If you want more cryptocurrency analysis including full-length research reports, trading signals, and social media sentiment analysis, use the code "Publish0x" when subscribing to CryptoEQ.io to make your first month of CryptoEQ just $10! Or simply click the button above!

1Inch

1inch is a leading cryptocurrency aggregator that revolutionized the decentralized finance (DeFi) landscape by streamlining and optimizing the trading experience for its users. Launched in 2019 by Sergej Kunz and Anton Bukov, 1inch emerged from a hackathon project and rapidly evolved into a comprehensive DeFi platform, garnering a reputation for its innovative approach to solving the inefficiencies prevalent in decentralized exchanges (DEXs).

As a DeFi aggregator, 1inch operates across various blockchain ecosystems, such as Ethereum, Arbitrum, Optimism, Polygon, Avalanche, BNB Chain, Gnosis, Fantom, Klaytn, and Aurora. Its primary objective is to facilitate seamless and efficient trading of cryptocurrencies while minimizing slippage and ensuring optimal price execution. To achieve this, 1inch employs its proprietary Aggregation Protocol (AP), which intelligently routes trades through multiple DEXs and liquidity sources, securing the best available rates for users.

In addition to its aggregation capabilities, the 1inch platform has introduced several other DeFi services over time. These include the 1inch Liquidity Protocol, an automated market maker (AMM) that allows users to provide liquidity and earn passive income through liquidity mining rewards. Another noteworthy development is the 1inch Limit Order Protocol (LOP), which supports conditional limit and stop-loss orders with no fees.

The platform's latest innovation, Fusion mode, enables users to place orders with predetermined price and time parameters without incurring network fees. This feature is partially based on the existing technology of the 1inch Limit Order Protocol and the 1inch Aggregation Protocol.

1inch is governed by a Decentralized Autonomous Organization (DAO), which uses the native 1INCH token for decision-making and operational management. By offering a suite of DeFi solutions and continuously improving its technology, 1inch has positioned itself as a powerful tool for cryptocurrency users, fostering a user-friendly, cost-effective, and efficient trading experience in the ever-evolving DeFi landscape.

What’s Wrong with DEXs?

DEX Design and Low Liquidity

Decentralized exchanges (DEXs) are typically open-source, permissionless protocols that allow users to create liquidity pools for ERC-20 trading pairs and enable trustless token swaps executed from smart contracts for small fees. There are two main types of DEXs: order book-based and liquidity pool-based. Liquidity pool-based DEXs currently dominate the DEX landscape.

DEXs provide traders with a trustless trading experience with no counterparty risk and, oftentimes, no Know-Your-Customer (KYC) requirements. DEXs also let DeFi users yield farm, i.e., locking up their tokens into a liquidity pool to earn trading fees/rewards for providing liquidity. The liquidity provided is used to make the market for a trading pair according to a mathematical formula. Trades within the pool alter the trading pair balance/ratio and, thus, changes the token prices. Arbitrageurs/traders are then incentivized to bring prices in line with the wider market.

Most DEXs execute their digital exchange under a Constant Function Market Makers (CFMM) architecture, a type of model of an Automated Market Maker (AMM). CFMMs use a constant function as their pricing mechanism for trading token A for token B. “Constant function” refers to the fact that the product of the asset reserves must remain constant with all incoming trades.

However, because CFMMs markets are dictated by a formula, they depend on arbitrage traders to bring prices back in line with the wider market when prices deviate. If prices become too deviated from the wider market, traders will buy tokens on other platforms to sell them on the CFMM DEX for a better price.

Inspired by Ethereum Co-Founder Vitalik Buterin and created by Haden Adams, Uniswap was the first AMM that let anyone create liquidity pools for any Ethereum token and to do so much faster than centralized exchanges. Anyone can provide liquidity to a pool that’s then distributed to providers in respect to the amount of the provider’s pool share. Stakers provide a deposit of two tokens—either ETH and an ERC-20 token or two ERC-20 tokens—in return for interest from the principle.

Due to these systemic problems, there have been several efforts to develop forms of cross-chain liquidity, liquidity that’s universal across two or more ecosystems. Present designs to implement this concept into the space include several projects that have developed solutions, such as atomic swaps or wrapped tokens. Connecting liquidity across many different blockchains works to make liquidity instantaneously accessible across ecosystems, allowing protocols to exist (and capture users) across blockchain networks.

Why Aggregators?

Aggregators offer seamless, efficient improvements to overall user experiences within the blockchain industry. This comes with many advantages, including time-saving measures for investors and users alike by simultaneously interacting with multiple chains. Additionally, these efficiency improvements also help to reduce costs that fall back onto the user. A single interface that aggregates potential transactions delivers adoptable technology that is more capable than other models for onboarding off-chain, mainstream users. By using available resources, including data, smart contracts, and existing APIs, aggregators offer users far more verifiable transparency.

