Introduction

We will analyse the BAT from many perspectives. Among the most interesting not questionable results we will show how the BAT ETH exchange rate is often far better in decentralized exchanges than centralized ones. We will work around the price equilibrium theory proposed by bat project in its whitepaper and study the possible flow of bat in an equilibrium market with implications on wallets, decentralized exchanges and liquidity pools.

What we will do is:

- Focus on the blockchain of the ICO (ethereum in this case) and list the main consequences of this.

- Define the token type: utility, payment, asset or hybrid. The first step is to clarify its nature and this is often not written anywhere therefore the investor judgement plays a role.

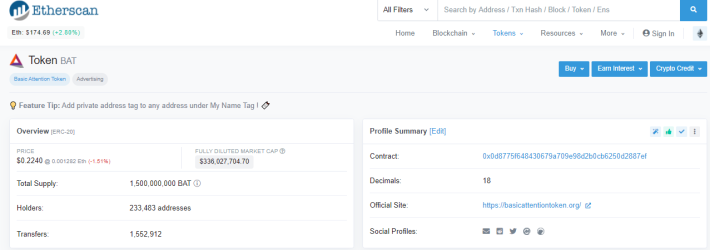

- Clarify the market cap and the monetary supply policy (capped, with inflation, with mining or minting). Use etherscan to proof all the assertions https://www.reddit.com/r/BATProject/comments/7maakq/will_the_total_supply_always_be_15_billion_tokens/?utm_source=share&utm_medium=ios_app&utm_name=iossmf

- Some meaningful observations from etherscan

- Study the white paper with an eye on the price equilibrium.

- Demonstrate the growth

- Observe that the stability could be very far to be reached: price up! Go through the implications in next points.

Here starts an original approach to focus on microfinance:

- The flow of bats (VISUAL).

- Micropayment to brave users, publish0X, content creators

- The concept of research of optimal liquidity PATH by user need.

- The need of studying liquidity pools, (S)DEX, wallets services.

Implication of running in ethereum

BAT is an ERC-20 token issued on the ethereum blockchain

The following schema is valid for each ERC-20 token:

- Ethereum is a very well known blockchain.

- The vast majority of ICOs has been performed on ethereum.

- There are qualified auditors for assessing the smart contracts which are backing the icos. Auditing is necessary because ethereum VM runs the contracts in a Turing complete language. This means that they can reach a certain degree of complexity and, being online on the ledger forever, are exposed to hackers which are looking for bugs (so called honeypots)

- The distributed ledger is easily accessible without the need of running a node. It is possible to use third party services like etherscan https://etherscan.io. This allows everybody to verify the data provided by the company behind the ICO

- The tokens issued on ethereum can be traded at cost of gas

- It is possible to trade in chain without the usage of an exchange using typically decentralized exchanges at the cost of gas plus bid ask spread. Changes among cryptos on different chains can be less frictionless but this is not a rule in case they are liquid enough; I mention here uniswap (link) as an example, ...provide others as changelly, shapeshift

Token type

From the website and technical paper we can say the following about BAT:

- it is not mined but minted in a predefined quantity

- it is an utility token which is distributed to users to reward their attention.

Being a contract on ehtereum can be audited and from this we can come to not opinable statements about market cap and monetary supply.

Market cap and monetary supply

The main data:

- Market cap: 1.5 billion tokens

- BAT team cannot create more tokens out of thin air

Market cap can be verified checking the contract:

https://etherscan.io/token/0x0d8775f648430679a709e98d2b0cb6250d2887ef

Below I show the meaningful part of it (see field total Total Supply)

This proofs that the total supply is limited.

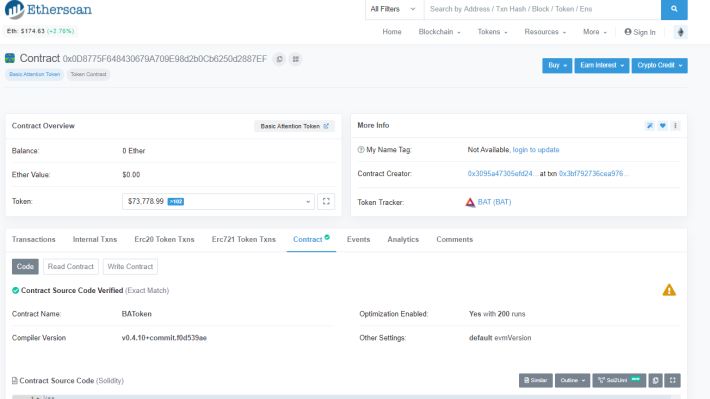

Now let’s read the contract:

