impending recession.

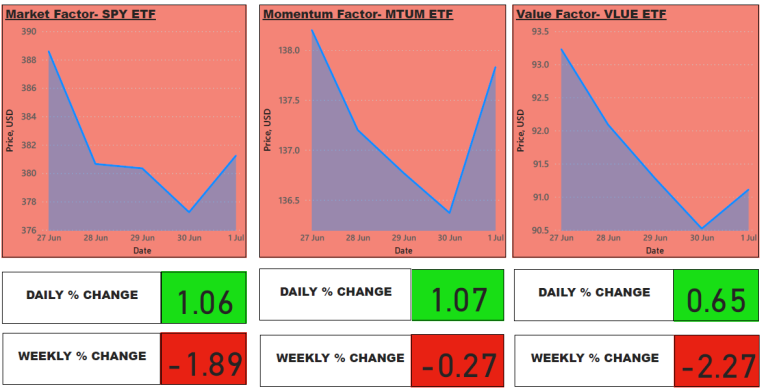

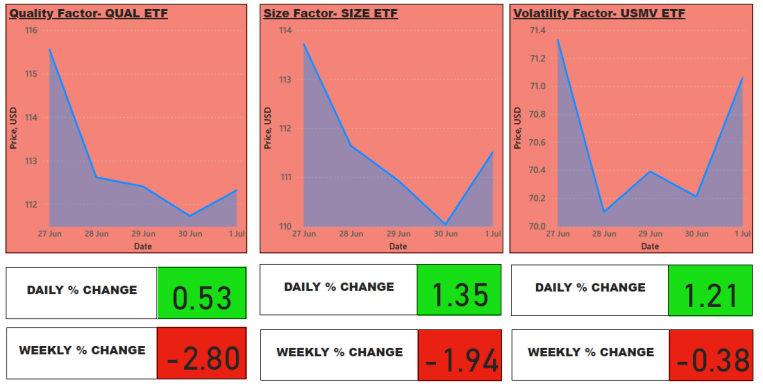

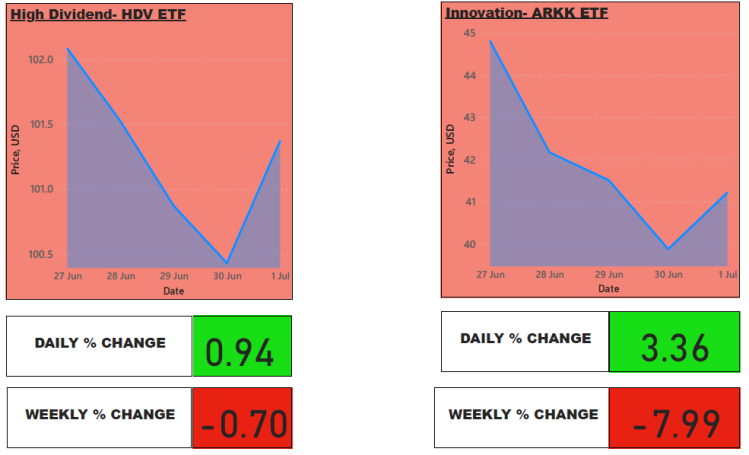

A flight-to-quality scenario was shown in the equity market too where stock investors are rotating from cyclical and volatile sectors which are sensitive to the surrounding economy such as oil and gas, mining, technology and consumer discretionary into stable sectors like utilities and consumer staples which are impacted less by the economic slowdown.

Crypto

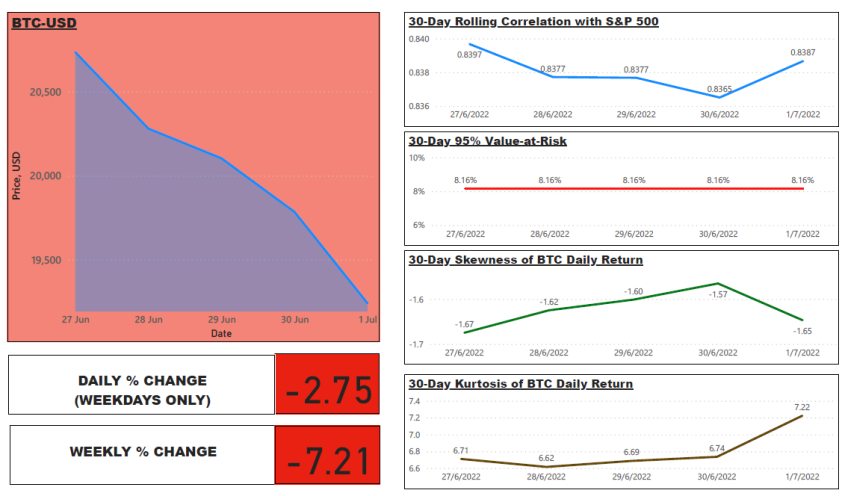

Bitcoin has had a bad week too as it suffered a further 7.21% drop over the last week. Its correlation with S&P 500 index has once again spiked to the previous week's level and its downside risk is getting more dominant with greater negative skewness (i.e. a higher probability of generating losses as compared to gains) and a larger kurtosis value (i.e. a higher probability of large drawdown).

That's it! That's the weekly market updates from me today.

Connect with me at:

If you like my analysis and articles, you could follow me at @quantdoge for daily market updates like this.

1. Thumbnail image here was downloaded from Unsplash, where credit is given to Mark Basarab the creator of this photo.

2. https://www.cnbc.com/2022/07/01/us-bonds-10-year-treasury-yield-in-focus-on-recession-fears.html

3. https://www.bloomberg.com/news/articles/2022-07-01/companies-are-scrapping-bond-sales-at-the-fastest-pace-in-years

4. https://www.reuters.com/business/energy/oil-prices-rise-after-falling-3-previous-session-2022-07-01/

9. https://www.businesstimes.com.sg/energy-commodities/oil-rises-as-tight-supply-trumps-recession-fears