The major problem associated with CLAs and cross-chain technologies is how early in development these tools are. Novel technologies and new concepts generally don’t have fully fleshed-out technology, nor are they 100% functional as intended in many cases. There are growing pains with new technology, particularly cross-chain technology. There are different approaches to building this technology; some tend to offer expansions and more options to users slowly, while others launch full services. There is a risk tradeoff on the part of the users when considering what to adopt.

What to consider in a trade

Gas costs

Ether is digital money on the Ethereum network and is required when a user interacts with the network to pay network fees in the form of “gas.” Gas is the allocative internal pricing mechanism in Ethereum used in transactions. It’s a derivative of Ether designed to mitigate spam attacks on the network and efficiently allocate computational resources.

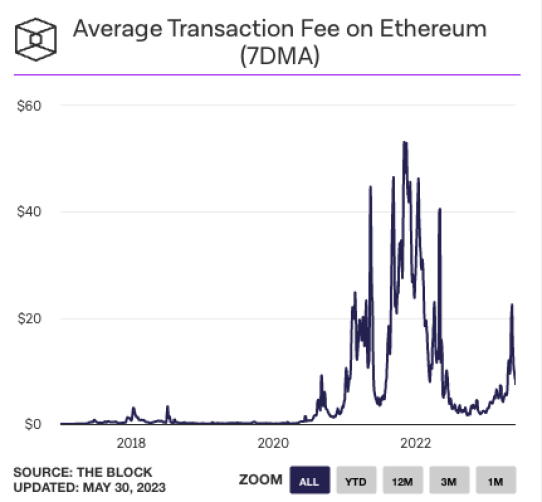

Gas prices (and transaction fees) can reach quite high price levels during periods of network congestion. This is because blocks and block space on the execution layer of a chain are scarce. There are only so many blocks that can be verified and added to the chain each second/minute. Once demand outstrips this finite resource, the only recourse users have left to ensure their transaction gets into a block (and executed) is to pay more than the market rate for transaction fees.

Image credit: TheBlock.crypto

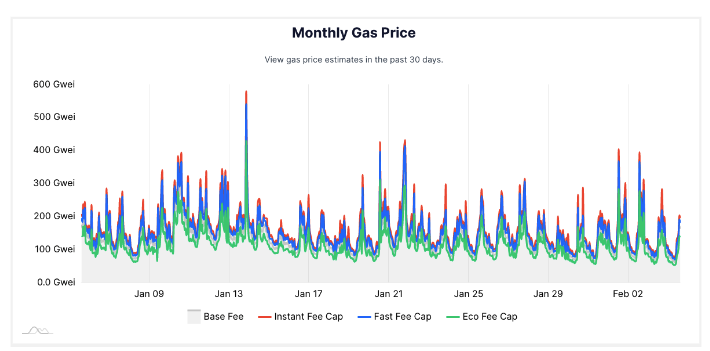

Ethereum's scalability on the base layer is limited by the block gas limit rather than the block size. There is an upper threshold on the amount of gas that can be expended in a block with 30 million gas being the absolute maximum.

Users pay different amounts of gas depending on the type of transactions they’re looking to execute. The more complex the transaction, the more gas is required. Sending one ETH to a friend (an ETH transfer) is far simpler (computationally-speaking) than making a trade on a DEX. Thus, trading on a DEX requires more gas and is more expensive. Below is a monthly chart of ETH gas fees.

ETH gas market. Source

While Ethereum gas costs may be prohibitively expensive for the everyday user, whales are far less price-sensitive due to their high-value transaction size. A $50 transaction fee is outrageous for a $100 trade but negligible for a $1M trade. Therefore, whales transacting on Ethereum do so because Ethereum has the best security, liquidity, and DeFi optionality of any cryptocurrency ecosystem.

Below is a breakdown of the average gas used and average fees paid for some of Ethereum’s top DEXs. Despite the architectural intricacies of each DEX, the difference paid in gas fees from one to the next is ~$20. This means traders and whales can feel confident transacting on their preferred DEX knowing that the opportunity cost could be as little as $10 (all else being equal).

However, things are never equal from one DEX to the other. Traders and whales that choose a DEX must account for a number of factors.

However, things are never equal from one DEX to the other. Traders and whales that choose a DEX must account for a number of factors like liquidity and market depth (previously discussed), tooling and UI/UX features, fees, trading pairs, regulations, exchange reliability, and more discussed in the following sections.