https://etherscan.io/address/0x0d8775f648430679a709e98d2b0cb6250d2887ef#code

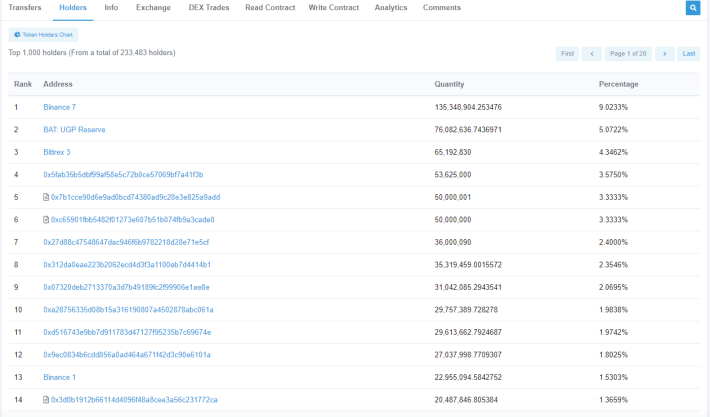

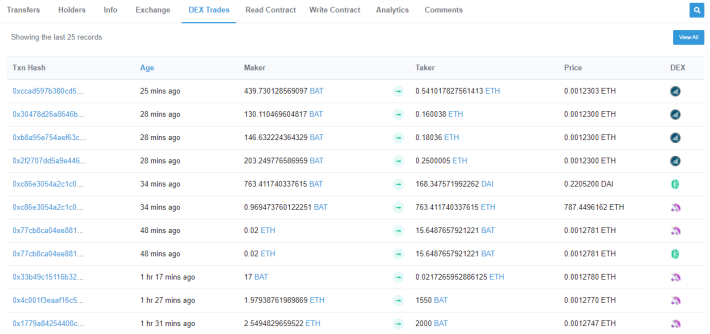

Other information from the ledger (DEX can be far cheaper than centralized exchanges!!!!)

We can see the biggest holders

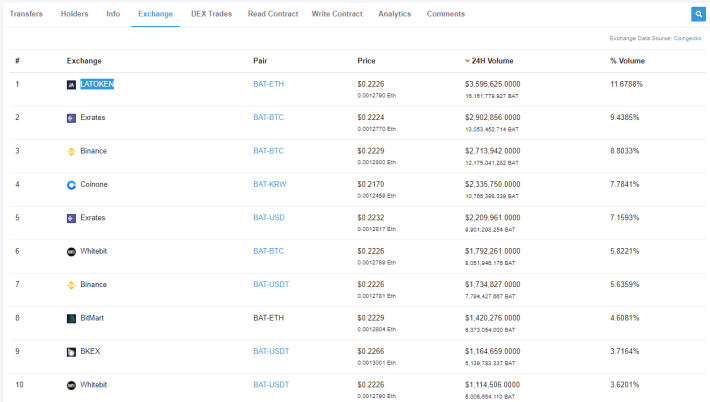

And a very interesting statistic about exchange prices in exchanges and decentralized exchanges (IMPORTANT: I took the data at the same time for the two graphics alone. Everybody can recheck periodically):

Exchanges

Decentralized exchanges

The symbol are idex, kyber and uniswap (the unicorn).

In the centralized exchanges bat/eth is 0.0012790 in the most liquid (Latoken) and more or less always around (0.00127-0.00128 or worse with one exception of Coinone).

In the DEX (so exchanges not centralized and run using the blockchain) 0.0012303 of IDEX, 0.0012780-1 of uniswap and kyber. I have not checked the bid ask spreads but it looks evident that the centralized exchanges are more expensive (boasting a 3% premium).

This proofs for the BAT-ETH that DEX can be far cheaper than centralized exchanges!!!

This has a strong implicaiton of on what could become the routes of the flow of BATs in the future.

White paper (price stability)

As with all ico or token emissions the official site includes many information ans, extremely important, a whitepaper. Nobody should ever invest in a cryptocurrency whitout ever having read the whitepaper. The steps in order are: checking if coin amount is capped, read the whitepaper, understand business model (the usual question is where is growth) . So I suggest to read the full paper here:

In this article we are interested in a specific part of the whitepaper. Don’t be too scared by formulas (I will just write down in extreme synthesis the main take)

