Official inflation rate in the United States has hovered around 2% over the last few years. For depositors in the U.S, there aren’t many opportunities to earn interest above the official inflation rate. The most competitive rate with legacy banks is currently 2.38% and is likely to decline to zero due to the Fed.

Non-traditional financial platforms like BlockFi may be the salvation against inflation. The platform is currently offering a whopping 8.6% APY (Annual Percentage Yield) on GUSD deposits. The Gemini Dollar (GUSD) is essentially a digital dollar issued on the Ethereum blockchain. It is fully regulated and is regularly audited to ensure 1:1 parity with the US dollar (USD). Moreover, the monthly interest payments are compounded.

Another Bitconnect?

For those who witnessed and participated in the 2017 mania, this tends to be initial response. However, in comparison Bitconnect offered a daily compounded rate of 1% and provided no transparency on their business model. The infamous Bitconnect scam exited in early 2018 and cleaned out many misled investors. Needless to say this incidence left a scar on the industry and many investors are now skeptical of lending platforms.

Unlike Bitconnect, BlockFi’s lending model is clearly stated on their website. Furthermore, the CEO of BlockFi is well known and regularly appears on interviews. In fact, Anthony Pompliano, an investor, regularly plugs the platform on his popular podcast (Off The Chain). This is a sharp contrast from Bitconnect. The creators of Bitconnect never appeared publicly or participated in interviews. In my view, it is clear that BlockFi is not a scam. However, it is not unreasonable to question their sustainability.

Lending Model

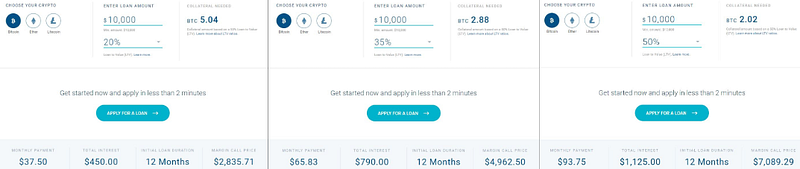

In short, BlockFi enables investors to use their cryptocurrencies as collateral towards a cryptocurrency-backed loan. The interest rate on the loans range from 4.5% to 13.25% and may include an origin fee. To sustain interest payments to depositors and investors, the platform’s average rate of return must remain above 8.6% for GUSD. Given that the platform is yielding 8.6% it is likely that most borrowers are selecting loans with a high LTV (Loan To Value) ratio.

As you see above, higher LTV ratio loans require less bitcoin to be locked up as collateral. And as a result the interest rate is higher. The highest interest rate according to the illustration above is approximately 9.375% for a loan of 10K USD. BlockFi can easily pay depositors 8.6% and sell bitcoin to make them whole in the event of a default. Ultimately, free market variables will determine the rates and adjustments may be necessary in the future. Supply of USD, demand for collateral-based loans, and competition will drive rates moving forward. For example, BlockFi adjusted the rate for lending Ethereum in May 2019.

“ The rate for deposits of between 25 ETH and 100 ETH will change from 6.2% to 3.25% APY “ -BlockFi

In my view, this is healthy and indicates BlockFi is focused on maintaining the platform’s long term financial viability. Other platforms such Crypto.com, Bitrue, and Celsisus have made similar efforts.

What If There Is A Default

All loans require collateral and have predetermined margin call prices. This means if the per unit price of an asset falls to a certain value, the collateral is liquidated to make the lender whole unless the borrower is able to provide more collateral. For example, in the image below the margin call price is $7336 and the collateral is 1.95 bitcoin. In the event that bitcoin price falls below $7336, the borrower must deposit more bitcoin as collateral or face liquidation. BlockFi notifies client with ample to time to preemptively take action by depositing additional collateral. If the client fails to deposit additional funds, BlockFi will sell off a part of the collateral to maintain a healthy LTV ratio.

Assuming the platform diligently adheres to their margin call policy, the depositors have zero risk from potential defaults. However, users are trusting that BlockFi is taking appropriate measures to secure investor funds and will not act against the interest of users. In modern finance, trusting a third party is unavoidable. For this reason, it is entirely up to the user to perform their due diligence in vetting a platform.

Here’s an interview from Pomp’s podcast, where Blockfi’s CEO addresses pertinent questions about the platforms lending service.

The Proliferation Of Lending Platforms

It’s not surprising to see these lending platforms are gaining traction with investors. The prospects of getting relatively high rates with minimal risk is a huge incentive. It becomes even more appealing in a world where central banks are aggressively cutting rates, geopolitical instability is creating profound market volatility, and many retirees have been deprived of reliable yields. I firmly believe finance Dapps (Decentralized Applications) in the crypto space are well positioned to disrupt traditional finance. It will take time for the space to mature and gain credibility. Once the space is sufficiently regulated, retail investors will flock to platforms like BlockFi. I personally have put my crypto assets to work across multiple platforms to mitigate my risk and maximize my yields. I recently got verified with BlockFi and moving forward I plan to publish my progress. If you are interested in following my progress please follow me on the social media channels below.