Smart contract security and oracle reliability

Above all else, whales (and everyone) want to ensure their funds are safe when interacting with a dApp/smart contract. DeFi and DEXs are fairly new innovations that are still constantly evolving. Risks are abundant! Token pairs and liquidity mean nothing if your trading venue is insecure.

Some ways traders can judge a DEX’s security:

- Reputation and time in the market (mature protocol vs new one)

- Investigating the code

- Vetting the team

- Checking and verifying any third-party audits

- Investigating the oracle price feeds used

- Using services like defisafety.com

Trading pairs/stablecoin risk

As mentioned in a previous section, stablecoins have become a critical part of the DeFi ecosystem and remain part of the most dominant and liquid trading pairs. The stablecoin market really began to grow in 2020 when the proliferation of DeFi dApps and yield farming opportunities exploded within the Ethereum ecosystem, dubbed “DeFi Summer.” The two charts below illustrate both stablecoin supply and total DeFi users began to reach inflection points in H2 2020.

As stablecoin adoption and usage have become more ubiquitous, their role and the risks associated with them have also grown. Traders and whales need a reliable, ultra-liquid stablecoin for maneuvering in and out of their positions. However, stablecoins can deviate from their $1 target peg, especially in times of high market volatility.

Current volatility for stablecoins on centralized exchanges has never been better thanks to increased liquidity, more robust trading infrastructure, and arbitrage opportunities. Below is a chart of the 20-day rolling volatility for four of the largest stablecoins using USD-denominated pairs trading on crypto-to-fiat exchanges. Pre-2020, volatility among the stablecoins oscillated between 10%-35%. Since then, it has declined significantly, down to its current rate of ~5%. Interestingly, despite Tether being a few years older, having a larger supply, and more liquidity, Tether’s USDT is slightly more volatile than the U.S.-compliant USDC stablecoin.

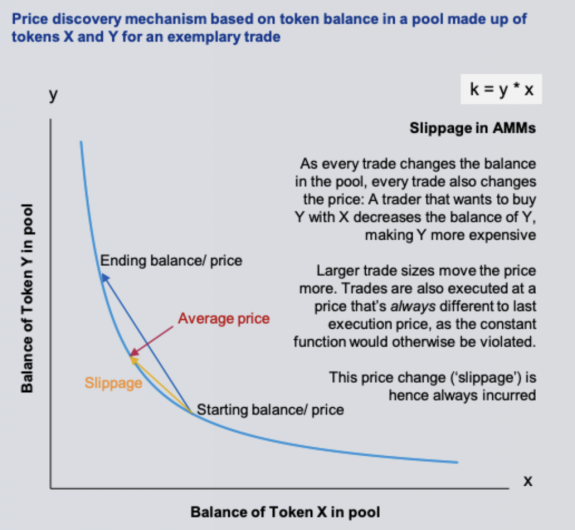

Slippage

Price slippage, as mentioned previously, is the difference between the expected price of a trade and the price at which the trade is executed. When a trader places a market order on an exchange, they expect that order to be filled at the current price. However, this is not always the case, especially for large orders or illiquid markets. Slippage can occur for two reasons: A change in the bid/ask spread in between the time a trade is placed and the trade is filled, or insufficient market depth.

In times of high market volatility, the best bid and ask for a crypto asset can meaningfully change between the time the trade is placed and the time it’s executed. If the ultimate execution price is less than the expected execution price, the net result is positive slippage (advantageous result). Conversely, if the final execution price is greater than the expected execution price, the trader is subjected to negative slippage, a less favorable trade.

In less liquid markets, slippage can also result from insufficient market depth. For a CEX with a traditional order book, depth is calculated from the number of bids and asks on either side of the mid price. The “deeper” the order book, the less sensitive the price to large whale orders. However, if the order book is “thin” (less liquidity), a large whale market order may move the price due to what is known as “order splitting.” When an order is too large to be filled at one price, it’s divided into multiple orders at different price levels. This is how slippage is realized.

Below is an example of the slippage experienced on the CEX Kraken when attempting to execute a $100,000 BTC and ETH order in 2020. Note that ETH slippage (green and yellow) is more volatile and higher on an absolute basis due to the inferior market depth of ETH vs BTC. While this example is dated, the relationship between slippage and illiquid altcoins remains valid.

ETH slippage is greater than BTC slippage due to less market depth.

Below is a more recent analysis conducted by KMPG on total cost and slippage across different markets. Unsurprisingly, the OTC options provided the least amount of total cost across all markets (crypto-to-fiat and crypto-to-stablecoin). However, DEXs (specifically Curve and Uniswap V3) have really begun to shine in the stablecoin-to-stablecoin category, even producing less slippage than their centralized counterparts. This data is just another example of how DEXs are maturing in a short amount of time and may soon rival CEXs for most trading pairs.