7.3

An Analysis of the Stability of the BAT A model for virtual currency exchange rates was postulated by Dutch economists von Oordt and Bolt in 2016[27]. The model postulates that the value of virtual currencies consists of three major factors; the utility of the virtual currency to make payments, the decision of forward-looking speculators to regulate the supply of virtual currency, and the elements that drive user adoption and merchant acceptance of a virtual currency. The argument originates with Fisher’s 1911 observation that speculators may effectively limit the money supply by withdrawing money from circulation in anticipation of higher future utility. Since this dynamic particularly applies to limited issuance currencies such as bitcoin or BAT, it can be an important factor in the pricing for token sales and stability analysis of virtual currencies. For a simple economic system with fixed quantity of currency tokens MBAT, we can write down a transaction quantity relationship: P BAT t T BAT t = MBATV BAT t Where V BAT t is velocity of BAT, the average number of times each unit of BAT is used to purchase services within the defined period of time t. T BAT t is the quantity of 32 services purchased with BAT over the period of time t and P BAT t is the weighted price of the services. Inserting the exchange rate in terms of $ P BAT t P $ t T BAT t = MBATV BAT t Since we can assume the legacy fiat currency is the accounting unit for all parties involved, we define the exchange rate S $ BAT t , and substitute in the above equation to give S $ BAT t = T BAT t MBATV BAT t If we consider the fraction of currency which is not used in transfer of services, we can postulate a velocity of the fraction of currency which is actually used for settlement VdBAT t . Defining Z BAT t to be the number of BAT units not used in transactions. Since the entire velocity of money in our economy V BAT t is an average between the currency units used and the units unused for transfer of services, V BAT t = MBAT − Z BAT t MBAT VdBAT t Combining these into the exchange rate S $ BAT t = TdBAT t (MBAT − Z BAT t )VdBAT t (1) The exchange rate for BAT tokens is therefore proportional to the volume of services purchased and inversely proportional to the currency not used in transactions for the time period t. This equation encapsulates the insight that a lack of money in circulation will raise the exchange rate. We now turn our attention to the fraction of BAT which is not used for exchange. Some of the Z BAT t tokens may be the result of users forgetting about the small number of tokens they hold. Some may be due to exchange delays in settlement for legacy currencies. Overall though, the holders of inactive tokens have standard ways of evaluating future utility of the tokens in terms of modern risk management theory. Since tokens do not bear interest, there is a discounted term associated with holding a position of size z BAT t in them. −RS $ BAT z BAT t where R is the interest rate discounting in the legacy currency. If we consider the future expected value of the BAT holdings as the sum of the future expected value of the position in BAT ||S $ BAT t + 1||z BAT t 33 with this discounted interest rate term (where R is the discounting operator), and the volatility of the future position in BAT scaled by a risk aversion term γ, we reach the efficient frontier from modern portfolio theory. ||S $ BAT t+1 ||z BAT t − R(S $ BAT t )z BAT t + γσ2 (||S $ BAT t+1 ||)z BAT t = 0 Using this standard result, we can solve for the optimal number of tokens held by an individual during a given time period. z BAT t = ||S $ BAT t+1 || − R(S $ BAT t ) γσ2(||S $ BAT t+1 ||) If we consider all of the people holding BAT at a given time interval t we get the economically efficient number of BAT held for later use. Z BAT t = Ntz BAT t = ||S $ BAT t+1 ||z BAT t − R(S $ BAT t ) γ Nt σ 2(||S $ BAT t+1 ||) Since this value can’t be negative, we assume that people who hold BAT have the position that ||S $ BAT t+1 || ≥ R(S $ BAT t ) hence, using our above relationship, we get the relationship between the expected future value of the BAT, the interest rate and the velocity of transfers in the BAT economy: R −1 (||S $ BAT t+1 ||) ≥ T BAT t MBATV BAT t So, people hold BAT if the discounted expected value exceeds the hypothetical value of the current exchange rate. So, the exchange rate as a function of future expected value of BAT is S $ BAT t = R −1 (||S $ BAT t+1 || − γ Nt Z BAT t σ 2 (||S $ BAT t+1 ||)) (2) Thus, the BAT holdings are the discounted expected future exchange rate minus the risk premium for the uncertainty in future value of the BAT. If the model holds, 1 and 2 can be used to define supply and demand for BAT. Since MBAT is not time dependent in the case of BAT, the time varying exchange rate can be readily understood in terms of BAT transactions and opinions on future utility of BAT transactions. As BAT transactions increase, the exchange rate becomes dominated by the transactions rather than future expectations of utility. This dynamic has been observed in maturing virtual currencies as well as various other in-house token systems. While models are imprecise, this model argues for long term price stability in a token mediated economy.

The main take is that the BAT should reach a price stability and fluctuate around that value without the high standard deviation we are experiencing now.

The theory is a model and models are questionable: I anyway agree on the stability on long term.

Where are we now?

- We will show that we are in a high expansion phase (growth)

- We will discuss about a stability moving up for many years with some swings

- We will speak about the token price possible evolution

Demonstrate growth

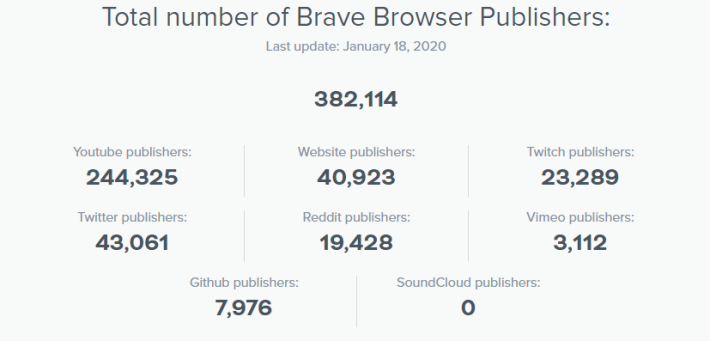

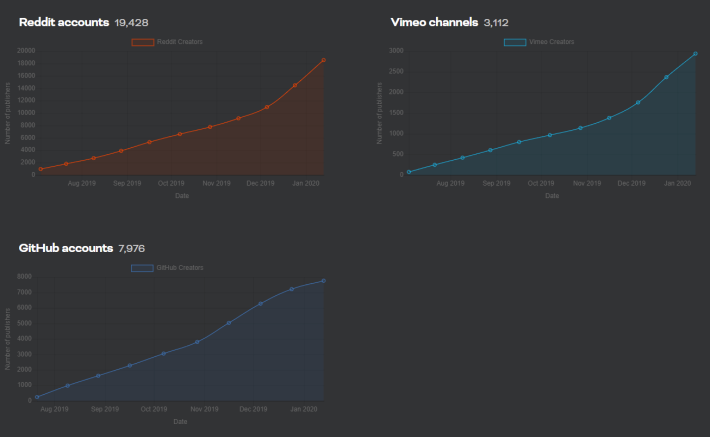

A nice work has been done by the website https://batgrowth.com/ which running robots against BAT API and in twitter, youtube and other social can keep trace with regularity of user adoption.

Thanks to https://batgrowth.com/ for the following table:

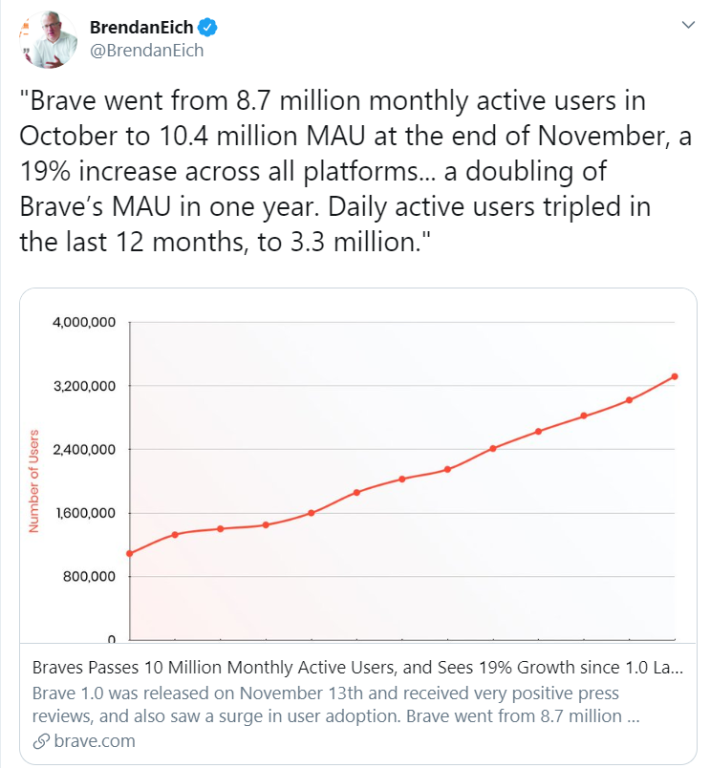

Above is reported a twitter from Brendan Eich…

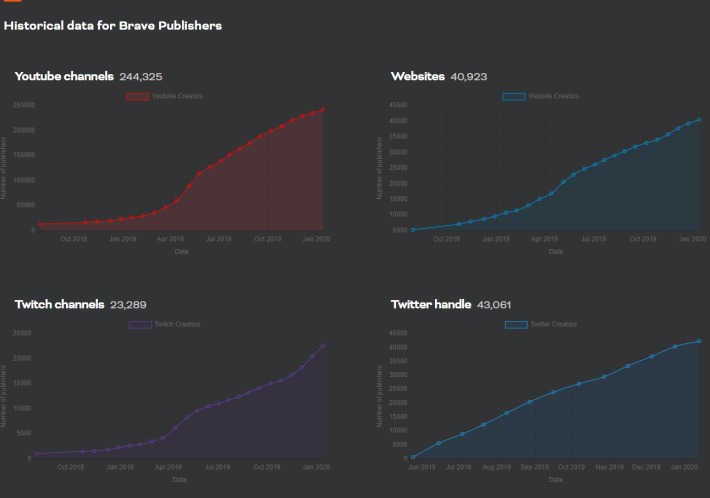

Thanks (again) to https://batgrowth.com/ for the following three tables:

All the information displayed are the proof of a string growth which is still accelerating. Now the question becomes: if BAT is modeled as a token whose valuation tend toreach stability in the long run: where is the stability? It is legit to expect that the stability will be reached after stabilization of growth. Till then, with the swings typical of cryptos there will be a growing trend in the BAT price

Investing in token

The horizon looks very positive to, at least, hold the token gained online. Actually we have seen that there are all the preconditions for a growth in value and a relative stability which will be reached when BAT will, if it is the case, become a kind of well accepted mean of payment and the growth narrative wil have slowed down.

Second part

We start now discussing the flow of the BAT (this model is particularly true for the BAT token because of its circular economy) and its implications.

The flow

The reader can skip the citation below if desires. I will summarize the part we need to develop now. I have found this beautiful reddit post so informative that I have decided to add it in all completeness into the article: https://www.reddit.com/r/BATProject/comments/7cr7yc/new_to_bat_read_this_introduction_to_basic/)

Welcome to r/BATProject, the official subreddit for Basic Attention Token (BAT)! This introductory guide is designed to help you gain a big picture understanding BAT: what it is, what it solves, and how. For more detailed information, please refer to the whitepaper. For an outline of BAT's release phases, please refer to the roadmap.

You can find fantastic beginner tutorial videos, courtesy of Coinbase, here. Also see our BAT Community YouTube channel for more video content.

Note: Please note that BAT is still in development and that some of the features mentioned herein have not yet been released. This guide will be continually updated.

What is Basic Attention Token (BAT)?

Basic Attention Token is a blockchain-based digital advertising and rewards platform from the creator of Javascript and co-founder of Mozilla & Firefox. Developers will be able to incorporate BAT functionality into their own applications with the upcoming BAT SDK.

The BAT token is an Ethereum-based ERC20 utility token, utilized as the unit of account within the overarching BAT platform:

- Advertiserswill transact in BAT tokens to purchase advertising space and user attention within the BAT Ads network. (Advertisers will use a self-serve advertiser dashboard or Brave's managed services for advertisers.) See: https://ads.brave.com

- Publishers, content creatorsand app developers will receive user contributions (e.g., tips) and ad revenue in BAT tokens. (Publishers/creators use the Creator Dashboard.)

- Userswill earn BAT tokens for opting into Brave Ads, called “ad revenue sharing”. (Users use BAT-enabled applications such as the Brave browser.)

Custodial wallet and exchange services, such as those provided by Uphold.com, allow mainstream parties to utilize the BAT platform and transact in BAT tokens without specialized knowledge of blockchain technology. For example, advertisers will be able to pay upfront with fiat currency, and an exchange for BAT tokens will occur behind the scenes.

Example Flow

- An advertiser launches an ad campaign using the BAT self-serve ad dashboard or through Brave's managed services for advertisers. (Payments in fiat will be exchanged for BAT tokens.)

- The ad campaign (its description, format, links, creatives, duration, targeted demographics, etc.) is added to the BAT network ad catalog.

- The ad catalogis downloaded into BAT-enabled applications, such as the Brave browser.

- The Brave browser uses locally-running machine learning algorithms to match ads inside the ad catalog to the user's interests and intent signals. All user data is stored locally and never leaves the device.

- Once a match is made, the application (Brave) delivers a targeted ad to the user at an opportune moment in their browsing experience.

- For seeing the ad, users are rewarded a percentage of the gross ad spend for that advertisement. Users receive 70% for User Ads ads which appear as system notifications, and will earn 15% for Publisher-Integrated Ads, which appear on or in conjunction with publisher content (such as a banner advertisement).

Brave Rewards: How does BAT work with the Brave browser?

Brave is an open-source, privacy-focused, performant web browser with millions of users that blocks third-party ads, trackers and mining scripts by default, and offers a set of powerful pro-privacy features (such as Tor-browsing). Brave is available on Android, iOS, Windows, macOS and Linux.

Brave is a BAT-enabled web browser that integrates the BAT platform through Brave Rewards. Brave Rewards is comprised of three complementary features: (1) Ads, (2) Tipping and (3) Auto-Contribute.

Brave Ads

Users who opt into Brave Ads will see privately-matched advertisements from the BAT network and earn a share of the ad revenue in BAT tokens. Since ad matching and delivery is performed by the browser entirely client-side, BAT and Brave Ads requires absolutely no user data collection or tracking. See section: "What Makes BAT Different?"

There are two kinds of advertisements in Brave Ads:

- User Ads:User ads are delivered directly to the user in a separate ad tab at specific moments in the user's browsing experience. The user will receive an ad notification which they can choose to expand or dismiss. If expanded, user ads reveal a landing page in a new browser tab. Users will earn 70% of ad revenue for user ads.

- Publisher-integrated Ads:Publisher ads are viewed by the user on or in association with publisher content, such as an interstitial banner advertisement on a publisher's webpage. Publishers will earn 70% of ad revenue, and users 15%, for publisher ads.

What can I do with BAT?

As a user, BAT tokens can be used in conjunction with Brave Rewards to support one's favorite publishers and content creators on the web. However, BAT will also let users redeem premium content, gift cards, discounts, digital goods and subscriptions with participating brands. (For example, users will be able to redeem BAT rewards at over 250,000 top brand partners in the TAP Network. Learn more about our partnership with TAP, here.) Premium subscriptions and other content purchased with BAT will generate cryptographic receipts that allow the user to enjoy purchased content without having to register for an account with the content provider.

Users can also transfer BAT tokens out of the Brave Rewards wallet by, e.g., linking an Uphold account to Brave Rewards.

Brave Ads Campaign Performance Metrics

Ad confirmations for ad campaign reporting involve the use of zero-knowledge proof (ZKP) protocols and various cryptographic techniques (e.g., blind signatures) to protect user privacy. For example, Brave tipping and auto-contribute utilize the ANONIZE2 privacy protocol, while Brave Ads utilizes a "blind tokens" protocol inspired by Privacy Pass.

Brave cannot tell which publishers a user contributed to, only that someone contributed to the publisher. Likewise, Brave cannot tell which ads a user viewed within a particular ad campaign price bucket, only that the user has been rewarded for the correct number of ad views.

Ad campaign performance metrics include:

- Ad views

- Click-through rates

- Dismissals

- 10 second landings

Additional performance metrics will continue to be added over time.

Brave Tipping & Auto-Contribute

Users can support their favorite publishers and content creators with monthly BAT token contributions and on-the-spot BAT tips. By default, Brave Auto-Contribute will divide a user's monthly auto-contribute budget across visited websites and channels based on how much time the user spends on each. Users can also directly tip websites or channels instantly, and make these tips recurring. When a user contributes to a creator who has not yet verified with the platform, the tip/contribution is marked as "pending" and will remain so for 90 days. During that time, the user’s browser periodically checks to see if the creator has verified, and if so, will process the contribution.

Is BAT restricted to the Brave browser?

While the Brave browser represents the first "BAT-enabled application" and is the primary focus of BAT Roadmap 1.0, the team intends to extend BAT beyond the Brave browser. We envision the BAT platform being extended to other web browsers, chat/messaging applications, games and other attention-economy apps via open source mobile app SDKs, connected TV SDKs, etc. (Read more about our upcoming BAT SDK, here.) For more info on the potential areas of expansion, see our Driving User Adoption and Extending the BAT Platform blog post.

The BAT SDK that will allow developers to integrate BAT-functionality (such as privately-matched ads with revenue share) into their own applications, allowing developers to monetize their apps and reward their users.

"I don’t want to corner the browser market; I think Brave will have a good growth curve and lots of market share among elite users who are very economically valuable, but BAT is the big play. I want the Basic Attention Token to be used widely, which means we will bring it to other browsers and other attention apps — things like podcast players, or games that have ads in them.” —Brendan Eich

What makes BAT different?

BAT represents a fundamental rethinking of digital advertising. The current model depends on third-party tracking, surveillance with tracking pixels, scripts, cookies and countless middlemen as advertisements are matched and delivered to users by external servers.

BAT eliminates the need for third-party tracking and middlemen by matching and delivering ads client-side, locally and on-device. In Brave, an ad catalog comprised of landing page URLs and other campaign segmentation data will be periodically downloaded into the browser. Brave will then match and deliver ads from the catalog to the user, using client-side machine learning algorithms against locally-stored data. Since all matching happens client-side on locally-stored data, absolutely no tracking or user data collection is required, including by Brave Software. (Read more about BAT's innovative, privacy-respecting matching/targeting system in this post.)

Targeting and delivering ads client-side confers many benefits:

- Users’ browsing data (e.g., browsing history) can be kept private, as all data required for ad-matching never leaves the device and third-party trackers are blocked by default.

- Improved ad matching.BAT Ads in the browser can see everything: search queries, Amazon queries and consummations, click logs/tab constellations, absolute above the fold and Z-order visibility and viewability. The browser has the full corpus of user data and intent signals, including active tabs, URL and search keyword entry data, browsing history, etc. The BAT platform, in conjunction with the browser, can therefore match ads with greater precision and determine if a user is actually in the optimal time and place in their browsing experience for an offer.

- Better experience.Since ad matching is performed locally, users do not need to call out to external servers on every page load for tracking scripts, tracking pixels, etc. This leads to a quantifiably faster browsing experience, in addition to battery life and data usage savings. Moreover, since ads can be served in a separate ad tab and not only interstitially, the BAT model helps avoid “banner blindness” and brand-safety issues.

How do I purchase BAT tokens?

- Through BAT’s partner, Uphold.com (fiat currencies, credit & debit card, cryptocurrencies)

- Through Coinbase.com (fiat currencies, credit & debit card)

- By funding one’s Brave wallet with BTC, ETH or LTC (automatic conversion to BAT tokens will occur in the background)

- With credit card or debit card directly through the in-browser wallet

- Secondary exchangesthat list BAT

Note: While we are aware that the token is currently being traded on the exchanges listed here, we have not encouraged or facilitated this exchange trading in any way. We have provided the foregoing information solely as a means of reducing the inquiries we receive directly.

Partnerships & Verified Publishers

BAT and Brave have or have had official partnerships with Dow Jones Media Group, DuckDuckGo, Coinbase Earn, Cheddar, TownSquare Media, Qwant, CIVIC, among others. Major YouTube star partners include Philip DeFranco and Bart Baker.

Hundreds of thousands of websites, YouTube creators, Twitch streamers and more are verified creators with the Brave Rewards program and receive monthly contributions in BAT tokens from their audiences. Publishers who've already verified with Brave Rewards include major sites such as Wikipedia, The Guardian, The Washington Post, The LA Times, NPR.org, VICE, Vimeo, Slate, Barron's, Ars Technica, Khan Academy, in addition to major YouTube and Twitch channels totalling over several hundred million subscribers. For a full list, see BATGrowth.com, a community-made resource.

BAT Token Launch Info

BAT's token launch took place on May 31st, 2017. The total supply of BAT tokens (1.5B tokens) was created during the token launch, of which 1B tokens were sold and the remaining 500M set aside for a user growth pool and development team pool. Tokens are designed to redeem services and provide utility within the platform. There are no plans for any subsequent token creation event or sale.

The proceeds from the token launch are being used for the development and growth of the platform. See this blog post for a breakdown of how the proceeds are distributed.

In addition to the token launch, the project is funded by Founders Fund, Foundation Capital, Propel Venture Partners, Pantera Capital, DCG, Danhua Capital, and Huiyin Blockchain Venture among others.

Why should I care about BAT?

The multibillion-dollar digital advertising industry is in crisis. User privacy has become a casualty in an ever-increasing consumer-surveillance ad model that relies on tracking and profiling users. Publishers and content creators are shutting down or retaliating with self-destructive tactics as users enable ad-blockers in response to privacy violations, irrelevant ads and malvertising. Ad fraud is rampant throughout the system ($16B or more in the US alone in 2017), and advertisers are struggling to find solutions that comply with new GDPR regulations.

Basic Attention Token fixes underlying economic incentives by correctly pricing user attention, delivering on privacy compliance, and offering a new win-win-win digital advertising paradigm for publishers, advertisers and users.

With BAT,

- Publisherswill be able to remonetize lost segments while adding additional revenue streams;

- Advertiserswill see better ad matching, brand safety, less fraud and more transparent accounting macro flows on the blockchain;

- Userswill be rewarded for their attention, and will no longer have to sacrifice their data, privacy or web experience.

BAT is a brilliant solution to a systemic problem, spearheaded by the creator of JavaScript, co-founder of Mozilla and Firefox, alongside an all-star team.

The main take for us here is: there is a circular BAT economy with micropayments to normal users, which triggers different behaviors. This is my starting point: such behaviors can be categorized leading to a diagram of the flow of BAT.

- Accumulating BAT can make sense because of the tendency to equilibrium which we have reasonable expectations to be higher than the current one. Long term hold is normally represented by BTC at the current stage of cryptospace.

- Conversion to other cryptos can happen to hold long term, go to a stable coin related, for example, to USD or to speculate on exchanges.

- Another option are payments which can be done in bat in the circular ecosystem or in the normal world through services converting crypto to cash or as deposits in liquidity pools where, counterparty risk is balanced by interest rates on a hold position (note that pools conditions must be carefully studied: they could also liquidate positions and depositors could incur in losses).

- Liquidity pools are an interesting phenomenon. They are pool of various cryptos, which, provided the liquidity is enough, can be exchanged at minimal spreads. We have seen at the beginning that centralized exchanges, which are often liquid, are usually able to apply higher spreads than decentralized.

Micropayments. Liquidity paths (beginner and expert mode).

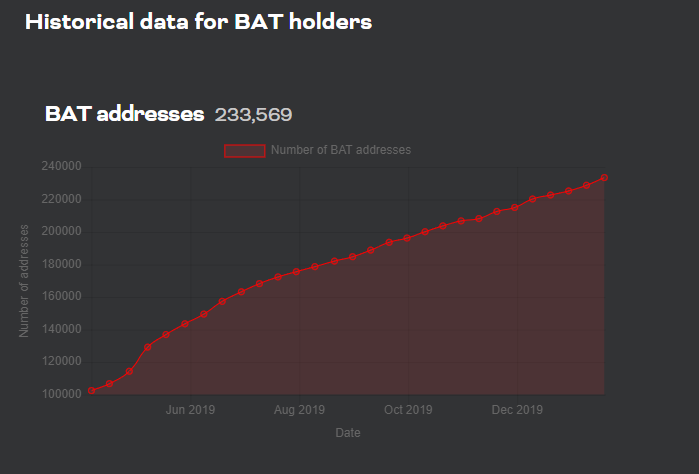

Among the 250k BAT addresses and growing of the graphic showed above there are plenty of little ones, which staying in a temporary HOLD can become around 100-1000 USD depending also from currency exchange. We can think statistically and we can easily convince ourselves that thousands of these accounts could decide to follow the path convert to other crypto (stable, BTC, ETH, OXT) the type depending from the need. This situation creates some micropayment liquidity paths:

- Uphold BAT account from brave rewards -> switch in uphold -> use uphold services (easy path till brave will not have its integrated wallet; it is a primitive user not looking at the high charge of the service)

- Uphold BAT account from brave rewards-> move out to other bat account (free of charge because of conventions brave - uphold) -> swap in the new wallet (user a bit more evoluted who has researched an eventual wallet offering better conditions. Normally the bid ask spread hidden in these conversions are high)

- Uphold BAT account from brave rewards->liquidity pool for deposit or swaps (user careful about slippage or similar) (user more sophisticated)

- Uphold BAT account from brave rewards->other wallet connected with SDEX and other liquidity pools -> this solution which would be very interesting is prevented by the lack of a liquid BAT anchor in stellar.

- other wallet as target from applications like publish0X -> all possible variants

The best liquidity path looks to accumulate in a known wallet as BAT will not fall to deep, according to the expansion combined with the stability model described and collect informations about the best liquidity pools. Once liquidity pools are better known the BAT holder can deposit BAT in a pool where capital is insured and interest accrued (compound seems to be suited but research has to be done) or exchange in uniswap (just to mention a liquidity pool) being careful about slippage if he wants to HODL e.g. BTC. The last could be a good liquidity path BAT to BTC. For a trader moving fo the SDEX (stellar decentralized exchange) would be nice but the absence of a liquid BAT XLM anchor forces to an unneeded haircut in a liquidity pool or in a trusted wallet for the swap bat to xml.

I leave open the topic: calculation of the best liquidity path by user need as it is clear that the pre requisite is study deeply:

- liquidity pools offer (uniswap, changelly, compound)

- Wallets wallet swap service (more expensive but simple: check many wallets), stellar hybrid wallets to move to SDEX trading using the liquid anchors only (necessary to study wallets like lobstr, litemint at least to see the full proposal)

Conclusion

We have developed many topics trying not to repeat the usual known things about brave and BAT. At first we have classified the token and applied the usual blueprint to evaluate the BAT token. Then we have focused on the micropayments flow introducing the role of wallets, liquidity pools and DEX/SDEX in the growing microfinance which is taking shape in this ecosystem.

NEXT STEPS

A continuation of the best liquidity path by user need could require to dig deeper in:

- stellar wallets: Litemint and Lobstr

- study liquidity pools: uniswap, compound, changelly, dx/dy plus research others.

- Play with the SDEX to show way in and out plus internal trading. Suggestion of some liquid anchors and hybrid wallets improvements.

- understand the motivation behind the lack of liquid stellar anchor for assets like bat, steem and, in general tokens from circular economies. Understand how to add and if it makes sense.

- understand the liquidity path in remittance business as well in cashing out from circular crypto economics like the BAT/Brave one

{kind=link}